Introduction – Addressing Core Industry Needs and Solutions

Meat processors, cheese manufacturers, and pharmaceutical companies face a critical packaging challenge: oxygen causes rapid spoilage (meat discoloration, cheese mold, lipid rancidity), while moisture loss leads to dehydration and weight loss. Standard PE films have poor barrier properties (OTR 5,000-10,000 cc/m²/day), limiting shelf life to 7-14 days. PVDC shrink film is an efficient packaging material. Polyvinylidene chloride (PVDC) is used as the barrier layer in multilayer shrink films for meat and cheese packaging. It is heat-sealable and serves as an excellent barrier to oxygen, water vapor, odors and flavors. PVDC offers exceptional oxygen barrier (OTR 1-10 cc/m²/day) and moisture barrier (MVTR 1-5 g/m²/day), extending shelf life to 30-90 days for vacuum-packed meat, cheese, and seafood. It is widely used in raw meat primal cuts, processed meat, cheese wheels, aquatic products, and pharmaceutical blister packaging.

Global Leading Market Research Publisher QYResearch announces the release of its latest report *“PVDC Shrink Film – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”*. Based on current situation and impact historical analysis (2021-2025) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global PVDC Shrink Film market, including market size, share, demand, industry development status, and forecasts for the next few years.

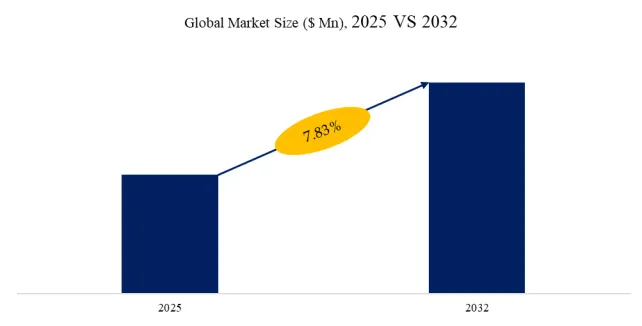

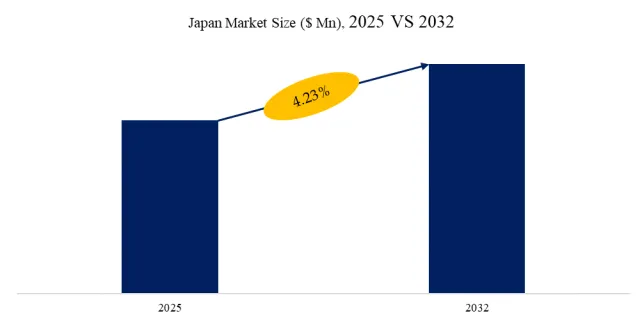

The global market for PVDC Shrink Film was estimated to be worth US$ million in 2025 and is projected to reach US$ million, growing at a CAGR of % from 2026 to 2032.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/5985500/pvdc-shrink-film

1. Core Market Drivers and Barrier Technology

The global PVDC shrink film market is projected to grow at 5-7% CAGR through 2032, driven by fresh meat demand (200M+ tons annually), cheese (20M+ tons), aquatic products (150M+ tons), and food waste reduction. PVDC’s dual barrier (oxygen + moisture) is superior to EVOH (moisture-sensitive) and nylon (lower barrier).

Recent data (Q4 2024–Q1 2026):

- PVDC OTR: 1-10 cc/m²/day (vs. EVOH 0.5-5, vs. nylon 50-100, vs. PE 5,000-10,000).

- PVDC MVTR: 1-5 g/m²/day (excellent, vs. EVOH moisture-sensitive >80% RH).

- Shelf life: fresh beef 30-60 days, cheese 90-180 days, salmon 20-30 days.

2. Segmentation: Film Type and Application Verticals

- PVDC Coated Film: 55% market share. PVDC emulsion coated onto substrate (BOPP, PET, nylon). Lower cost, good barrier. Price: $2-6 per kg. Best for: cheese, processed meat, dry foods.

- Multi-layer Coextruded Film: 45% share (fastest-growing at 7% CAGR). PVDC coextruded with PE, EVA, or nylon. Better layer adhesion, uniform barrier, no pinholes. Higher cost. Price: $4-10 per kg. Best for: raw meat (primal cuts), aquatic products, pharmaceuticals.

- By Application:

- Raw Meat: 40% share. Beef, pork, lamb primal cuts (export, long-distance distribution).

- Meat Products: 25% share. Ham, turkey, sausages, bacon.

- Aquatic Products: 15% share. Fresh fish (salmon, tuna), shellfish.

- Dairy Products: 10% share. Cheese (cheddar, gouda, mozzarella).

- Drugs (Pharmaceuticals): 5% share (highest value). Blister packaging for moisture/oxygen-sensitive tablets.

- Others: 5%.

3. Industry Vertical Differentiation: PVDC vs. EVOH vs. Nylon vs. PE

| Parameter | PVDC | EVOH | Nylon | PE |

|---|---|---|---|---|

| Oxygen barrier (OTR) | 1-10 | 0.5-5 | 50-100 | 5,000-10,000 |

| Moisture barrier (MVTR) | 1-5 (excellent) | Moderate (moisture-sensitive >80% RH) | 5-20 (good) | 5-20 (good) |

| Flavor/odor barrier | Excellent | Excellent | Moderate | Poor |

| Clarity | Good | Excellent | Good | Good |

| Cost | Moderate-High | Moderate | Low-Moderate | Low |

| Sustainability | Low (chlorine, not recyclable) | Moderate (recyclable with PE) | Moderate | High (recyclable) |

| Best for | High moisture + oxygen barrier (meat, cheese) | Oxygen barrier (dry foods) | Puncture resistance | Low-cost, short shelf life |

Unlike EVOH (moisture-sensitive, loses barrier at >80% RH), PVDC maintains excellent barrier in high-humidity environments (meat, cheese packaging). However, PVDC contains chlorine and is not recyclable, facing sustainability pressure.

4. User Case Studies and Technology Updates

Case – Asahi Kasei (Japan) : Global PVDC resin leader. 2025: Multi-layer PVDC shrink film for fresh beef export (US to Japan, 45-day shelf life). Price: $5-8 per kg.

Case – Kureha Corporation (Japan) : PVDC resin and film manufacturer. 2025: PVDC shrink bag for cheese (cheddar, 180-day shelf life). Price: $6-10 per kg.

Case – Shuanghui (China) : Largest Chinese meat processor. 2025: PVDC shrink film for ham and sausages (domestic distribution). Price: $3-5 per kg.

Case – Suzhou Tipack (China) : Domestic film manufacturer. 2025: PVDC coated film for aquatic products (salmon, 20-day shelf life) at $2-4 per kg (30-50% below Western brands).

Technology Update (Q1 2026) :

- Halogen-free alternatives: PVDC faces regulatory pressure (chlorine, dioxin concerns). EVOH + moisture barrier layer (PP or PE) emerging as replacement.

- Thinner PVDC layers: New coating technology reduces PVDC thickness (saving material, cost) while maintaining barrier.

- Recyclable PVDC-free structures: PE/EVOH/PE (mono-material recyclable) gaining share for sustainability-focused brands.

5. Exclusive Industry Insight: PVDC vs. EVOH TCO and Sustainability Trade-off

Our analysis reveals that PVDC has better moisture barrier than EVOH (critical for high-humidity meat packaging), but faces sustainability pressure (chlorine, not recyclable). EVOH + moisture barrier layer (PP/PE) is the long-term replacement.

Proprietary TCO comparison (1M primal cuts/year, export, 30-day transit) :

| Parameter | PVDC Shrink Film ($0.25) | EVOH/PE ($0.22) | Difference |

|---|---|---|---|

| Oxygen barrier (OTR) | 2 cc/m²/day | 1 cc/m²/day | Comparable |

| Moisture barrier (80% RH) | Excellent (1-5 MVTR) | Moderate (barrier degrades) | PVDC superior |

| Spoilage rate (high humidity transit) | 2% | 4% | PVDC saves 20,000 cuts |

| Annual spoilage cost (1M cuts, $200/cut) | $4M | $8M | PVDC saves $4M |

| Recyclability | No (chlorine) | Yes (PE/EVOH/PE) | EVOH better for ESG |

Key insight: PVDC outperforms EVOH in high-humidity environments (ocean freight, refrigerated containers) – critical for meat export. EVOH is preferred for dry goods and sustainability-focused brands.

Decision matrix – Choose PVDC when :

| Factor | PVDC Recommended | EVOH Recommended |

|---|---|---|

| Humidity environment | High (>80% RH – ocean freight, tropical) | Low-moderate (<80% RH – dry storage) |

| Moisture barrier requirement | Critical | Moderate |

| Sustainability priority | Low | High (recyclable) |

| Budget | Moderate-High | Moderate |

| Regulatory pressure (chlorine) | Low (unregulated markets) | High (EU, California) |

Regional Dynamics:

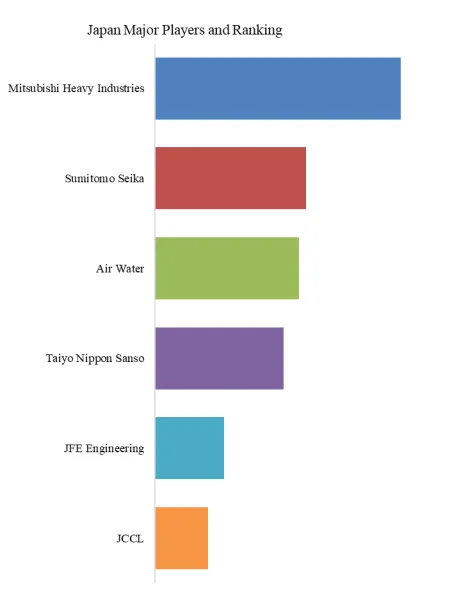

- Asia-Pacific (50% market share, fastest-growing at 8% CAGR): Largest and fastest-growing. China (Shuanghui, Hubei Hawking, Suzhou Tipack – domestic production). Japan (Asahi Kasei, Kureha). High meat consumption, growing export.

- North America (25% market share): US, Canada. PVDC for meat export (US to Asia). Sustainability pressure driving EVOH conversion.

- Europe (20% market share): Germany, France, UK, Italy. Strong sustainability focus (PVDC declining, EVOH rising). Vibac, Polinas, Solvay, Chiripal.

- Rest of World (5%): Latin America (Brazil meat export), Middle East.

Market Outlook 2026–2032

The global PVDC shrink film market is projected to grow at 5-7% CAGR, reaching an estimated $XX billion by 2032. Raw meat remains largest segment (40% share). Multi-layer coextruded film fastest-growing (7% CAGR). PVDC faces sustainability pressure (chlorine, not recyclable) – EVOH + moisture barrier layer gaining share in Europe, North America. Asia-Pacific remains strong for PVDC (less regulatory pressure). Halogen-free alternatives emerging.

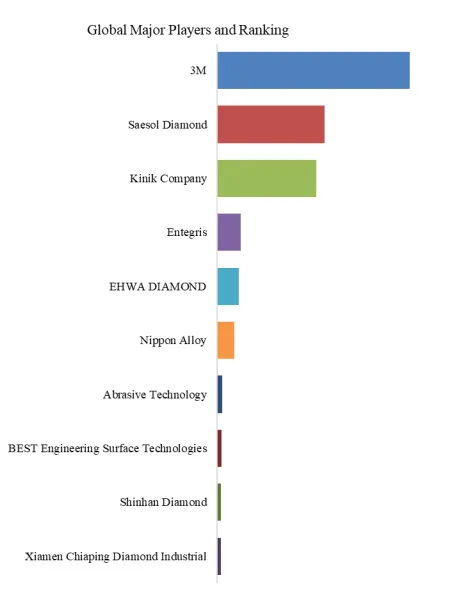

Success requires mastering three capabilities: (1) PVDC emulsion coating or coextrusion (uniform barrier, no pinholes), (2) moisture barrier optimization (maintain performance at >80% RH), and (3) transition to recyclable alternatives (PE/EVOH/PE) for sustainability-focused markets. Vendors with PVDC portfolios (Asahi Kasei, Kureha, Chiripal, Vibac, Astar, Polinas, Solvay, Shuanghui, Hubei Hawking, Suzhou Tipack) lead in Asia-Pacific and meat export; EVOH-based producers gain in Europe and North America.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp