Feed Additives for Methane Mitigation Market Summary

In the battle against climate change, if carbon reduction is a marathon, then mitigating methane emissions is a decisive sprint. As a potent “heat-trapper” with over 80 times the warming power of CO2on a twenty-year scale, the natural fermentation in the gut of ruminants has become a primary target for precision intervention, and Feed Additives for Methane Mitigation are emerging as the microscopic weaponry of this green revolution. By incorporating trace amounts of bioactive substances—such as red seaweed, 3-NOP, or botanical extracts—into livestock diets, these additives directly interfere with biochemical reactions in the rumen to block the enzymatic pathways of methane production without altering feed palatability. This innovative technology, which stifles greenhouse gases at the source of every “burp,” is moving from laboratories to vast pastures, redefining the sustainable boundaries of animal husbandry while sketching a technological arc for the “Net Zero” blueprint that balances agricultural productivity with planetary cooling.

Feed additives for methane mitigation are substances added to the diets of ruminant animals—such as cows and sheep—to reduce the amount of methane they produce during digestion. These additives work by altering the fermentation process in the animals’ stomachs, inhibiting the microbes responsible for methane production without harming the animals’ health or productivity. Common types include fats, nitrates, seaweed (like Asparagopsis), and synthetic compounds such as 3-NOP (3-nitrooxypropanol). By lowering enteric methane emissions, these feed additives play a significant role in reducing the environmental impact of livestock farming and supporting climate change mitigation efforts.

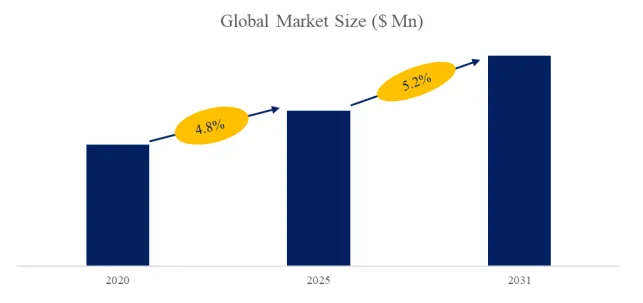

According to the new market research report “Europe Feed Additives for Methane Mitigation Market Report 2025-2031”, published by QYResearch, the Europe Feed Additives for Methane Mitigation market size is projected to reach USD 104 Million by 2031, at a CAGR of 13.2% during the forecast period.

Market Development Opportunities & Main Driving Factors

In the urgent Europe mission to address climate change, the market for methane-mitigating feed additives is in a period of dual growth fueled by policy dividends and technological breakthroughs. As the “Europe Methane Pledge” advances, governments worldwide are introducing mandatory regulations or subsidy incentives for agricultural carbon reduction, which serve as the core engine for market expansion. Iterative technological updates—particularly the accelerated commercialization of 3-NOP, seaweed extracts (such as Asparagopsis), and essential oil additives—have made it technically feasible to significantly reduce methane emissions without compromising livestock growth performance. Furthermore, the maturing carbon credit markets offer farmers additional revenue streams by converting emission reductions into tradable assets. This shift from environmental responsibility to economic benefit is attracting massive capital into biotechnology R&D, driving a leapfrog upgrade of Europe animal husbandry toward climate-smart agriculture.

Market Challenges, Risks, & Restraints

Despite its immense potential, the large-scale application of methane-mitigating feed additives faces severe challenges and multiple uncertainties. High R&D costs and production inputs directly lead to elevated terminal prices; without sustained government subsidies or premium purchasing mechanisms, farmers’ willingness to adopt remains significantly suppressed. Regulatory hurdles are equally significant, as safety assessment standards for novel feed additives vary across countries, and lengthy approval cycles increase compliance costs and market risks for enterprises. Moreover, scientific debates persist regarding whether long-term supplementation of such bioactives might disrupt rumen microecology or leave chemical residues (such as bromoform affecting meat and milk quality), posing potential crises for consumer acceptance. Finally, supply chain vulnerabilities, such as the immature large-scale cultivation technology for red seaweed, limit the stability and continuity of market supply.

Downstream Demand Trends

Downstream demand is clearly trending from “passive compliance” toward “brand premiumization.” Large food retailers and multinational dairy giants, in pursuit of their own Net Zero commitments, are leveraging their supply chain influence to mandate the adoption of mitigation technologies at the farm level, creating massive demand for customized, high-efficiency additives. Simultaneously, growing consumer preference for “climate-friendly” dairy and meat products is prompting downstream companies to develop low-carbon labeled products to capture premium margins. On the technical side, the rise of Precision Livestock Farming requires additives to better integrate with automated feeding systems for refined dosage management based on growth stages. This transformation, driven by the end of the supply chain, is forcing feed manufacturers to evolve from mere product suppliers into providers of comprehensive system solutions, including emission monitoring and reduction verification.

Figure00001. Europe Feed Additives for Methane Mitigation Market Size (US$ Million), 2020-2031

Above data is based on report from QYResearch: Europe Feed Additives for Methane Mitigation Market Report 2025-2031 (published in 2024). If you need the latest data, plaese contact QYResearch.

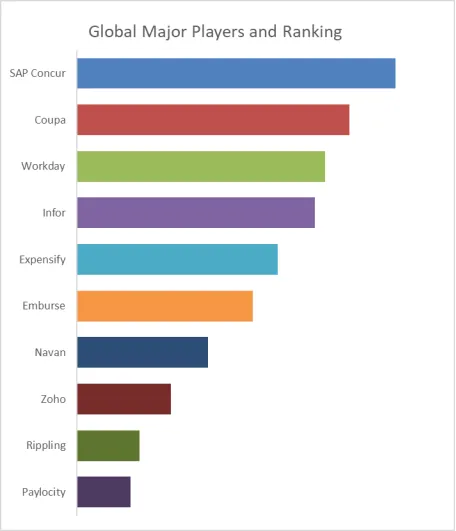

Figure00002. Europe Feed Additives for Methane Mitigation Top 8 Players Ranking and Market Share (Ranking is based on the revenue of 2024, continually updated)

Above data is based on report from QYResearch: Europe Feed Additives for Methane Mitigation Market Report 2025-2031 (published in 2024). If you need the latest data, plaese contact QYResearch.

According to QYResearch Top Players Research Center, the Europe key manufacturers of Feed Additives for Methane Mitigation include Agolin (Alltech), Cargill, etc. In 2024, the Europe top three players had a share approximately 92.0% in terms of revenue.

Figure00003. Feed Additives for Methane Mitigation, Europe Market Size, Split by Product Segment

Based on or includes research from QYResearch: Europe Feed Additives for Methane Mitigation Market Report 2025-2031.

In terms of product type, currently Asparagopsis-based is the largest segment, hold a share of 32.4%.

Figure00004. Feed Additives for Methane Mitigation, Europe Market Size, Split by Application Segment

Based on or includes research from QYResearch: Europe Feed Additives for Methane Mitigation Market Report 2025-2031.

In terms of product application, currently Dairy Cattle is the largest segment, hold a share of 81.8%.

Figure00005. Feed Additives for Methane Mitigation, Europe Market Size, Split by Region

Based on or includes research from QYResearch: Europe Feed Additives for Methane Mitigation Market Report 2025-2031

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 18 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp