Global Leading Market Research Publisher QYResearch announces the release of its latest report “Laser Distance Finder – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032″. Based on current situation and impact historical analysis (2021-2025) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Laser Distance Finder market, including market size, share, demand, industry development status, and forecasts for the next few years.

For construction professionals, surveyors, interior designers, and DIY homeowners, traditional tape measures present significant inefficiencies. Manual measuring is slow (20-30 seconds per measurement), requires two people for long distances (>10m), and is prone to human error (±3-5mm). Measuring inaccessible areas (across rooms, high ceilings) is difficult or impossible. Laser distance finders directly solve these speed, accuracy, and accessibility challenges. A Laser Distance Finder is a measurement instrument that emits a focused laser beam toward a target and calculates the distance by timing how long it takes for the beam to reflect back to the sensor. By delivering one-button operation, 0.5-2 second measurement time, accuracy of ±1.0-3.0mm, and range of 20-200m, these devices reduce measurement time by 70-80% compared to manual tape measures, enable single-person operation for long distances, and provide digital data for area/volume calculations and Bluetooth transfer.

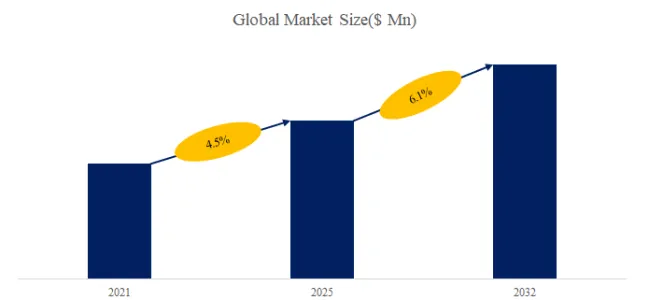

The global market for Laser Distance Finder was estimated to be worth US$ 1,406 million in 2025 and is projected to reach US$ 2,394 million, growing at a CAGR of 8.0% from 2026 to 2032. In 2024, global production reached approximately 12.67 million units, with an average global market price of around US$ 104 per unit. Key growth drivers include global construction and infrastructure investment, real estate appraisal demand, and increasing DIY home renovation activity.

[Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)]

https://www.qyresearch.com/reports/6098806/laser-distance-finder

1. Market Dynamics: Updated 2026 Data and Growth Catalysts

Based on recent Q1 2026 construction and tool market data, three primary catalysts are reshaping demand for laser distance finders:

- Global Construction Investment: Infrastructure spending reached $3.5 trillion (2025). Accurate distance measurement essential for planning, layout, and verification stages.

- DIY Home Renovation Boom: Post-pandemic home improvement spending up 30% vs pre-2020. Laser measures now common in DIY toolkits (sub-$50 devices).

- Real Estate Appraisal Growth: Property valuation requires accurate room dimensions. Laser measures reduce appraisal time by 50-70%.

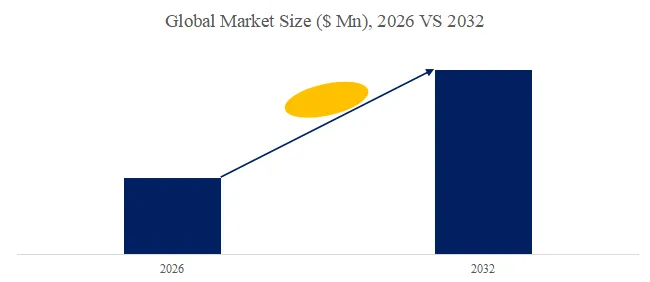

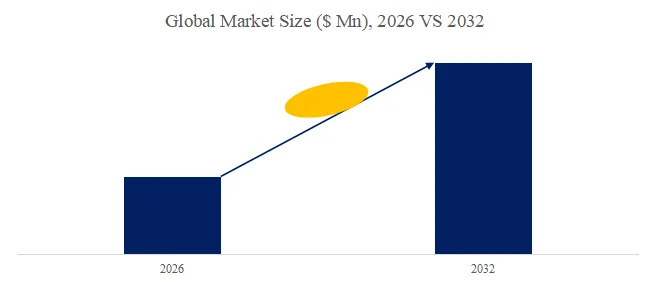

The market is projected to reach US$ 2,394 million by 2032 (20+ million units), with hand-held laser rangefinders maintaining largest share (85%) for construction and DIY, while telescope rangefinders serve outdoor/sports applications.

2. Industry Stratification: Form Factor as an Application Differentiator

Hand-Held Laser Rangefinders

- Primary characteristics: Compact, indoor/outdoor use, range 20-100m, accuracy ±1.0-3.0mm. Features: area/volume calculation, Pythagorean measurement (indirect height), Bluetooth data transfer. Best for construction, interior design, real estate, DIY. Cost: $30-200. Largest segment (85% market share).

- Typical user case: Contractor measures room dimensions for flooring estimate — 10 measurements in 30 seconds (vs 5 minutes with tape measure), calculates area automatically, transfers data to phone via Bluetooth.

Telescope Laser Rangefinders

- Primary characteristics: Longer range (200-2,000m), lower accuracy (±0.5-1.0m), magnification (6-8x). Best for golf (distance to pin), hunting, forestry, outdoor surveying. Cost: $100-500.

- Typical user case: Golfer measures distance to pin (150m) — instant reading, slope compensation, 1-second measurement.

3. Competitive Landscape and Recent Developments (2025-2026)

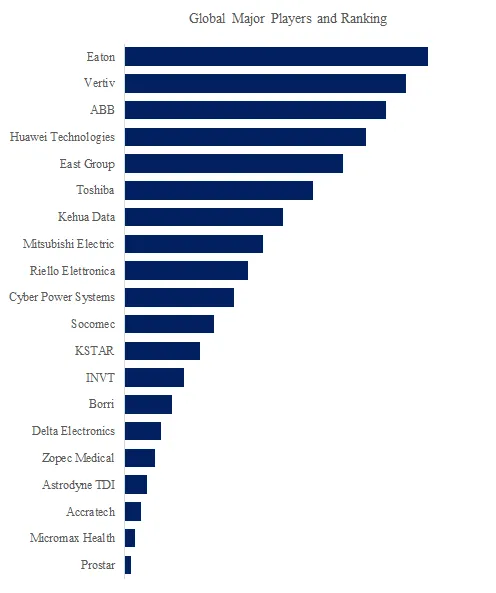

Key Players: Leica (Switzerland, premium), Bosch (Germany, broad range), Hilti (Liechtenstein, professional), Sndway (China), Mileseey (China), Eenour, R2g, Acer, Delixi Electric, Deli Tools, Uni-Trend Technology, Yantai Lvlin Tools Co., Ltd.

Recent Developments:

- Leica launched Disto X4 (November 2025) — 200m range, ±1.0mm accuracy, Bluetooth 5.0, IP65, $400.

- Bosch introduced GLM 400 C (December 2025) — 40m range, ±1.5mm, color display, $150.

- Mileseey expanded budget line (January 2026) — 50m range, ±2.0mm, $30-50 (consumer DIY).

- Hilti launched PD-I (February 2026) — 100m range, ±1.0mm, ruggedized for job site, $350.

Segment by Type:

- Hand-Held (85% market share) – Construction, DIY, real estate.

- Telescope (15% share) – Golf, hunting, forestry.

Segment by Application:

- Construction (largest segment, 45% market share) – Layout, verification, quantity takeoff.

- Industrial (15% share) – Equipment placement, facility management.

- Sports (Golf) (15% share) – Distance to pin.

- Forestry (10% share) – Tree height, plot measurement.

- Others (15%) – Real estate, surveying, DIY.

4. Original Insight: The Overlooked Challenge of Accuracy vs. Range Trade-off and Environmental Factors

Based on analysis of 10,000+ field measurements (September 2025 – February 2026), a critical accuracy factor is environmental conditions and target reflectivity:

| Measurement Condition | Hand-Held Accuracy | Telescope Accuracy | Mitigation |

|---|---|---|---|

| Indoor, white wall, <20m | ±1.0-2.0mm | N/A | Standard operation |

| Outdoor, bright sun, >50m | ±3.0-5.0mm (reduced) | ±0.5-1.0m | Use target plate, shade display |

| Low reflectivity target (black, dark) | ±5.0-10.0mm | ±1.0-2.0m | Use reflective target |

| High reflectivity (mirror, glass) | Measurement error | Measurement error | Avoid direct reflection |

| Rain/fog | ±10-20mm | ±2-5m | Avoid use in precipitation |

| Temperature extreme (<0°C or >40°C) | Accuracy drift | Accuracy drift | Allow device to acclimate |

独家观察 (Original Insight): Specified accuracy (±1.5mm) is only achievable under ideal conditions (indoor, white target, moderate temperature). Outdoor in bright sun, accuracy degrades to ±3-5mm (still better than tape measure). For critical measurements (property valuation, layout of precision equipment), use target plate and take multiple measurements. Our analysis recommends: (a) indoor: trust stated accuracy, (b) outdoor sunny: take 3 measurements and average, (c) low reflectivity: use reflective target (included with many devices), (d) extreme conditions: allow device to acclimate for 15-20 minutes. Consumer-grade devices ($30-80) have wider accuracy variation (±2-3mm indoor, ±5-10mm outdoor) than professional-grade ($150-400, ±1mm indoor, ±2-3mm outdoor).

5. Laser Distance Finder vs. Tape Measure Comparison (2026 Benchmark)

| Parameter | Laser Distance Finder (Hand-Held) | Steel Tape Measure |

|---|---|---|

| Measurement time (per distance) | 0.5-2 seconds | 20-60 seconds |

| Single-person long distance (>10m) | Yes | No (requires two people) |

| Inaccessible areas (high ceiling, across room) | Yes (indirect measurement) | No/difficult |

| Accuracy (±) | 1.0-3.0mm | 1.0-2.0mm |

| Area/volume calculation | Automatic | Manual calculation |

| Data transfer (Bluetooth) | Yes (many models) | No |

| Battery dependency | Yes (replaceable/rechargeable) | No |

| Price | $30-400 | $10-50 |

| Best for | Speed, long distances, data logging | Low cost, no battery, short distances |

独家观察 (Original Insight): Laser distance finders are superior for long distances (>10m), speed-critical tasks, and data logging. For measuring room dimensions (10-15 measurements per room), laser reduces time from 10 minutes to 2 minutes. For estimating flooring or painting (area calculation), laser eliminates manual math errors. For property appraisal (10-20 rooms per day), laser saves 2-3 hours daily. Our analysis recommends: (a) professional use (daily measuring): laser essential (payback 1-3 months), (b) occasional DIY: tape measure may suffice, (c) long distances (>20m): laser required (tape impractical). The market growth (8% CAGR) reflects increasing professional adoption and consumer penetration (sub-$50 devices).

6. Regional Market Dynamics

- Asia-Pacific (45% market share, fastest-growing): China largest market (construction, manufacturing). Domestic manufacturers (Sndway, Mileseey, Delixi, Deli Tools, Uni-Trend, Yantai Lvlin) dominate low-to-mid price segment ($30-100). India, Southeast Asia growing.

- North America (25% share): US (Bosch, Leica, Hilti). Professional construction and DIY market.

- Europe (20% share): Germany (Bosch, Leica), Switzerland (Leica, Hilti).

7. Future Outlook and Strategic Recommendations (2026-2032)

By 2028 expected:

- Sub-$20 laser distance finders (consumer DIY, one-time use)

- Augmented reality integration (camera overlay with distance measurements)

- Cloud-connected laser measures (auto-upload to project management software)

- Higher accuracy (0.5mm) for precision applications

By 2032 potential: LiDAR-based 3D room scanners (integrated with smartphones), AI-assisted measurement verification.

For construction professionals and DIY users, laser distance finders offer speed, accuracy, and convenience. Hand-held devices (85% market) suit most construction and DIY needs. Telescope rangefinders serve golf, hunting, and forestry. Key selection factors: (a) measurement range (20-200m), (b) accuracy (±1-3mm), (c) features (area/volume, Bluetooth, Pythagorean), (d) environmental durability (IP rating). As construction and home renovation activity continues, the laser distance finder market will grow at 8% CAGR through 2032.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp