Introduction (Covering Core User Needs & Pain Points):

Semiconductor packaging engineers, wafer fabrication specialists, and advanced substrate manufacturers face a critical metallization challenge: depositing uniform, high-quality metal layers (nickel (Ni), palladium (Pd), gold (Au), copper (Cu), silver (Ag), or alloys) on device surfaces without using external electric current. Traditional electroplating requires complex fixturing (electrical contacts to each substrate or wafer), cannot plate non-conductive surfaces (polymer dielectrics, passivation layers), and results in non-uniform thickness distribution (edge vs. center) on high-aspect-ratio or recessed structures. The Semiconductor Electroless Plating Solution – a chemical bath containing metal ions (e.g., NiSO₄, Na₂PdCl₄, KAu(CN)₂), reducing agents (sodium hypophosphite (NaH₂PO₂), dimethylamine borane (DMAB), formaldehyde (HCHO)), complexing agents, stabilizers, and pH buffers – enables autocatalytic (self-catalyzing) metal deposition on catalytic surfaces (typically activated by a palladium seed layer) without external current, producing uniform thickness (even on recessed features, edges, and non-planar surfaces), excellent solderability, bondability, corrosion resistance, and wire bonding compatibility (Au, Al). However, process engineers face complex decisions: plating type (ENIG (electroless nickel immersion gold), ENEPIG (electroless nickel electroless palladium immersion gold), ENIPIG (electroless nickel immersion palladium immersion gold), direct electroless copper or silver), bath chemistry (nickel-phosphorus (Ni-P) with high/low phosphorus content, nickel-boron (Ni-B), palladium-phosphorus (Pd-P)), deposit thickness (Ni 3-8μm, Pd 0.05-0.5μm, Au 0.05-0.5μm), bath stability (bath lifetime, replenishment), and compatibility with downstream processes (wire bonding (Au, Cu, Al), soldering (lead-free SnAgCu), sintering (Ag), and die attach). This industry research report by QYResearch provides a data-driven roadmap for IC substrate manufacturers (AT&S, Ibiden, Shinko, Unimicron, Samsung Electro-Mechanics), OSATs (ASE, Amkor, JCET), wafer-level packaging (WLP) foundries, and power device fabs (infineon, STMicroelectronics, onsemi). Global Leading Market Research Publisher QYResearch announces the release of its latest report “Semiconductor Electroless Plating Solutions – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032″. Based on current situation and impact historical analysis (2021-2025) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Semiconductor Electroless Plating Solutions market, including market size, share, demand, industry development status, and forecasts for the next few years.

Market Size & Product Definition:

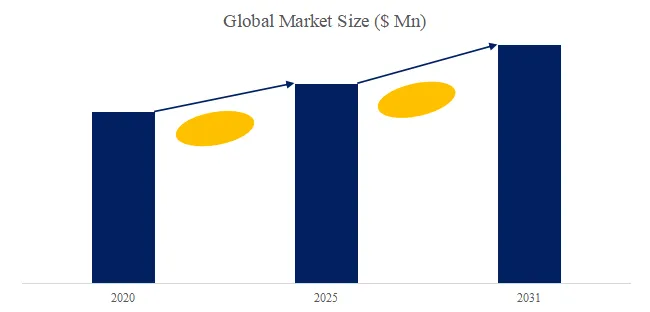

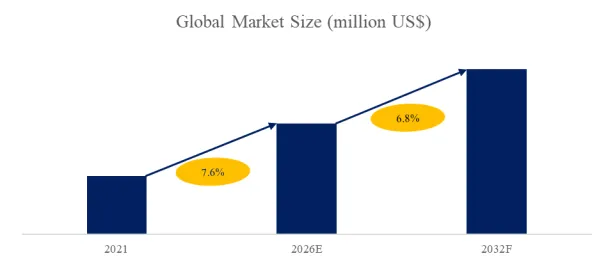

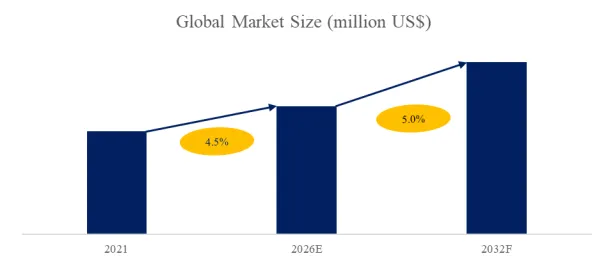

The global market for Semiconductor Electroless Plating Solutions was estimated to be worth US244millionin2025andisprojectedtoreachUS244millionin2025andisprojectedtoreachUS 402 million by 2032, growing at a CAGR of 7.5% from 2026 to 2032.

Semiconductor electroless plating solutions are specialized chemical formulations used in the semiconductor manufacturing and packaging process to deposit metallic layers (typically nickel (Ni), palladium (Pd), gold (Au), copper (Cu), silver (Ag)) on surfaces (IC package substrates, wafers (TSV (through-silicon via), RDL (redistribution layer), UBM (under bump metallurgy)), and power devices) via autocatalytic (electroless) deposition. Unlike electroplating (requires electrical contacts and external current), electroless plating works by chemical reduction: the substrate surface is first activated (by a palladium (Pd) seed layer – using a PdCl₂ solution) to create catalytic sites, then immersed in the electroless bath, where the reducing agent (e.g., sodium hypophosphite for Ni-P, DMAB for Ni-B, formaldehyde for Cu) reduces metal ions onto the catalytic surface. The deposited layer itself is catalytic (for electroless nickel, the Ni-P alloy is catalytic; for gold, the process stops after a thin immersion gold layer), enabling continuous deposition until the substrate is removed from the bath. Key advantages: (1) uniform thickness – even on complex 3D surfaces, high-aspect-ratio features, edges (no “dog-bone” effect of electroplating), (2) selective deposition – only on catalytic surfaces (palladium-activated), (3) no electric contacts – no fixturing cost, no electrical connection issues, (4) multiple substrates – batch processing possible (wafer carriers, leadframes, substrates), (5) encapsulated features – can plate into cavities and recesses where electroplating current cannot reach.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/5514301/semiconductor-electroless-plating-solutions

Section 1: Technology Segmentation – ENEPIG Dominates

The Semiconductor Electroless Plating Solutions market is segmented below by plating type and application, with updated 2025 estimates:

By Plating Type (2025 Market Share – QYResearch data):

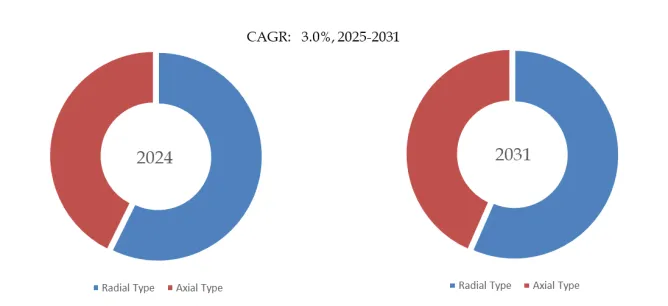

- ENEPIG (Electroless Nickel – Electroless Palladium – Immersion Gold): 60% share (largest segment; multi-layer stack: Ni-P (3-8μm, diffusion barrier/under bump metallurgy), Pd-P (0.05-0.5μm, protects Ni from oxidation and provides bondable surface), immersion Au (0.05-0.5μm, protects Pd from oxidation, provides wire bonding surface, and solderability). ENEPIG is the preferred surface finish for advanced IC substrates (flip-chip BGA, wafer-level CSP (chip-scale package), SiP (system-in-package)) due to: (1) excellent wire bondability (Au and Cu wire), (2) good solderability (lead-free SnAgCu), (3) corrosion resistance (Pd + Au layers protect Ni from oxidation), (4) flat surface (no intermetallic compounds (IMC) spikes).)

- ENIG (Electroless Nickel – Immersion Gold): 25% share (second-largest; Ni-P (3-8μm) + immersion Au (0.05-0.5μm). Simpler, lower cost than ENEPIG (no Pd layer). Disadvantages: (1) immersion Au is porous, allowing Ni oxidation over time (shelf-life issue), (2) wire bonding reliability is lower (poor adhesion to oxidized Ni), (3) black pad (corrosion) defect risk. ENIG still used in less demanding applications (older package types, consumer PCBs, power device leadframes).)

- Others (ENIPIG (Electroless Nickel – Immersion Palladium – Immersion Gold – similar to ENEPIG but Pd immersion (replaces electroless Pd) – lower cost but less uniform thickness), Direct Electroless Cu (for RDL, TSV filling), Electroless Ag (for high-frequency (RF) applications), Ni-B (for aluminum wire bonding)): 15% share (fastest-growing segments: ENIPIG for cost-sensitive substrates, direct electroless Cu for wafer-level packaging (RDL, pillar), electroless Ag for 5G RF modules)

Technical insight: ENEPIG is the dominant technology (60% share) because it addresses the limitations of ENIG (black pad, wire bonding reliability) and provides a robust, multi-functional surface finish for advanced packaging (flip-chip, wafer-level CSP, SiP, AiP (antenna-in-package)). The Pd layer in ENEPIG serves as both a diffusion barrier (prevents Ni oxidation during immersion Au plating) and a bondable surface (Pd wire bonding is also possible). The Ni-P layer is critical: (1) phosphorus content: low phosphorus (3-5% P) for solderability (less brittle intermetallic), high phosphorus (10-12% P) for corrosion resistance (amorphous Ni-P), (2) stress control: internal stress can cause warpage on thin substrates; bath additives adjust stress. A key advancement in the past six months (Q4 2025-Q1 2026) is the introduction of “low-stress ENEPIG” and “high-frequency ENEPIG” by C. Uyemura (NP-100 series) and Atotech (Auruna series). Low-stress ENEPIG (Ni-P stress <5 MPa vs. 20-30 MPa for conventional) reduces warpage on thin (0.2-0.4mm) IC substrates for mobile and HPC applications. High-frequency ENEPIG (ultra-smooth Ni-P layer with Ra <20nm, ultra-thin Pd/Au <0.1μm) minimizes insertion loss for RF/mmWave modules (5G, 6G, radar). Early adopters (AT&S, Unimicron, Samsung Electro-Mechanics) are qualifying these advanced formulations.

By Application (2025 Market Share – QYResearch data):

- IC Package Substrate (Flip-Chip BGA, CSP, SiP, AiP, FC-CSP, FC-BGA, MCM (multi-chip module), interposers (silicon, organic)): 65% share (largest segment; ENEPIG and ENIG are the standard surface finishes for bond fingers, ball pads, and under bump metallization (UBM); growth driven by AI, HPC, 5G, automotive ADAS)

- Wafer (TSV (Through-Silicon Via) filling – electroless Cu; RDL (redistribution layer) – electroless Cu or Ni-P; UBM (under bump metallurgy) – electroless Ni-P + immersion Au; wafer-level CSP (WLCSP) bumping): 25% share (fastest-growing at 10% CAGR; wafer-level packaging (WLP) eliminates substrate, reduces package height; electroless plating is batch process (multiple wafers per cassette), key for high-volume manufacturing)

- Power Device (Leadframes (copper), discrete semiconductors (diodes, MOSFETs, IGBTs), power modules (IGBT, SiC, GaN) – electroless Ni-P + immersion Ag or Au for die attach (sintering) and wire bonding (Al, Au)): 10% share (growing at 9% CAGR, driven by EV power electronics, renewable energy inverters, industrial motor drives)

Section 2: Competitive Landscape – Top Five Players Hold >76% Share (Highly Concentrated)

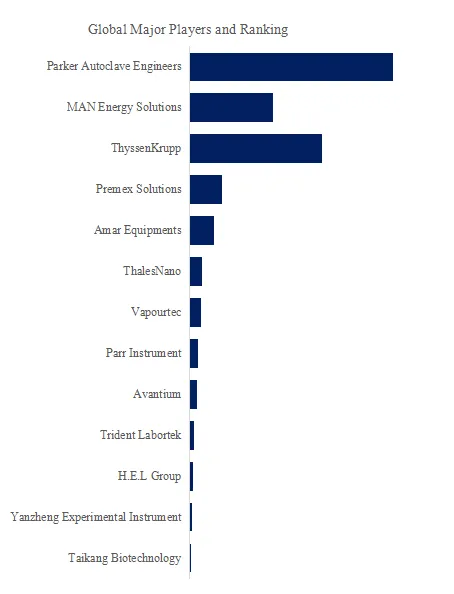

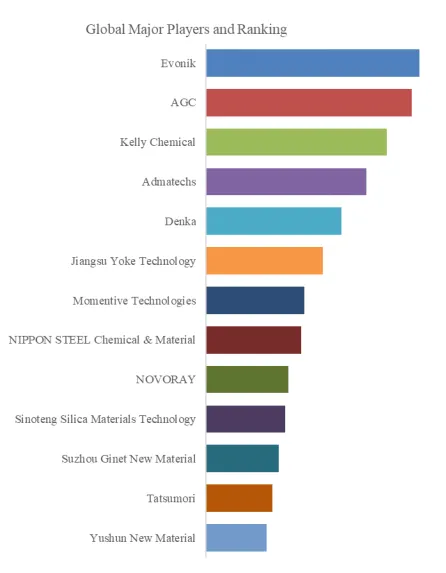

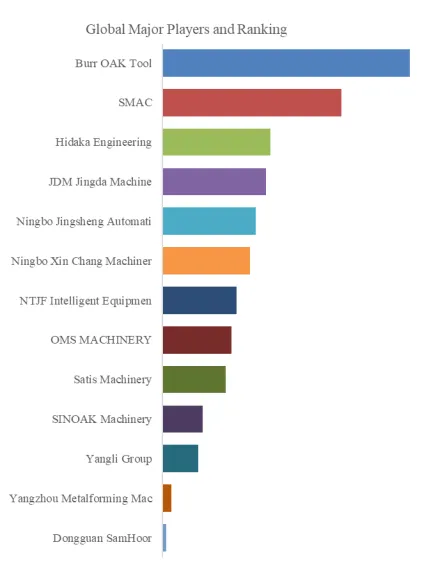

Global key players of Semiconductor Electroless Plating Solutions include C. Uyemura & Co (Japan – global leader in electroless plating for semiconductor and PCB; estimated 30-35% share; ENEPIG (NP series), ENIG, direct electroless Cu; strong in Asia-Pacific (Japan, Taiwan, Korea, China)), Atotech (MKS) (Germany/USA – subsidiary of MKS Instruments; electroless plating (Auruna series) for semiconductor, PCB, automotive; 20-25% share), DOW Electronic Materials (DuPont) (USA – electroless plating for semiconductor packaging and wafer-level processing; 10-12% share), TANAKA (Japan – precious metals; electroless Au, Pd formulations for ENEPIG/ENIPIG; 8-10% share), YMT (Japan – electroless Ni-P, Ni-B for semiconductor; 5-8% share). The top five players hold a share over 76% , indicating a highly concentrated market (oligopoly) due to: (1) proprietary chemistry (metal ion complexes, reducing agents, stabilizers, brighteners, stress relievers), (2) long qualification cycles (2-5 years for semiconductor customers; ENEPIG qualification includes 1,000+ hours reliability testing (autoclave, HAST, thermal cycling, high temperature storage), (3) technical support expertise (process troubleshooting, waste treatment (heavy metals (Ni, Pd, Au), reducing agents), analytical lab support), (4) high R&D costs (new formulations for each node (finer pitch, thinner substrates, new materials (Cu, Ag, etc.))). Other players (24% combined share): MK Chem & Tech Co., Ltd (Korea), HLHC (China), GHTECH (China), JX Metals (Japan), Shenzhen Chuangzhi Success Technology (China), Shenzhen Yicheng Electronic (China), MacDermid Enthone Industrial Solutions (USA/UK), PacTech (Germany – equipment + chemistry), KPM Tech Vina (Vietnam), OKUNO Chemical Industries (Japan), Shenzhen Hotchain (China).

Regional market share: Asia-Pacific dominates (estimated 75-80% of global consumption) due to concentration of IC substrate manufacturing (Taiwan (Unimicron, Nan Ya, Kinsus, Zhen Ding), Japan (Shinko, Ibiden, Kyocera, Toppan), Korea (Samsung Electro-Mechanics, LG Innotek, Daeduck), China (Shennan Circuits, Wus, Kinsus (China plant), AT&S (China plant)). North America (10-12% – Intel (substrate manufacturing, assembly), ASE US, Amkor US, Macom). Europe (5-8% – AT&S (Austria, China), Bosch (Germany) – power devices). Rest of World (3-5%).

Section 3: Exclusive Industry Observation – The AI/HPC Driver (Large Substrates, Thin Cores)

A 2025-2026 trend accelerating Semiconductor Electroless Plating Solutions demand (particularly ENEPIG) is the ramp-up of large, thin IC substrates for AI/HPC (artificial intelligence/high-performance computing) packages (e.g., NVIDIA B200, AMD MI300, Intel Falcon Shores). AI/HPC packages use large flip-chip BGA (FC-BGA) substrates (75×75mm up to 100×100mm) with many layers (>20) and thin cores (0.2-0.4mm). These large, thin substrates are prone to warpage (caused by CTE mismatch and plating-induced stress). ENEPIG formulations must have ultra-low stress to prevent warpage during reliability testing and device assembly.

A典型案例 (case study): A leading IC substrate manufacturer (Unimicron, Ibiden, Shinko) producing 75×75mm FC-BGA substrates for NVIDIA B200 AI accelerator (expected 2025-2026 volume ramp) experienced warpage issues (200-300μm) with conventional ENEPIG (Ni-P stress 25MPa). Warpage caused assembly issues (die attach placement accuracy, underfill flow, lid attach). Switching to low-stress ENEPIG (Ni-P stress <5MPa, C. Uyemura NP-100-LS) reduced warpage to 50-80μm, within assembly tolerance. ENEPIG consumption per large substrate: 50-100mL plating solution per substrate (multiple plating cycles). AI/HPC substrate volume is projected to reach 50-100 million units per year by 2030 (from 10-20 million in 2025), driving ENEPIG demand growth.

Section 4: Technical Challenges and Future Developments

Technical challenges for semiconductor electroless plating solutions:

- Bath stability and lifetime – Electroless baths can decompose (spontaneous plating on tank walls, heaters) or run out of metal ions or reducing agent. Bath lifetime (typically 5-10 metal turnovers (MTO) – amount of plated metal equivalent to initial bath metal content) must be managed; replenishment solutions, bath analysis, and automatic dosing systems required.

- Palladium activation process – ENEPIG requires Pd activation before electroless Ni (or before electroless Pd in ENEPIG). The Pd seed layer must be uniform, adherent, and non-porous. Pd activation step adds process complexity and cost. Newer formulations reduce Pd activation steps (direct electroless Ni on Cu, or electroless Pd on Ni without separate activation).

- Uniformity for large panels/substrates – For large IC substrates (100×100mm or panel-level packaging (PLP) 300×300mm), maintaining Ni, Pd, Au thickness uniformity across the panel is challenging (edge vs. center differences due to bath depletion, agitation, temperature gradients). Panel plating tool (vertical or horizontal) and solution flow management critical.

Recent industry developments include: (1) C. Uyemura “NPR-4 series” (2026) – next-generation ENEPIG with Pd-free activation (direct electroless Ni on Cu substrate, Ni-P layer catalytic for subsequent electroless Pd), reducing process steps and cost, (2) Atotech “Auruna 6000″ (2025) – high-speed ENEPIG for panel-level packaging (PLP), 2-3× faster deposition rate (0.5 μm/min Ni vs. 0.2 μm/min conventional), (3) DuPont “Circular Ni-Au” (2026) – electroless nickel and immersion gold with recyclable chemistry (reduced heavy metal waste, lower total cost of ownership), (4) ISO 26262 (functional safety) for power device electroless plating – new qualification requirements for EV power modules (SiC, GaN) – longer reliability testing (autoclave, H3TRB (high temperature, high humidity reverse bias), and thermal cycling).

Section 5: Market Forecast and Strategic Outlook (2026-2032)

By 2032, Asia-Pacific will remain the largest market (75-80% share), North America 10-12%, Europe 6-8%, Rest of World 4-6%. ENEPIG will maintain largest segment (58-60% share). IC Package Substrate will remain largest application (62-65% share), but Wafer (WLP) will grow to 28-30% share (from 25%) as fan-out wafer-level packaging (FOWLP) and chiplet integration increase. The market will grow at 7.5% CAGR through 2032, driven by: (1) AI/HPC large substrate demand, (2) advanced packaging (FOWLP, 3D IC, chiplets), (3) automotive power electronics (SiC, GaN), (4) 5G/6G RF modules requiring ultra-flat, low-loss ENEPIG. Key success factors: (1) low stress ENEPIG for large thin substrates, (2) high-speed deposition for panel-level packaging (PLP), (3) bath stability (longer lifetime, automatic replenishment), (4) environmental compliance (heavy metal reduction, waste treatment), (5) technical support (global coverage near customer sites).

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp