Introduction – Addressing Core Industry Pain Points

Perovskite solar cell (PSC) researchers and manufacturers face three persistent challenges with conventional deposition methods: spin-coating wastes >90% of precursor ink (unsuitable for large-area production), slot-die coating requires expensive masks and generates material waste, and vacuum-based methods (thermal evaporation, sputtering) have high capital and operating costs. Inkjet Printing Systems for Perovskite Solar Cells – advanced, non-contact deposition technologies used to precisely pattern and deposit perovskite precursor inks onto substrates during solar cell fabrication – solve these problems through digital, material-efficient manufacturing. This method enables scalable, digital, and material-efficient manufacturing by allowing controlled droplet-by-droplet delivery of functional inks, which can form uniform, defect-free perovskite films after subsequent drying and crystallization processes. Inkjet printing is particularly attractive for large-area, flexible, or patterned solar cells, and supports roll-to-roll processing, making it a promising approach for commercial-scale production of high-efficiency perovskite photovoltaics. For PSC researchers, pilot line operators, and solar cell manufacturers, the critical decisions now center on system scale (Small Laboratory Type vs. Large Production Type), application (Solar Cells, LEDs, Others), and the printhead technology/ink formulation that balances resolution, throughput, and film uniformity.

Global Leading Market Research Publisher QYResearch announces the release of its latest report “Inkjet Printing Systems for Perovskite Solar Cells – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032″. Based on current situation and impact historical analysis (2021-2025) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Inkjet Printing Systems for Perovskite Solar Cells market, including market size, share, demand, industry development status, and forecasts for the next few years.

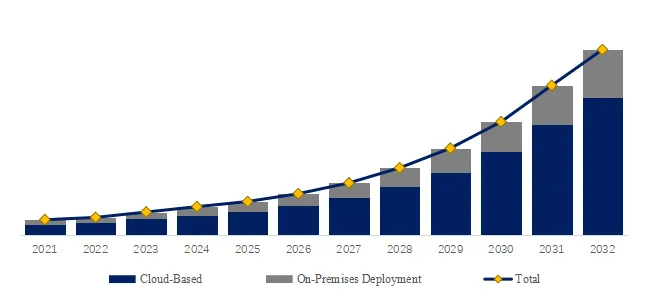

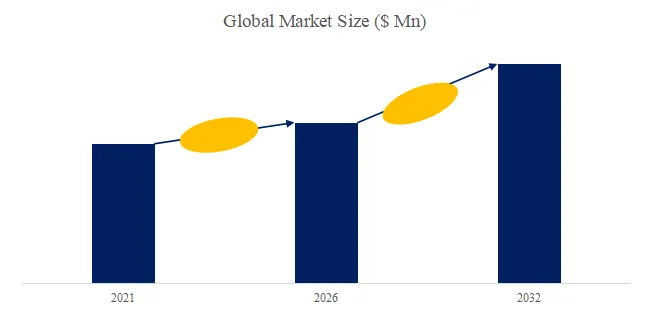

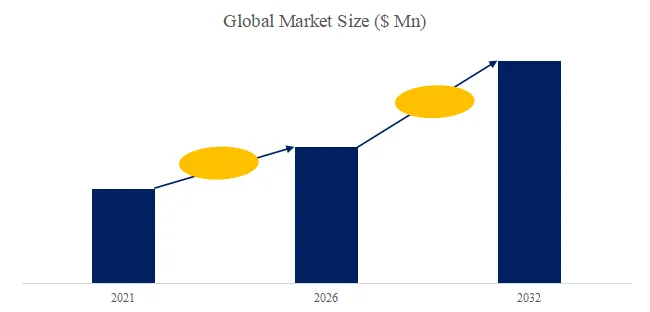

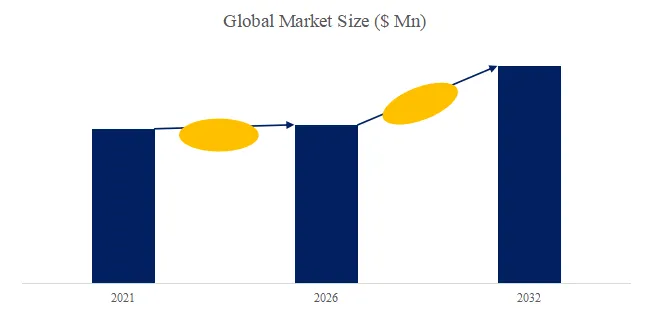

The global market for Inkjet Printing Systems for Perovskite Solar Cells was estimated to be worth US$ 2.44 million in 2025 and is projected to reach US$ 6.48 million by 2032, growing at a CAGR of 15.2% from 2026 to 2032. Inkjet printing systems for perovskite solar cells are advanced, non-contact deposition technologies used to precisely pattern and deposit perovskite precursor inks onto substrates during solar cell fabrication. This method enables scalable, digital, and material-efficient manufacturing by allowing controlled droplet-by-droplet delivery of functional inks, which can form uniform, defect-free perovskite films after subsequent drying and crystallization processes. Inkjet printing is particularly attractive for large-area, flexible, or patterned solar cells, and supports roll-to-roll processing, making it a promising approach for commercial-scale production of high-efficiency perovskite photovoltaics.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)

https://www.qyresearch.com/reports/6094534/inkjet-printing-systems-for-perovskite-solar-cells

Market Segmentation – Key Players, System Scales, and Applications

The Inkjet Printing Systems for Perovskite Solar Cells market is segmented as below by key players:

Key Manufacturers (Inkjet Deposition Specialists):

- MicroFab – US pioneer in inkjet printing for research (piezoelectric drop-on-demand).

- Gosan Tech – Korean inkjet printing systems.

- Elephantech – Japanese inkjet manufacturing.

- DJK – Inkjet systems.

- M-SOLV – UK inkjet printing solutions (perovskite and OLED).

- Suzhou Guangsu Technology – Chinese inkjet printing systems for photovoltaics.

Segment by Type (System Scale / Throughput):

- Small Laboratory Type – Research-scale systems (single-nozzle or multi-nozzle printheads, 100x100mm substrate). Used for ink formulation development, process optimization, and small-area cell fabrication. Largest segment by unit volume (~70% market share).

- Large Production Type – Pilot or production-scale systems (industrial printheads, roll-to-roll or sheet-fed, up to 300mm web width). Used for pilot production and commercial-scale manufacturing. Smaller unit volume but higher ASP (~30% market share, 18% CAGR).

Segment by Application (End-Use Device):

- Solar Cells – Largest segment (~80% market share). Perovskite solar cells (single-junction, tandem, flexible).

- LEDs – Perovskite LEDs (PeLEDs) for displays and lighting (~10% market share).

- Others – Photodetectors, sensors, memristors, and other perovskite-based electronic devices (~10%).

New Industry Depth (6-Month Data – Late 2025 to Early 2026)

- Perovskite solar cell efficiency record – In December 2025, NREL reported a certified 26.8% efficiency for a small-area (0.1 cm²) perovskite cell fabricated using inkjet-printed perovskite layer (Helmholtz-Zentrum Berlin). This validates inkjet as a viable deposition method for high-efficiency cells.

- Roll-to-roll inkjet commercialization – In January 2026, M-SOLV announced a roll-to-roll inkjet printing system for perovskite solar cells (300mm web width, 10 m/min), targeting pilot production of flexible perovskite modules.

- Discrete vs. process manufacturing realities – Unlike process manufacturing (e.g., continuous slot-die coating), inkjet printing system production involves discrete printhead assembly, drop ejection calibration, and substrate motion control – each system is individually calibrated for drop volume, velocity, and placement accuracy. This creates unique challenges:

- Printhead manufacturing – Piezoelectric actuators (100-1,000+ nozzles) bonded to nozzle plate. Nozzle diameter 20-50 microns. Each printhead tested for drop uniformity.

- Drop ejection calibration – Drive waveform (voltage, pulse width) tuned for specific perovskite ink (viscosity 5-15 cP). Drop volume (2-50 pL) and velocity (3-10 m/s) verified by strobe visualization.

- Substrate positioning – XY stage or roll-to-roll transport accuracy ±5-10 microns. Encoder feedback calibrated per axis.

- Drying and crystallization integration – Inkjet systems often integrated with hotplates, vacuum, or gas flow for film drying. Temperature uniformity across platen ±1°C.

- Defect detection – Inline camera inspection for missing drops, satellite drops, or misdirection. Reject criteria set per application.

Typical User Case – University Perovskite Research Lab (US, 2026)

A US university research lab (perovskite photovoltaics) purchased a small laboratory inkjet system (MicroFab, single-nozzle, 50 pL drop volume) for perovskite ink development. Results after 12 months:

- Material utilization: >95% (inkjet) vs. <10% (spin-coating) – dramatic reduction in precious precursor waste

- Pattern flexibility: ability to print graded compositions, multi-layer structures without masks

- Publications: 3 papers using inkjet-deposited perovskite layers (previously 0)

- System cost: $50,000 (inkjet) vs. $500 (spin-coater) – 100x higher, but enabled new research directions

The technical challenge overcome: preventing nozzle clogging (perovskite inks contain solvents that evaporate quickly, leaving solids). The solution involved a humidified printhead environment (sealed chamber with solvent vapor saturation) and automated purging cycles. This case demonstrates that small laboratory type inkjet systems enable advanced perovskite research despite higher capital cost.

Exclusive Insight – The “Lab vs. Production System Market Dynamics”

Industry analysis often treats laboratory and production systems as a continuum. However, market segmentation analysis (Q1 2026) reveals distinct customer profiles and requirements:

| Parameter | Small Laboratory Type | Large Production Type |

|---|---|---|

| Substrate size | <100 x 100 mm | Up to 300mm web width or sheet |

| Throughput | Manual (1-10 substrates/day) | Semi/fully automated (10-100 m²/hour) |

| Printhead nozzles | 1-256 | 1,000-10,000+ |

| Drop volume | 2-50 pL | 10-100 pL |

| Placement accuracy | ±5-10 μm | ±20-50 μm |

| Price range | $20,000-150,000 | $500,000-5,000,000+ |

| Typical customer | University labs, research institutes | Pilot lines, commercial manufacturers |

| Market share (units) | ~70% | ~30% |

| Market share (value) | ~40% | ~60% |

The key insight: small lab systems drive unit volume (70% of units) for research. Large production systems drive revenue (60% of market value) for commercial scale-up. The transition from lab to production is a key inflection point for perovskite commercialization.

Policy and Technology Outlook (2026-2032)

- US DOE Solar Energy Technologies Office (SETO) funding – $5 million allocated for inkjet-printed perovskite modules (2025-2027), supporting scale-up from lab to pilot production.

- EU Horizon Europe (PERPRINT project) – €8 million for roll-to-roll inkjet printing of perovskite solar cells (2024-2028), targeting 25% efficiency on flexible substrates.

- China’s “14th Five-Year Plan” for renewable energy – Perovskite solar cells identified as a strategic technology, with inkjet printing as a priority deposition method for large-area modules.

- Next frontier: multi-nozzle inkjet for high-throughput production – Research prototypes (2026) use 10,000+ nozzle printheads (page-wide arrays) achieving 100 m²/hour throughput, comparable to slot-die coating.

Conclusion

The Inkjet Printing Systems for Perovskite Solar Cells market is small but growing rapidly (15.2% CAGR), driven by the need for material-efficient, scalable deposition methods for perovskite photovoltaics. Small Laboratory Type systems dominate unit volume (70%) for research and development. Large Production Type systems drive revenue (60% of market value) for pilot and commercial production. Solar cells are the dominant application (80% of market). The discrete, high-precision manufacturing nature of inkjet printing systems – printhead assembly, drop ejection calibration, substrate positioning – favors specialized instrumentation companies (MicroFab, M-SOLV, Elephantech, Suzhou Guangsu). For 2026-2032, the winning strategy is offering both lab-scale and production-scale systems, developing perovskite-specific printhead and ink formulations (to prevent nozzle clogging), and integrating drying/crystallization modules for turnkey processing.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp

Vector Search Engine, Global Market Size, Split by Product Segment

Vector Search Engine, Global Market Size, Split by Product Segment