AI Data Center Active Electrical Cable (AEC) Modules

AI Data Center Active Electrical Cable (AEC) Modules are high-performance interconnect modules engineered with integrated Retimer chips to handle the extreme data rates required by hyperscale AI computing clusters. Unlike traditional Direct Attach Copper (DAC) cables, AECs embed active electronics within the connectors at both ends to compensate for signal loss and remove jitter. This allows them to support massive bandwidths—such as 800G and 1.6T—while maintaining the cost-effectiveness of copper. In 2026 AI infrastructures, AECs have become a pivotal component in NVLink hierarchical architectures and distributed training fabrics, offering lower power consumption than Active Optical Cables (AOCs) and greater reach with thinner, more flexible cabling than standard passive copper.

AI Data Center Active Electrical Cable (AEC) Modules Market Summary

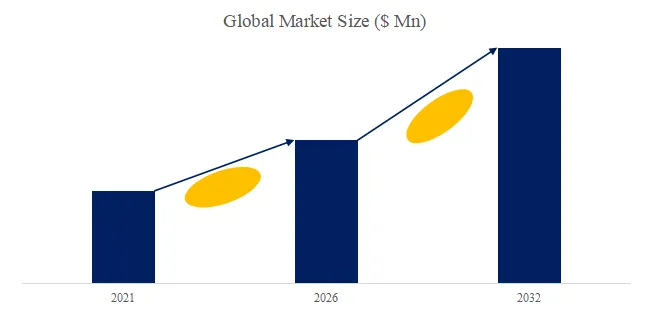

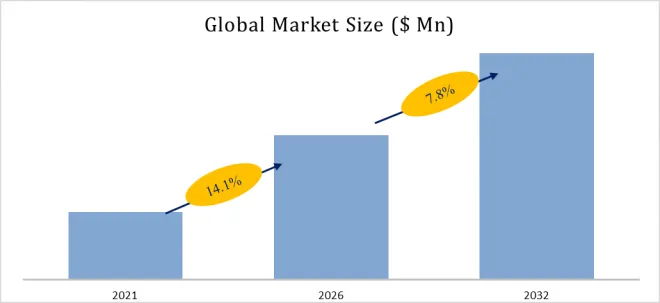

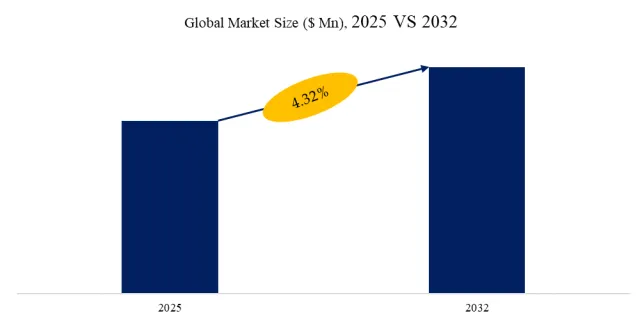

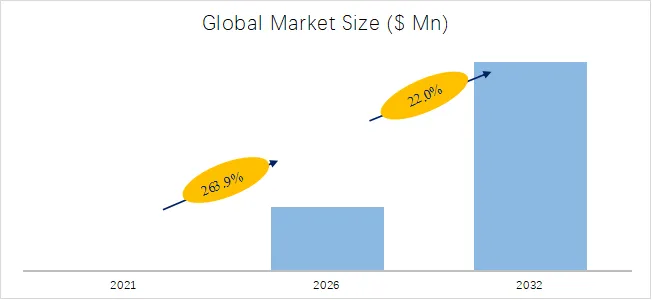

According to the new market research report “Global AI Data Center Active Electrical Cable (AEC) Modules Market Report 2026-2032”, published by QYResearch, the global AI Data Center Active Electrical Cable (AEC) Modules market size is projected to reach USD 2.66 billion by 2032, at a CAGR of 22.0% during the forecast period.

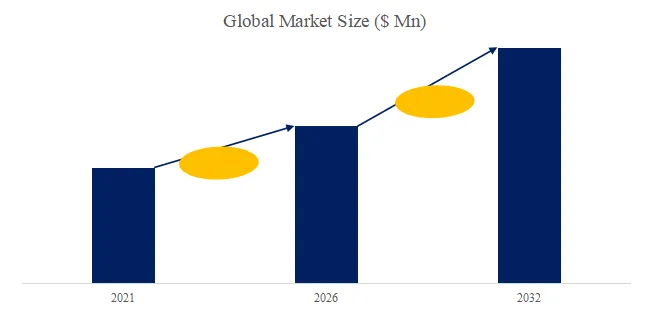

Global AI Data Center Active Electrical Cable (AEC) Modules Market Size (US$ Million), 2020-2031

Above data is based on report from QYResearch: Global AI Data Center Active Electrical Cable (AEC) Modules Market Report 2026-2032 (published in 2025). If you need the latest data, plaese contact QYResearch.

Global AI Data Center Active Electrical Cable (AEC) Modules Market

Market Drivers:

The rapid deployment of AI training clusters and hyperscale data centers is the primary driver of the Active Electrical Cable (AEC) modules market. As GPU-based servers move to 400G, 800G, and future 1.6T interconnect speeds, traditional passive copper cables face signal integrity limitations and optical modules remain relatively expensive and power-intensive at short reach. AEC modules integrate retimers or signal conditioning chips inside the cable assembly, enabling high-speed, low-latency connectivity over short distances (typically 1–7 meters) with lower power consumption than optical transceivers. The increasing adoption of high-radix switch architectures, high-density racks, and top-of-rack to GPU server connections in AI clusters significantly boosts demand for AEC interconnect solutions.

Restraint:

Despite strong demand, the AEC modules market faces constraints related to thermal management, interoperability, and standardization. The integration of active semiconductor components within the cable increases design complexity and requires careful power and heat dissipation control in dense server environments. Compatibility between switch vendors, GPU platforms, and cable firmware can also create qualification barriers. In addition, rapid evolution of optical interconnect technologies and co-packaged optics (CPO) may limit long-term adoption in certain architectures, especially for higher-reach connections where optical links remain technically superior.

Opportunity:

Significant opportunities arise from the expansion of AI inference infrastructure and next-generation Ethernet and InfiniBand networks. As data centers transition toward higher port counts and disaggregated architectures, operators increasingly seek solutions that balance cost, power efficiency, and installation simplicity. AEC modules offer a compelling middle ground between DAC and optical modules, particularly for rack-level and row-level connectivity. Emerging liquid-cooled racks, modular data center deployments, and edge AI facilities further expand deployment scenarios. In addition, continued SerDes advancements and low-power retimer ICs are expected to extend AEC reach and bandwidth, supporting future 1.6T and 3.2T interconnect ecosystems.

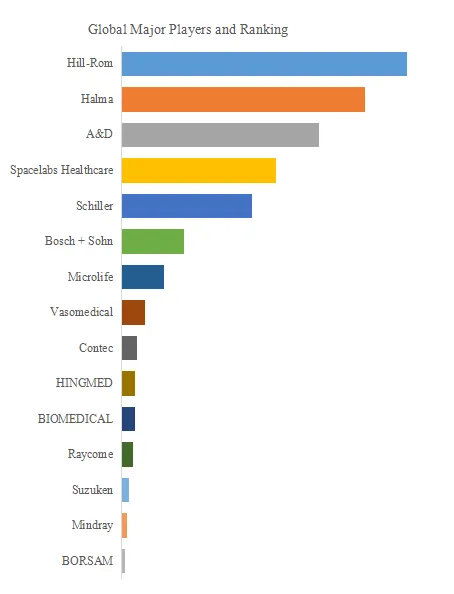

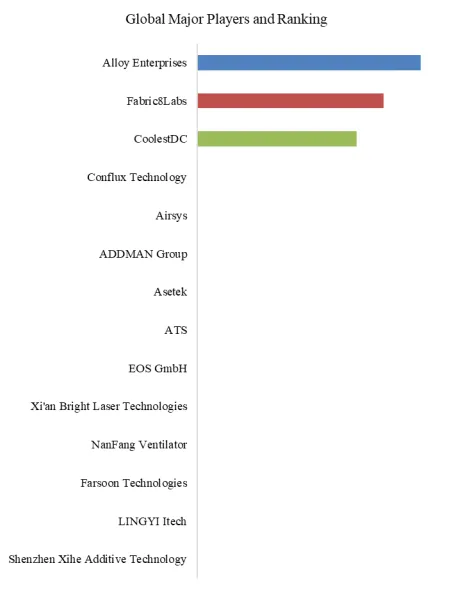

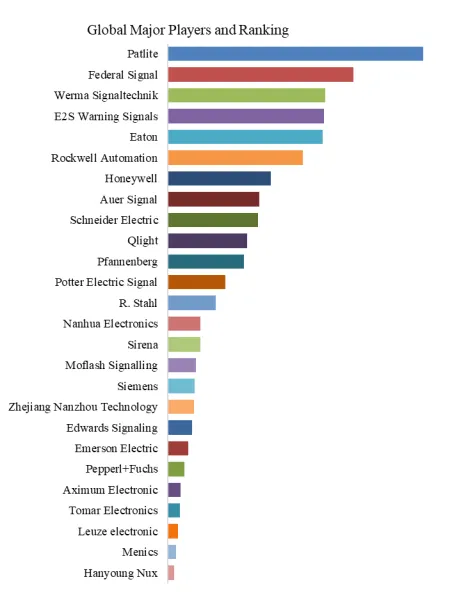

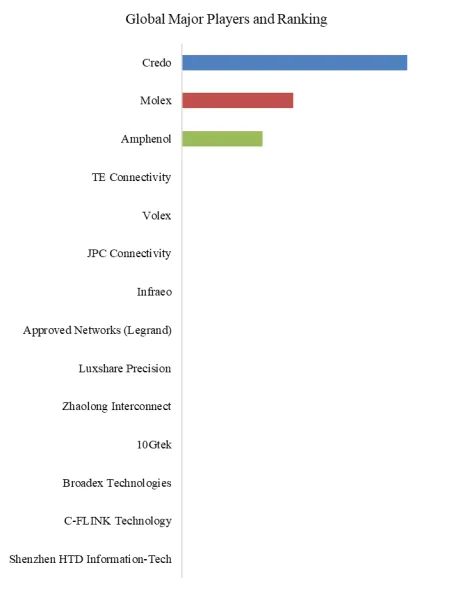

Global AI Data Center Active Electrical Cable (AEC) Modules Top 14 Players Ranking and Market Share (Ranking is based on the revenue of 2025, continually updated)

Above data is based on report from QYResearch: Global AI Data Center Active Electrical Cable (AEC) Modules Market Report 2026-2032 (published in 2025). If you need the latest data, plaese contact QYResearch.

This report profiles key players of AI Data Center Active Electrical Cable (AEC) Modules such as Credo, Molex, Amphenol.

In 2023, the global top five AI Data Center Active Electrical Cable (AEC) Modules players account for 64.1% of market share in terms of revenue. Above figure shows the key players ranked by revenue in AI Data Center Active Electrical Cable (AEC) Modules.

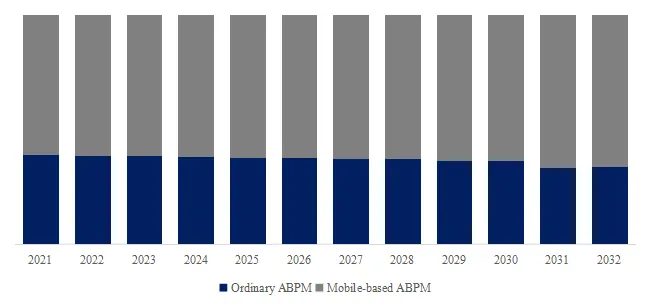

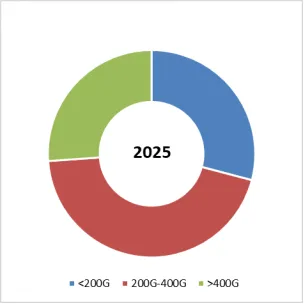

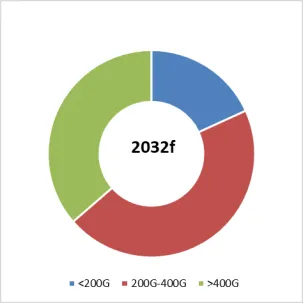

AI Data Center Active Electrical Cable (AEC) Modules, Global Market Size, Split by Product Segment

Based on or includes research from QYResearch: Global AI Data Center Active Electrical Cable (AEC) Modules Market Report 2026-2032.

In terms of product type, 200G-400G is the largest segment, hold a share of 39%,

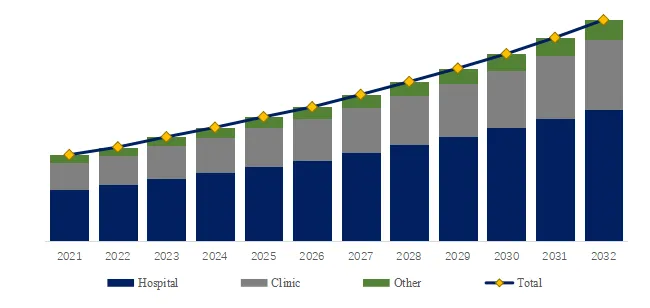

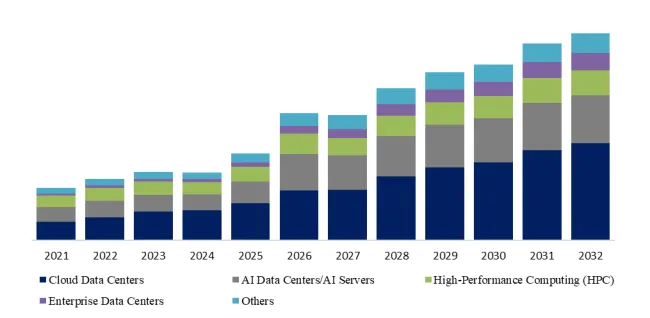

AI Data Center Active Electrical Cable (AEC) Modules, Global Market Size, Split by Application Segment

Based on or includes research from QYResearch: Global AI Data Center Active Electrical Cable (AEC) Modules Market Report 2026-2032.

In terms of product application, Cloud Data Centers is the largest application, hold a share of 42.5%,

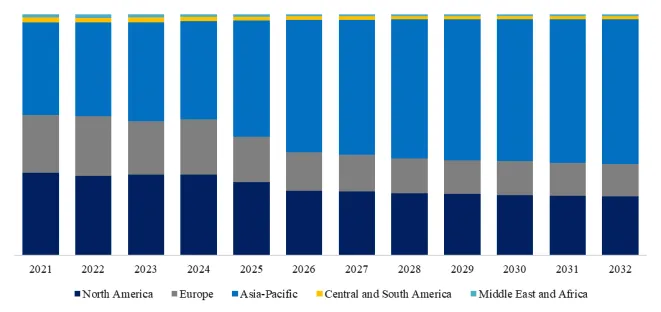

AI Data Center Active Electrical Cable (AEC) Modules, Global Market Size, Split by Region

Based on or includes research from QYResearch: Global AI Data Center Active Electrical Cable (AEC) Modules Market Report 2026-2032.

About QYResearch

QYResearch founded in California, USA in 2007.It is a leading global market research and consulting company. With over 17 years’ experience and professional research team in various cities over the world QY Research focuses on management consulting, database and seminar services, IPO consulting, industry chain research and customized research to help our clients in providing non-linear revenue model and make them successful. We are globally recognized for our expansive portfolio of services, good corporate citizenship, and our strong commitment to sustainability. Up to now, we have cooperated with more than 60,000 clients across five continents. Let’s work closely with you and build a bold and better future.

QYResearch is a world-renowned large-scale consulting company. The industry covers various high-tech industry chain market segments, spanning the semiconductor industry chain (semiconductor equipment and parts, semiconductor materials, ICs, Foundry, packaging and testing, discrete devices, sensors, optoelectronic devices), photovoltaic industry chain (equipment, cells, modules, auxiliary material brackets, inverters, power station terminals), new energy automobile industry chain (batteries and materials, auto parts, batteries, motors, electronic control, automotive semiconductors, etc.), communication industry chain (communication system equipment, terminal equipment, electronic components, RF front-end, optical modules, 4G/5G/6G, broadband, IoT, digital economy, AI), advanced materials industry Chain (metal materials, polymer materials, ceramic materials, nano materials, etc.), machinery manufacturing industry chain (CNC machine tools, construction machinery, electrical machinery, 3C automation, industrial robots, lasers, industrial control, drones), food, beverages and pharmaceuticals, medical equipment, agriculture, etc.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp