Introduction – Addressing Core Industry Pain Points

The global swine production industry faces a persistent challenge: maximizing genetic improvement through artificial insemination (AI) while maintaining boar welfare, semen quality, and collection efficiency. Traditional semen collection methods (manual collection from live sows or dummy sows) can be stressful for boars, leading to reduced libido, lower semen volume, decreased sperm quality, and increased labor requirements. Commercial boar studs, genetic companies, and large-scale swine operations increasingly demand boar semen collection stations—specialized equipment designed to simulate natural mating conditions. The appearance of the semen collection platform is visually stimulating to satisfy the boar. Sow sound induction during estrus (recorded vocalizations) reduces the boar’s reaction time, improves the boar’s comfort during collection, and increases semen quality and quantity. These stations improve worker safety (reducing injury risk from aggressive boars), standardize collection procedures, and enhance genetic dissemination through AI. Global Leading Market Research Publisher QYResearch announces the release of its latest report “Boar Semen Collection Station – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032″. Based on current situation and impact historical analysis (2021-2025) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Boar Semen Collection Station market, including market size, share, demand, industry development status, and forecasts for the next few years.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart) 】

https://www.qyresearch.com/reports/5986025/boar-semen-collection-station

Market Sizing & Growth Trajectory

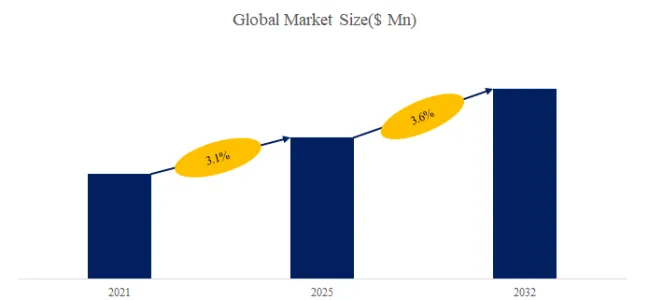

The global market for Boar Semen Collection Station was estimated to be worth US$ million in 2025 and is projected to reach US$ million, growing at a CAGR of % from 2026 to 2032. According to QYResearch’s interim tracking (January–June 2026), the market is driven by: (1) global expansion of artificial insemination in swine (estimated 90%+ of commercial sows in developed countries, 60-70% in emerging markets), (2) consolidation of boar studs (larger, centralized facilities with 200-1,000+ boars), (3) focus on genetic improvement and disease control (biosecurity). The large station segment dominates (60-65% market share), used by commercial boar studs and genetic companies, with small stations (35-40%) serving private farms and smaller operations. Company (commercial/stud) application accounts for 70-75% of demand, private (individual farm) 25-30%.

独家观察 – Semen Collection Station Design and Functionality

Boar semen collection stations are engineered to optimize collection efficiency, boar welfare, and semen quality:

| Feature | Functional Benefit | Impact on Semen Collection |

|---|---|---|

| Visual simulation (dummy sow appearance) | Reduces boar anxiety, encourages mounting | Faster collection time (3-5 minutes vs. 5-10 minutes manual) |

| Estrus sound induction (recorded sow vocalizations) | Triggers natural mounting behavior | Reduces false starts, increases collection success rate (95%+ vs. 80-85% manual) |

| Adjustable height/angle | Accommodates different boar sizes (200-400 kg) | Reduces injury risk, improves boar comfort |

| Non-slip surface | Stable footing during collection | Increases boar confidence, reduces falls |

| Easy-clean materials (stainless steel, antimicrobial) | Biosecurity, disease prevention | Reduces pathogen transmission between boars |

| Semen collection dummy mount | Standardized collection position | Improves technician ergonomics, reduces labor strain |

From a discrete manufacturing perspective (fabricated equipment), semen collection stations differ from general livestock handling equipment through: (1) ergonomic design for boar anatomy, (2) acoustic components (speakers for estrus calls), (3) material selection (non-porous, chemical-resistant for disinfection), (4) portability options (wheeled or fixed installation), (5) compatibility with automated semen collection systems (emerging).

Six-Month Trends (H1 2026)

Three trends reshape the market: (1) Automated semen collection integration – Robotic collection systems (emerging) reducing labor requirements, standardizing collection technique; early adopters report 30-40% labor reduction; (2) Biosecurity-enhanced designs – COVID-19 and African swine fever (ASF) concerns driving demand for stations with enhanced cleanability, separate entry/exit zones, and antimicrobial surfaces; (3) Data collection integration – RFID-enabled stations tracking individual boar performance (collection frequency, volume, sperm quality trends) integrated with herd management software.

User Case Example – Commercial Boar Stud, United States

A 600-boar commercial stud in Iowa (supplying semen to 150,000 sows) replaced manual collection dummy sows with 24 large-format semen collection stations (POC and Shandong Zhubajie) from October 2025 to January 2026. Results (Q1 2026 vs. Q1 2025): average collection time reduced from 8.2 to 3.8 minutes per boar (54% reduction); semen volume per collection increased from 180mL to 225mL (25% increase); sperm concentration increased 12% (from 280M/mL to 315M/mL); boar rejection rate (refusal to mount) reduced from 12% to 3%; technician injury reports (from aggressive boars) reduced from 8 to 0. Annualized labor savings $78,000; increased semen doses sold (from 180,000 to 225,000 annually), generating $225,000 additional revenue.

Technical Challenge – Boar Welfare and Collection Consistency

A key technical challenge for boar semen collection stations is maintaining consistent collection performance across different boar breeds, ages, and temperaments:

| Challenge | Impact | Mitigation Strategy |

|---|---|---|

| Boar habituation | Reduced interest in station over time | Rotating estrus soundtracks, periodic retraining |

| Breed differences | Duroc, Landrace, Large White, Yorkshire have different mounting behaviors | Adjustable station dimensions, breed-specific training protocols |

| Age-related decline | Older boars (>3 years) may have reduced libido | Station design with easier access, lower mounting height |

| Temperament variability | Aggressive or timid boars | Soundproofing (reduces external distractions), consistent handling protocols |

| Seasonality | Reduced libido in hot weather (>25°C) | Cooling features (fans, shade, evaporative cooling) |

Leading stations incorporate: (1) modular design for breed/age adjustment, (2) multiple estrus sound tracks, (3) positive reinforcement compatibility (feed rewards post-collection), (4) climate control integration.

独家观察 – Large vs. Small Station Segmentation

| Parameter | Large Station | Small Station |

|---|---|---|

| Dimensions | 180-220 cm length, 80-100 cm width | 120-150 cm length, 60-80 cm width |

| Weight | 150-250 kg | 60-120 kg |

| Boar capacity | All sizes (200-400+ kg) | Small-medium boars (<300 kg) |

| Material | Heavy-gauge stainless steel, reinforced frame | Stainless steel or coated steel, lighter frame |

| Features | Estrus sound, adjustable height/angle, non-slip, wheels | Basic estrus sound (optional), fixed height |

| Price range | $2,500-6,000 | $800-2,200 |

| Primary users | Commercial boar studs (200+ boars), genetic companies | Private farms (10-50 boars), small studs |

| Expected lifespan | 10-15 years (heavy daily use) | 5-10 years (moderate use) |

| Key manufacturers | POC, Shandong Zhubajie, Zubaba | Dezhou Xinbaijia, small station variants |

Downstream Demand & Competitive Landscape

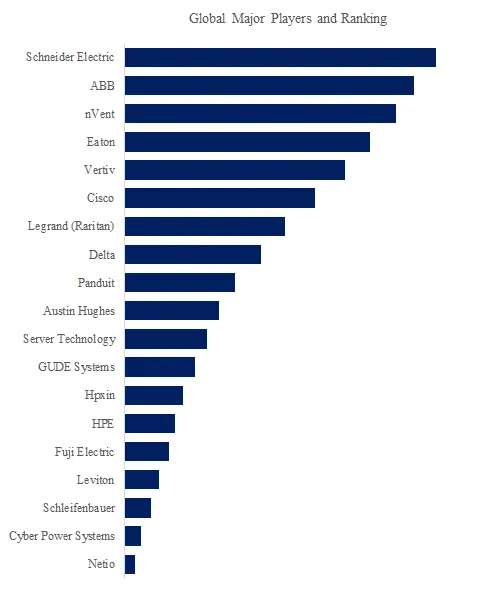

Applications span: Company (commercial boar studs, genetic supply companies, large-scale integrated swine operations – largest segment, 70-75% of market value), Private (individual pig farms, small breeding operations, research facilities – stable demand). Key players: POC (manufacturer, large stations), Shandong Zhubajie Animal Husbandry Machinery Co., Ltd. (China, full range), Zubaba (brand/supplier), Dezhou Xinbaijia (China, small stations). The market is concentrated in pork-producing regions (China, US, EU, Brazil, Canada, Vietnam) with China as largest manufacturer and consumer. Distribution is primarily through agricultural equipment dealers and direct sales.

Segmentation Summary

The Boar Semen Collection Station market is segmented as below:

Segment by Type – Large (commercial boar studs, high-volume, heavy-duty – dominant, 60-65%), Small (private farms, smaller operations – 35-40%)

Segment by Application – Company (commercial studs, genetic companies – 70-75%), Private (individual farms, research – 25-30%)

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp

Mobile Bearer Network, Global Market Size, Split by Product Segment

Mobile Bearer Network, Global Market Size, Split by Product Segment