Introduction (Covering Core User Needs: Pain Points & Solutions):

Global Leading Market Research Publisher QYResearch announces the release of its latest report “Leno Bag – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032″. Based on current situation and impact historical analysis (2021-2025) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Leno Bag market, including market size, share, demand, industry development status, and forecasts for the next few years.

For farmers, produce packers, and agricultural cooperatives, packaging fresh fruits and vegetables presents a fundamental challenge: sealed plastic bags trap moisture, accelerate spoilage, and promote mold growth; traditional jute or paper bags lack durability, are heavy, and cannot be reused. A leno bag is a type of mesh or open-weave bag typically made from polypropylene material. It features a distinctive diamond-patterned mesh construction that allows for breathability and visibility of the contents inside. Leno bags are widely used in agriculture, particularly for packaging and transporting fresh produce such as fruits, vegetables, and potatoes. The open design promotes air circulation, reducing the risk of moisture buildup and mold growth, thus helping to maintain the freshness and quality of the packaged items. Leno bags are a cost-effective, reusable, and sustainable packaging solution suitable for various agricultural and industrial purposes. As global fresh produce trade expands, post-harvest loss reduction becomes a priority (UN FAO targets 50% reduction by 2030), and consumers demand sustainable packaging, leno bags are transitioning from traditional jute/paper to modern synthetic mesh packaging.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)

https://www.qyresearch.com/reports/5985593/leno-bag

1. Market Sizing & Growth Trajectory (With 2026–2032 Forecasts)

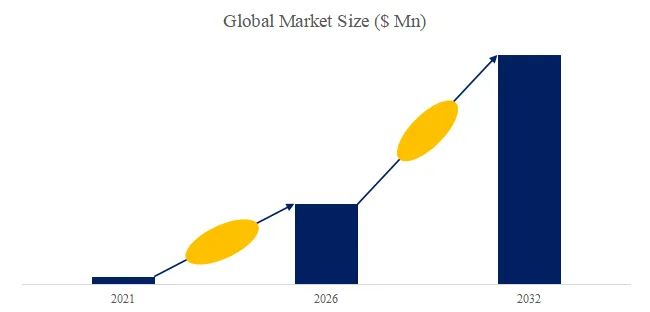

The global market for Leno Bag was estimated to be worth approximately US$1,500 million in 2025 and is projected to reach US$2,000 million by 2032, growing at a CAGR of 4.2% from 2026 to 2032. This steady growth is driven by three converging factors: (1) increasing global production of potatoes, onions, citrus fruits, and vegetables, (2) shift from jute and paper to polypropylene mesh packaging, and (3) demand for reusable and recyclable agricultural packaging.

By material type, PP leno bags dominate with approximately 80% of market revenue (lowest cost, good strength, UV resistance). PE leno bags account for 10% (softer, more flexible, lower strength), PA (nylon) leno bags for 5% (higher strength, higher cost), and others for 5%. By application, fruit packaging (citrus, apples, oranges, lemons, grapefruit) accounts for approximately 45% of market revenue, vegetable packaging (potatoes, onions, garlic, carrots, tomatoes) for 50%, and others for 5%.

2. Technology Deep-Drive: Mesh Construction, UV Stabilization, and Reusability

Technical nuances often overlooked:

- Breathable mesh produce bags construction: Woven polypropylene (PP) tape (width 2-5mm, denier 500-2,000). Mesh size (aperture): 5-25 mm. Open area: 30-70% (ventilation, visibility). Basis weight: 30-120 g/m². Tensile strength: 500-2,000 N/50mm. Elongation: 10-30%. UV stabilizers for outdoor storage (6-12 months). Food-grade PP (no heavy metals, no phthalates).

- Diamond-pattern polypropylene packaging benefits: Moisture evaporation (prevents rot, mold). Temperature regulation (reduces heat buildup). Visibility (inspect contents without opening). Lightweight (reduces transport cost). Reusable (multiple harvest cycles). Recyclable (PP recycling streams). Custom printing available.

Recent 6-month advances (October 2025 – March 2026):

- CTM Technical Textiles launched “CTM Leno Bag” – PP mesh, UV stabilized, 50-100 g/m². For potato and onion packaging. Price US$0.10-0.50 per bag.

- Trinity Packaging introduced “Trinity Leno Bag” – PE leno bag (softer, flexible), for delicate fruits (peaches, plums, tomatoes). Price US$0.12-0.55 per bag.

- Singhal Industries commercialized “Singhal Leno Bag” – PP mesh with custom printing (brand name, weight, origin). Price US$0.10-0.60 per bag.

3. Industry Segmentation & Key Players

The Leno Bag market is segmented as below:

By Material Type (Base Polymer):

- PP Leno Bag – Polypropylene. Low cost, high strength, UV resistant. Price: US$0.10-0.50 per bag. Largest segment.

- PE Leno Bag – Polyethylene. Softer, more flexible, lower strength. Price: US$0.12-0.55 per bag.

- PA Leno Bag – Polyamide (nylon). Higher strength, higher cost. Price: US$0.20-0.80 per bag.

- Others – Biodegradable PLA, jute, cotton. Price: US$0.30-1.00 per bag.

By Application (End-Use Sector):

- Fruit Packaging (citrus, apples, oranges, lemons, grapefruit, pomegranates) – 45% of 2025 revenue.

- Vegetable Packaging (potatoes, onions, garlic, carrots, tomatoes, peppers) – 50% of revenue, largest segment.

- Others (firewood, charcoal, recycling, industrial) – 5%.

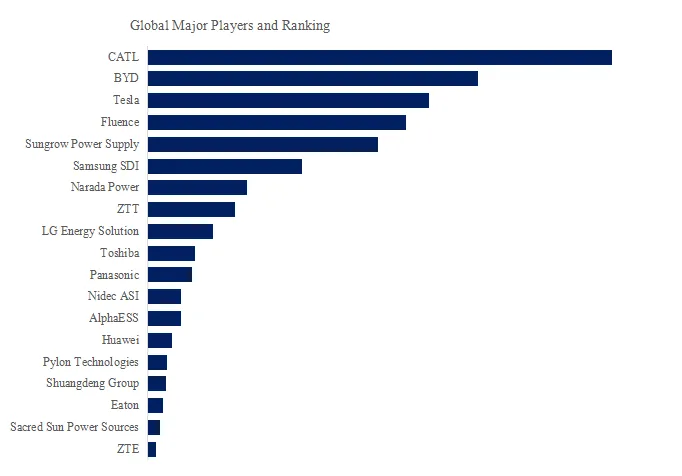

Key Players (2026 Market Positioning):

Global Leaders: Singhal Industries (India), CTM Technical Textiles (India), Trinity Packaging (India), LC Packaging (Netherlands), Meher International (India), Skill DyeChem (India), Balaajie Packaging (India), Kalna Hessian Bags Supply (India), Manokamna Polypack (India), Prime Industries (India), SPpFood Products (India), Pack World (India), Coderre Packaging (Canada), Megaflex Plastics (India).

独家观察 (Exclusive Insight): The leno bag market is fragmented with Singhal Industries (≈15-20% market share), CTM Technical Textiles (≈10-15%), and LC Packaging (≈10-15%) as top players. Singhal Industries (India) is the largest manufacturer (export to Europe, US, Middle East). CTM Technical Textiles (India) serves domestic and export markets. LC Packaging (Netherlands) is the largest Western manufacturer (Europe, Africa). India is the largest producer and exporter of leno bags (60-70% of global supply) due to low labor costs, abundant PP resin, and proximity to onion/potato producing regions. Leno bags are replacing jute bags (heavy, absorb moisture, mold-prone) and paper bags (tear easily, not reusable). Shelf life extension: onions stored in leno bags last 3-6 months vs. 1-2 months in plastic bags (reduced rot). UV stabilization is critical for outdoor storage (6-12 months without degradation). Custom printing (brand name, weight, grade, origin) adds value (10-20% premium). Bag sizes: 5-50 kg capacity (standard 10-25 kg for retail, 25-50 kg for bulk). Color: natural (clear/translucent), white, green, orange (color-coding by product). Reusability: 5-10 harvest cycles (if handled carefully). End-of-life: recyclable in PP recycling streams (some municipal programs). Biodegradable alternatives (jute, cotton, PLA) are less durable, more expensive, or not yet scalable. The leno bag industry is currently witnessing several notable trends. Firstly, there is an increasing demand for eco-friendly and biodegradable materials in response to environmental concerns. Manufacturers are exploring sustainable alternatives to traditional polypropylene for leno bag production. Secondly, customization and branding are gaining importance as companies look to distinguish their products with unique designs and logos on leno bags. Thirdly, the adoption of advanced printing technologies is on the rise to create high-quality, eye-catching graphics and labeling on the bags. Lastly, the continued expansion of the agricultural and retail sectors drives the overall growth.

4. User Case Study & Policy Drivers

User Case (Q1 2026): Dole Food Company (USA) – fresh produce. Dole adopted Singhal leno bags for citrus fruit packaging (2025). Key performance metrics vs. plastic bags:

- Post-harvest loss (rot, mold): 5% (leno) vs. 10% (plastic) – 50% reduction

- Bag weight: 50g (leno) vs. 100g (plastic) – 50% lighter, lower transport cost

- Reusability: 5 harvests (leno) vs. 1 harvest (plastic) – 5× longer life

- Cost per bag: US$0.30 (leno) vs. US$0.20 (plastic) – 50% premium, justified by loss reduction and reusability

- Customer satisfaction (retailers): 95% (leno) vs. 85% (plastic) – improved

Policy Updates (Last 6 months):

- UN FAO – Post-harvest loss reduction (December 2025): Targets 50% reduction in post-harvest loss by 2030. Leno bags (ventilation) recognized as best practice for potatoes, onions, citrus.

- EU Single-Use Plastics Directive – Agricultural packaging (January 2026): Exempts reusable agricultural packaging (leno bags) from single-use plastic bans. Encourages reuse (5+ cycles).

- India Ministry of Agriculture – Onion storage scheme (November 2025): Subsidizes leno bags for onion farmers (50% subsidy). Domestic manufacturers (Singhal, CTM, Trinity, Meher, Skill DyeChem, Balaajie, Kalna, Manokamna, Prime, SPpFood, Pack World, Coderre, Megaflex) benefit.

5. Technical Challenges and Future Direction

Despite steady growth, several technical challenges persist:

- UV degradation: Polypropylene degrades under prolonged UV exposure (6-12 months). UV stabilizers (HALS, benzophenone) extend life to 12-24 months but add cost (10-20%). Non-UV-stabilized bags become brittle, crack.

- Drawstring durability: Drawstring (if present) may break under tension (overfilling, rough handling). Reinforced drawstrings (woven, thicker) add cost (5-10%).

- Recycling contamination: Leno bags are recyclable but often contaminated with produce residue (dirt, organic matter). Washing required before recycling (adds cost, water usage). Many bags end up in landfill.

独家行业分层视角 (Exclusive Industry Segmentation View):

- Discrete export and bulk agricultural applications (onion/garlic export, potato storage, citrus packing) prioritize UV stabilization, high tensile strength, and custom printing. Typically use Singhal, CTM, Trinity, LC Packaging, Meher, Skill DyeChem, Balaajie, Kalna, Manokamna, Prime, SPpFood, Pack World, Coderre, Megaflex. Key drivers are durability and shelf life extension.

- Flow process local market and consumer applications (farmers markets, retail produce) prioritize low cost (US$0.10-0.30 per bag), drawstring convenience, and color-coding. Typically use regional manufacturers. Key performance metrics are cost per bag and breakage rate.

By 2030, leno bags will evolve toward biodegradable mesh bags (PLA, PHA) and smart bags with RFID tracking. Prototype biodegradable leno bags (PLA) available but higher cost (2-3× PP) and lower strength. RFID-enabled bags for traceability (farm to fork) in development. As breathable mesh produce bags become standard for fresh produce and diamond-pattern polypropylene packaging reduces post-harvest loss, leno bags will remain essential for global agriculture.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666 (US)

JP: https://www.qyresearch.co.jp