Global Leading Market Research Publisher QYResearch announces the release of its latest report, *”Cables for Photovoltaic Power Generation Systems – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032.”* Based on current situation and impact historical analysis (2021-2025) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global cables for photovoltaic power generation systems market, including market size, share, demand, industry development status, and forecasts for the next few years.

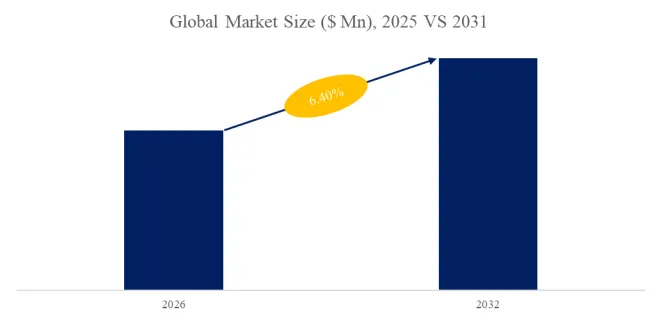

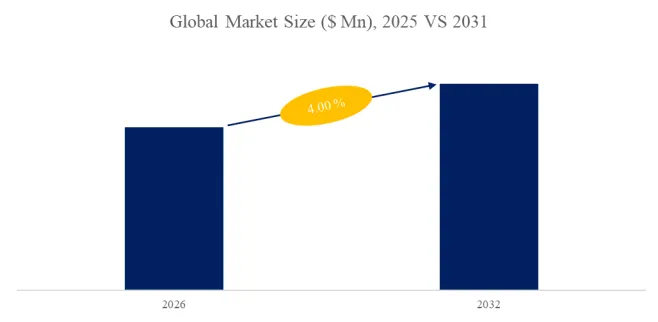

The global market for cables for photovoltaic power generation systems was estimated to be worth US6.5billionin2025andisprojectedtoreachUS6.5billionin2025andisprojectedtoreachUS 14.2 billion by 2032, growing at a CAGR of 11.8% from 2026 to 2032. For solar project developers, EPC contractors, and asset owners facing three critical pain points—fire safety risks from DC arc faults (responsible for 45% of PV system fires according to a 2024 industry analysis), premature cable degradation due to UV exposure in outdoor installations (typical service life of standard cables is only 10-15 years vs. 25+ year panel warranties), and voltage drop-induced energy losses (up to 3-5% of annual yield)—specialized cables for photovoltaic power generation systems offer essential solutions. These cables serve as the critical electrical interconnection between solar panels, inverters, batteries, controllers, and balance-of-system components, requiring specific electrical and environmental characteristics—including high-temperature resistance (up to 120°C), UV stability (accelerated aging test equivalent to 25 years), halogen-free low-smoke (HFFR) properties, and mechanical robustness (withstanding 10,000+ flex cycles).

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)

https://www.qyresearch.com/reports/5933116/cables-for-photovoltaic-power-generation-systems

1. Core Technology: DC Cable Engineering and Environmental Durability

Cables for photovoltaic power generation systems are broadly classified into DC cables (between panels, strings, and inverters) and AC cables (from inverter to grid connection). DC cables operate at higher voltage levels (1,500 V DC becoming standard in 2025, up from 1,000 V previously) and carry continuous current in outdoor, UV-exposed environments. Key technical requirements validated by recent testing (TÜV SÜD certification data, March 2025) include:

- UV Resistance: Cross-linked polyethylene (XLPO) insulation achieves 90% tensile strength retention after 2,500 hours of accelerated UV exposure (equivalent to 25 years in Central Europe), compared to 60% for standard PVC cables.

- Fire Safety: EN 50618:2025-compliant cables (effective January 2025 in EU) require flame propagation distance <1.5 meters per IEC 60332-1-2 and halogen-free smoke emission with peak optical density <2.0 per IEC 61034-2. Major manufacturers like Prysmian and Nexans have transitioned to HFFR compounds as standard.

- Temperature Endurance: Conductors rated for 90°C continuous (120°C for 20,000 hours) prevent thermal runaway in rooftop installations where surface temperatures exceed 80°C in summer.

Recent policy catalysts (2024-2025): China’s GB/T 40175-2025 standard (effective April 2025) mandates 25-year warranty for PV cables—requiring manufacturers to certify UV stability via 3,000-hour xenon-arc testing. The U.S. National Electric Code (NEC 2026 draft, released February 2025) proposes mandatory arc-fault circuit interruption (AFCI) monitoring integrated with DC cables for all residential PV systems >15 kW.

2. Market Segmentation by Cable Type and Application

The cables for photovoltaic power generation systems market is segmented below by electrical configuration and end-use sector:

Segment by Type:

| Cable Type | 2025 Market Share (%) | Voltage Range | Key Characteristics | Typical Applications |

|---|---|---|---|---|

| DC Cable | 68 | 600-1,500 V DC | Double insulation, UV-resistant, flexible | String connections, panel-to-inverter |

| AC Cable | 32 | 230-1,000 V AC | Armored option, lower insulation thickness | Inverter-to-grid, building interface |

Segment by Application:

- Residential Photovoltaic System (22% of 2025 demand): Rooftop installations (3-10 kW). Case study: Sumitomo Electric Industries supplied 5,000 km of DC cables for 200,000 Japanese residential systems installed under FIT revision (April 2024-March 2025). After one year, field failure rate was 0.03% (vs. 0.21% for non-specialized cables), attributed to enhanced UV-stabilized XLPE insulation.

- Industrial Photovoltaic System (38%): Large-scale ground-mount (10-100+ MW). Example: Jiangsu Zhongtian Technology completed supply of 1,200 km of 1,500 V DC cables for the 500 MW Golmud solar park in Qinghai (December 2024). DC voltage boost from 1,000 V to 1,500 V reduced cable weight by 28% and aluminum conductor volume by 22%—saving US$ 4.2 million in material costs.

- Commercial Photovoltaic System (32%): Carport, warehouse rooftop, and C&I ground-mount (100 kW-10 MW). LS Cable & System’s aluminium-alloy DC cable (announced January 2025) reduces weight by 45% compared to copper, enabling easier rooftop installation without structural reinforcement.

- Others (8%): BIPV (building-integrated PV), floating solar, and agrivoltaic systems requiring additional moisture resistance (IP68-rated cable glands).

Industry Insight – Discrete vs. Process Manufacturing: In cables for photovoltaic power generation systems production, discrete manufacturing applies to cable assembly and termination: conductor stranding (multi-wire twisting to achieve flexibility), insulation extrusion (cross-head tooling applying uniform 0.7-1.2 mm XLPE layer), and sheath application (UV-stabilized HFFR compound). Leading manufacturers operate high-speed lines at 200-400 m/min. Process manufacturing dominates material compounding—continuous blending of XLPE resin (with dicumyl peroxide as crosslinking agent), flame retardant fillers (aluminum trihydroxide at 50-60% loading), and UV stabilizers (hindered amine light stabilizers). This bifurcation creates specialized roles: discrete-focused suppliers optimize extrusion consistency (target ±0.05 mm insulation thickness tolerance), while chemical process suppliers prioritize cure kinetics and dispersion uniformity.

3. Competitive Landscape and Technical Challenges

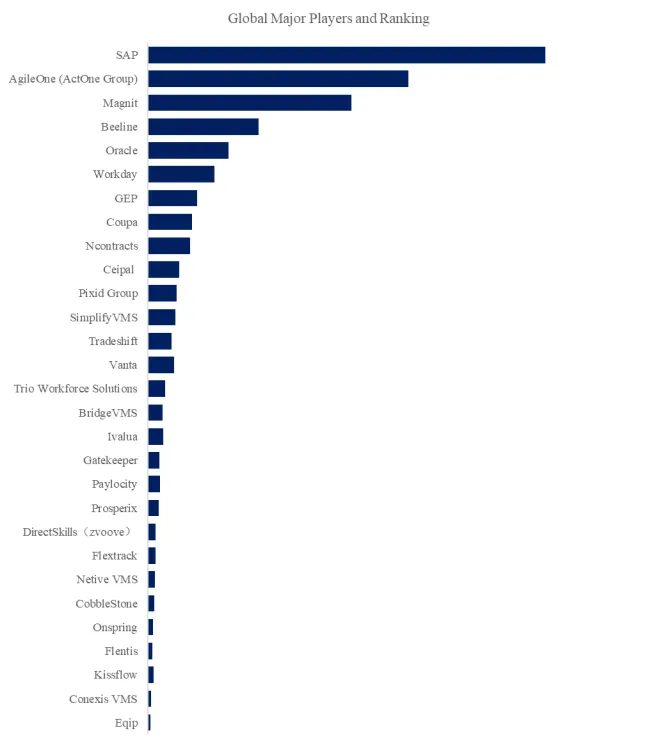

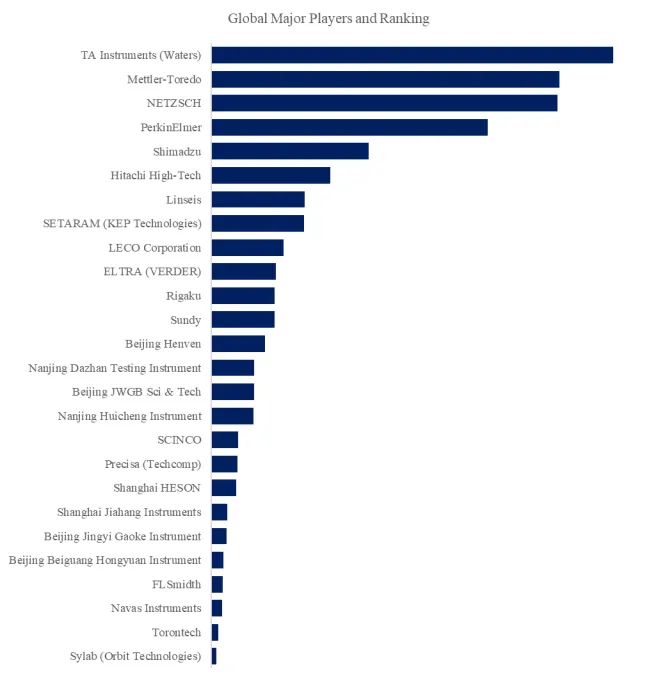

Key players include Prysmian Group (global leader, PV cable portfolio with 1,500 V certification), Nexans (European focus, low-carbon aluminium cables), Lapp Group (high-flex cables for tracker systems), Jiangsu Zhongtian Technology Co., Ltd. (largest Chinese PV cable manufacturer, 30% domestic share), Ningbo Orient Wires & Cables Co., Ltd., HENGTONG OPTIC-ELECTRIC Co., Ltd., LS Cable & System (aluminium alloy innovation), Sumitomo Electric Industries (Japanese rooftop specialist), Furukawa Electric Co., Ltd., Qingdao Hanhe Cable Co., Ltd., Guda Wire and Cable (Group) Co., Ltd., Guangdong Xinyaguang Cable Co., Ltd., Zhejiang CHINT Electric Cable Co., Ltd., Southwire (U.S. market leader), General Cable, HUBER+SUHNER (high-frequency PV cables), and Alpha Wire.

Technical Challenge – Aluminum Conductor Oxidation and Creep: Aluminium DC cables (35-50% cost savings vs. copper) face two failure modes: surface oxidation increasing contact resistance by up to 300% after 5 years, and creep relaxation causing terminal loosening. An April 2025 breakthrough from Nexans introduced a tin-nickel bilayer coating (applied via continuous electroplating), demonstrating stable contact resistance (<50 µΩ after 2,000 thermal cycles from -40°C to +85°C) and zero terminal loosening in accelerated vibration testing (10 million cycles at 50 Hz). Adoption rates for coated aluminium PV cables rose from 12% in 2024 to 28% in Q2 2025.

4. Regional Market Outlook and Exclusive Observations

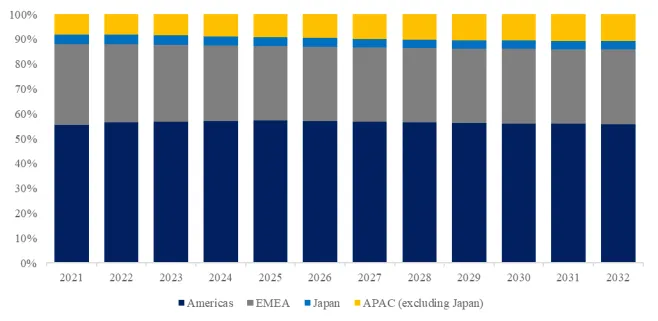

Asia-Pacific dominates with 58% global market share (US3.77billionin2025),drivenbyChina′s2025NationalEnergyAdministrationmandate(requiring1,500VDCsystemsforall>6MWprojects)andIndia′sALMM(ApprovedListofModelsandManufacturers)includingPVcablesfromApril2025.Europeholds243.77billionin2025),drivenbyChina′s2025NationalEnergyAdministrationmandate(requiring1,500VDCsystemsforall>6MWprojects)andIndia′sALMM(ApprovedListofModelsandManufacturers)includingPVcablesfromApril2025.Europeholds24 1.56 billion), supported by EU’s Eco-Design for Cables Regulation (2024) banning PVC insulation in outdoor PV applications—accelerating XLPO and TPE adoption. North America represents 14% (US$ 910 million), with the Inflation Reduction Act’s domestic content bonus (10% adder for U.S.-made cables) driving Southwire and Prysmian’s U.S. plant expansions (completed Q1 2025).

Exclusive Observation – Connector-Cable Integration Failure Mode: Industry field data (analysis of 15,000 failure reports from 2024-2025, collected by QYResearch) reveals that 62% of PV cable failures occur at the connector interface rather than along the cable length—caused by improper crimping (35%), seal degradation (28%), and dissimilar metal corrosion (39%). In response, leading OEMs like HUBER+SUHNER launched pre-terminated “plug-and-play” DC cable assemblies in February 2025, reducing on-site labor by 75% and eliminating field termination errors. Early adopters report warranty claims reduced from 1.2% to 0.15% of installed connectors. This trend toward assembly-line terminations (discrete manufacturing applied to cable subassemblies) is projected to capture 35% of the residential PV cable market by 2028.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp