Automated Spectrum Management System Market Summary

An Automated Spectrum Management System is a sophisticated technological solution designed to efficiently manage and optimize the use of radio frequency (RF) spectrum resources. It utilizes advanced algorithms, sensors, and software to automatically monitor, analyze, and control the spectrum. By continuously tracking the presence and activity of various RF signals, it can detect interference, identify unused or underutilized spectrum bands, and allocate frequencies to different users or services in a dynamic and intelligent manner. This system plays a crucial role in ensuring seamless communication in a wide range of applications, from mobile networks and wireless local area networks to military and aerospace communications. It helps in enhancing the overall performance of communication systems, reducing interference, and maximizing the utilization of the limited spectrum resources. With the ever-increasing demand for wireless connectivity and the proliferation of various wireless devices, an Automated Spectrum Management System has become an essential tool for maintaining the efficiency and reliability of modern communication infrastructure.

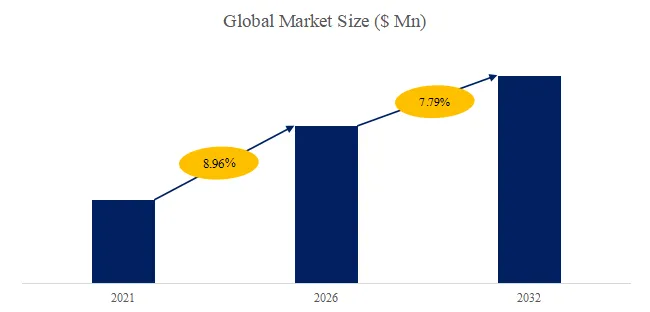

According to the new market research report “Global Automated Spectrum Management System Market Report 2026-2032″, published by QYResearch, the global Automated Spectrum Management System market size is projected to grow from USD 503.12 million in 2026 to USD 789.33 million by 2032, at a CAGR of 7.79% during the forecast period.

Figure00001. Global Automated Spectrum Management System Market Size (US$ Million), 2021-2032

Above data is based on report from QYResearch: Global Automated Spectrum Management System Market Report 2026-2032 (published in 2025). If you need the latest data, plaese contact QYResearch.

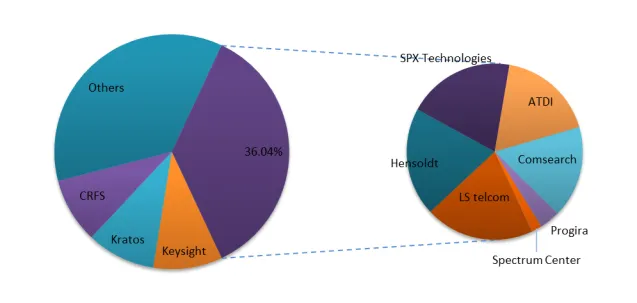

Figure00002. Global Automated Spectrum Management System Top 10 Players Ranking and Market Share (Ranking is based on the revenue of 2025, continually updated)

Above data is based on report from QYResearch: Global Automated Spectrum Management System Market Report 2026-2032 (published in 2025). If you need the latest data, plaese contact QYResearch.

This report profiles key players of Automated Spectrum Management System such as Keysight, Kratos, CRFS.

In 2025, the global top three Automated Spectrum Management System players account for 28% of market share in terms of revenue. Above figure shows the key players ranked by revenue in Automated Spectrum Management System.

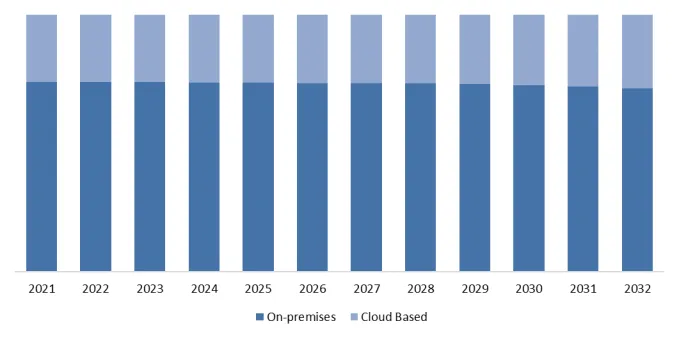

Figure00003. Automated Spectrum Management System, Global Market Size, Split by Product Segment

Based on or includes research from QYResearch: Global Automated Spectrum Management System Market Report 2026-2032.

In terms of product type, type one is the largest segment, hold a share of xx%,

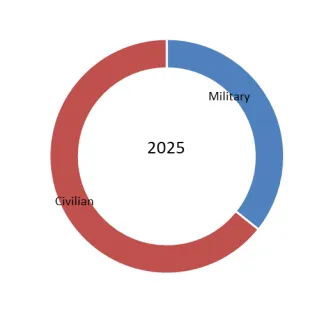

Figure00004. Automated Spectrum Management System, Global Market Size, Split by Application Segment

Based on or includes research from QYResearch: Global Automated Spectrum Management System Market Report 2026-2032.

In terms of product application, application one is the largest application, hold a share of 64%,

About The Authors

| Zhang Haijing is the main analyst of this article.

zhanghaijing@qyresearch.com

Ms. Zhang has 4 years of experience in industry data analysis, focusing on the research of metalens, ultra-low temperature fans, electronics and communication industry chain related fields. Mainly responsible for the collection, organization, analysis, and data processing of product and market information.

|

About QYResearch

QYResearch founded in California, USA in 2007.It is a leading global market research and consulting company. With over 17 years’ experience and professional research team in various cities over the world QY Research focuses on management consulting, database and seminar services, IPO consulting (data is widely cited in prospectuses, annual reports and presentations), industry chain research and customized research to help our clients in providing non-linear revenue model and make them successful. We are globally recognized for our expansive portfolio of services, good corporate citizenship, and our strong commitment to sustainability. Up to now, we have cooperated with more than 60,000 clients across five continents. Let’s work closely with you and build a bold and better future.

QYResearch is a world-renowned large-scale consulting company. The industry covers various high-tech industry chain market segments, spanning the semiconductor industry chain (semiconductor equipment and parts, semiconductor materials, ICs, Foundry, packaging and testing, discrete devices, sensors, optoelectronic devices), photovoltaic industry chain (equipment, cells, modules, auxiliary material brackets, inverters, power station terminals), new energy automobile industry chain (batteries and materials, auto parts, batteries, motors, electronic control, automotive semiconductors, etc.), communication industry chain (communication system equipment, terminal equipment, electronic components, RF front-end, optical modules, 4G/5G/6G, broadband, IoT, digital economy, AI), advanced materials industry Chain (metal materials, polymer materials, ceramic materials, nano materials, etc.), machinery manufacturing industry chain (CNC machine tools, construction machinery, electrical machinery, 3C automation, industrial robots, lasers, industrial control, drones), food, beverages and pharmaceuticals, medical equipment, agriculture, etc.

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 18 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp