Fully Automated Soldering Robot

A fully automated soldering robot is an automation system—typically a desktop/benchtop multi-axis robot or an in-line multi-axis/SCARA platform—that performs soldering operations using an iron tip, laser, or other localized heating method, combined with automatic solder wire feeding and programmable motion control. It is used to produce repeatable solder joints on PCBs, connectors, and wires, with controllable process parameters and reduced reliance on manual skills.

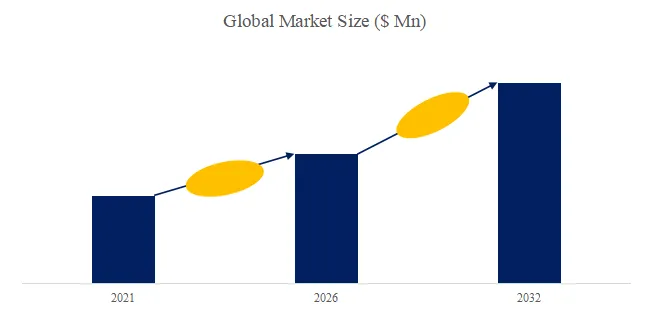

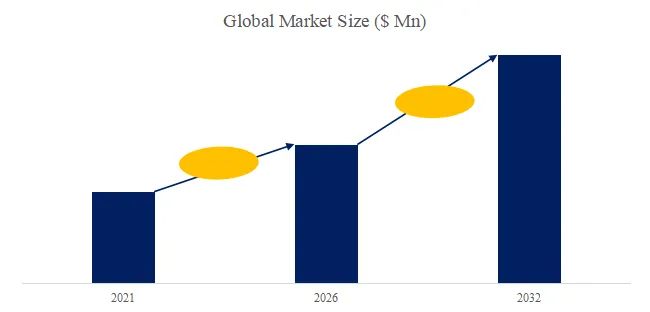

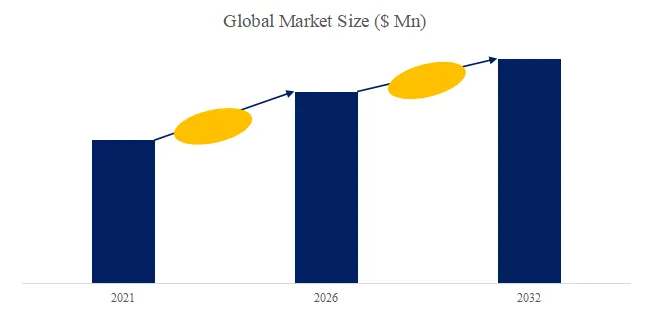

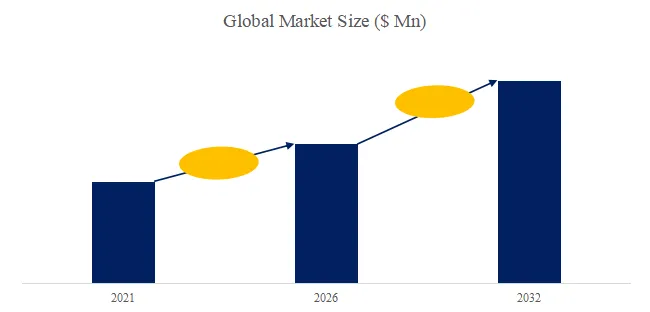

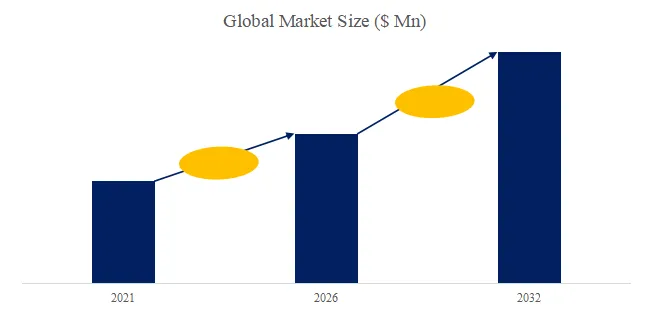

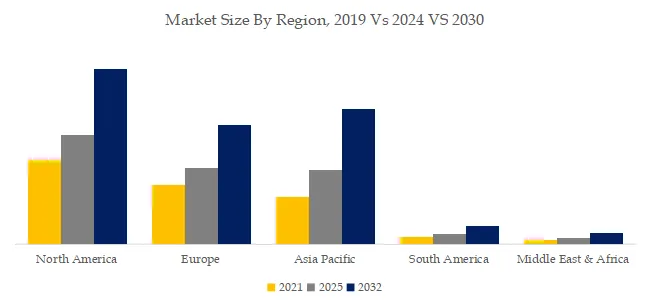

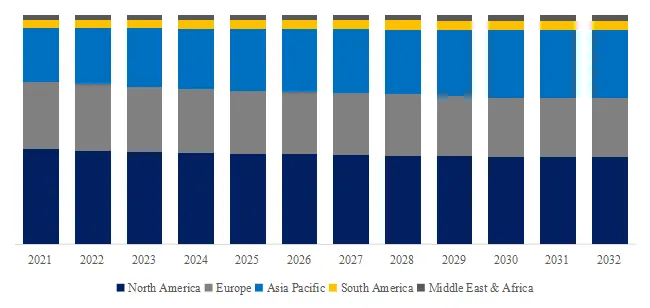

According to the latest QYResearch report, the global Fully Automated Soldering Robot market is expected to reach US$ 10403.72 million in 2025, with a compound annual growth rate (CAGR) of 3.5%.

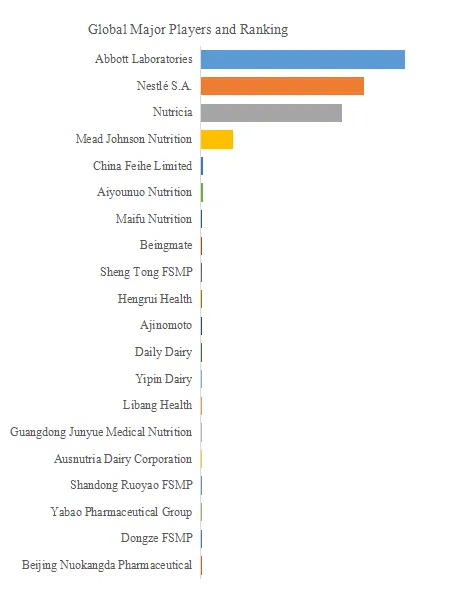

Manufacturing companies include Apollo Seiko, MTA Robotics, Unitechnologies Holding AG, Elmotec, Fanuc, ABB, KUKA, Kawasaki Heavy Industries, Nachi-Fujikoshi, Mitsubishi, Hyundai Robotics, Comau, Yamaha, Daihen, Stäubli, IGM Robotersysteme, Cloos Group, EFORT Group, Quick Intelligent, Estun Automation.

|

Company Name |

Description |

|

Apollo Seiko |

Apollo Seiko is a Japan-based specialist in automated soldering and joining technologies, widely recognized for its robotic soldering systems used in electronics manufacturing. The company provides integrated solutions combining soldering robots, control systems, solder feeders, and process know-how, supporting applications in automotive electronics, consumer electronics, industrial equipment, and precision components. Apollo Seiko is known for its high process stability, repeatability, and ability to meet stringent quality requirements in high-mix, high-reliability production environments. |

|

Mta Robotics |

MTA Robotics is an industrial automation company focused on robotic welding systems and customized robotic integration solutions. The company designs and delivers turnkey robotic cells for arc welding, spot welding, and special joining applications, serving industries such as automotive components, metal fabrication, machinery, and industrial equipment manufacturing. MTA Robotics emphasizes system engineering, process optimization, and flexible automation to improve productivity, weld quality, and manufacturing consistency. |

|

EFORT Group |

EFFORT a prominent high-tech company in the industrial robotics industry, has been listed on the Science and Technology Innovation Board since 2020. Ever since EFORT was founded, we have been committed to forward-looking strategic planning and relentless pursuit of core technologies. As a result, we have gradually become a well-known provider of robot solutions and intelligent manufacturing expertise in China. Our focus lies in developing a full range of robot products and offering cross-industry solutions for intelligent manufacturing. Through the integration of advanced global automation technology and experience, we have established a collaborative development model encompassing the entire industrial chain, which includes core robotic components, complete robot systems, and high-end robot system integration. |

|

Quick Intelligent |

Founded in 1993, QUICK is committed to becoming a leading global supplier of precision electronic assembly and back-end semiconductor packaging solutions. To create value for its customers, QUICK focuses on meeting their specific needs and application requirements, with a particular emphasis on reliability, high-quality products, technical expertise, and application knowledge. Over the years, it has earned an outstanding reputation based on numerous successful business cases and equipment deployments. |

Upstream includes motion/control (linear stages, servos/drives, controllers and software), soldering process modules (iron/laser/IH tool, automatic solder feeder, temperature control and tip cleaning, vision and fixturing), plus consumables (solder wire/alloys, flux). Representative materials suppliers include Indium Corporation (solder wire), AIM Solder (including robotic solder wire), Senju (soldering materials), and MacDermid Alpha (flux-cored wire/alloys). Downstream demand comes from electronics manufacturing and assembly (EMS/ODM, automotive electronics, industrial/medical/communications), covering through-hole point soldering, wire/connector soldering, localized rework, and flexible low-to-mid volume automation.

Market Drivers:

Market growth is driven by increasing demand for high-precision, consistent, and defect-free soldering in electronics, automotive electronics, and industrial equipment manufacturing. Rising labor costs, labor shortages, and stricter quality and traceability requirements accelerate the shift from manual soldering to fully automated solutions. In addition, miniaturization of electronic components, higher PCB density, and growing adoption of advanced packaging technologies require precise thermal control and repeatability that automated soldering robots can reliably deliver.

Restraint:

High initial investment and process integration complexity constrain adoption, particularly among small and mid-sized manufacturers. Fully automated soldering robots require precise programming, fixturing, and process optimization to accommodate product variations, increasing setup time and technical requirements. In addition, for low-volume or frequently changing production, manual or semi-automatic soldering may remain more cost-effective, limiting the addressable market in certain segments.

Opportunity:

Opportunities are emerging from the rapid growth of electric vehicles, renewable energy systems, smart appliances, and industrial IoT devices. These applications require reliable soldering for power electronics, sensors, and control modules, driving demand for high-performance automated soldering solutions. Integration with machine vision, AI-based process monitoring, and data analytics further enhances system capability, enabling adaptive soldering, predictive maintenance, and higher yield, particularly in smart factory and Industry 4.0 environments.

Barriers to Entry:

Barriers to entry are high due to the need for deep expertise in soldering processes, thermal management, robotics, and control software. New entrants must invest heavily in R&D, application engineering, and long-term process validation to meet stringent reliability and yield requirements. Established suppliers benefit from proprietary soldering know-how, extensive application libraries, and long-standing relationships with electronics manufacturers, making it difficult for newcomers to compete without clear technological differentiation or strong application focus.

About QYResearch

QYResearch founded in California, USA in 2007.It is a leading global market research and consulting company. With over 17 years’ experience and professional research team in various cities over the world QY Research focuses on management consulting, database and seminar services, IPO consulting (data is widely cited in prospectuses, annual reports and presentations), industry chain research and customized research to help our clients in providing non-linear revenue model and make them successful. We are globally recognized for our expansive portfolio of services, good corporate citizenship, and our strong commitment to sustainability. Up to now, we have cooperated with more than 60,000 clients across five continents. Let’s work closely with you and build a bold and better future.

QYResearch is a world-renowned large-scale consulting company. The industry covers various high-tech industry chain market segments, spanning the semiconductor industry chain (semiconductor equipment and parts, semiconductor materials, ICs, Foundry, packaging and testing, discrete devices, sensors, optoelectronic devices), photovoltaic industry chain (equipment, cells, modules, auxiliary material brackets, inverters, power station terminals), new energy automobile industry chain (batteries and materials, auto parts, batteries, motors, electronic control, automotive semiconductors, etc.), communication industry chain (communication system equipment, terminal equipment, electronic components, RF front-end, optical modules, 4G/5G/6G, broadband, IoT, digital economy, AI), advanced materials industry Chain (metal materials, polymer materials, ceramic materials, nano materials, etc.), machinery manufacturing industry chain (CNC machine tools, construction machinery, electrical machinery, 3C automation, industrial robots, lasers, industrial control, drones), food, beverages and pharmaceuticals, medical equipment, agriculture, etc.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp