OLED Front-end Materials

OLED Front-end Materials refer to the functional organic and supporting materials used during the device fabrication stage of organic light-emitting diode (OLED) panels, particularly in the thin-film deposition processes before encapsulation and module assembly. These materials include emissive layer (EML) dopants and hosts, hole transport layers (HTL), electron transport layers (ETL), hole/electron injection layers (HIL/EIL), and related high-purity evaporation materials deposited by vacuum thermal evaporation (VTE) or other coating techniques. They determine key panel performance parameters such as luminance efficiency, color purity, power consumption, lifetime, and operational stability. Because OLED devices rely on precise molecular energy level alignment and ultra-high purity, front-end materials are considered the most technically critical and value-intensive part of the OLED material supply chain.

OLED Front-end Materials Market Summary

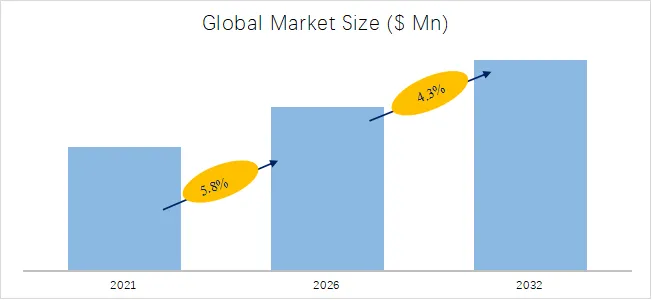

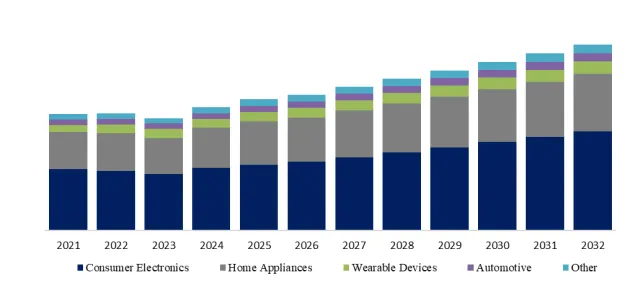

According to the new market research report “Global OLED Front-end Materials Market Report 2026-2032”, published by QYResearch, the global OLED Front-end Materials market size is projected to reach USD 4.47 billion by 2031, at a CAGR of 4.3% during the forecast period.

Global OLED Front-end Materials Market Size (US$ Million), 2021-2032

Above data is based on report from QYResearch: Global OLED Front-end Materials Market Report 2026-2032 (published in 2025). If you need the latest data, plaese contact QYResearch.

Global OLED Front-end Materials Market

Market Drivers:

The growth of the global OLED front-end materials market is primarily driven by the rapid penetration of OLED displays in smartphones, premium televisions, tablets, and emerging IT devices such as laptops and automotive displays. OLED technology offers high contrast ratio, flexibility, ultra-thin form factors, and lower power consumption compared with LCDs, encouraging panel makers to expand production capacity. In addition, the commercialization of foldable and rollable displays and the increasing adoption of LTPO backplanes in high-end devices significantly increase material consumption per panel. Continuous investment by panel manufacturers in new fabrication lines, especially in Asia, further stimulates demand for organic emissive materials, transport layers, and host materials.

Restraint:

Market expansion is constrained by the high cost and technical complexity of OLED material systems. OLED front-end materials require extremely high purity and strict synthesis control, resulting in expensive manufacturing processes and limited qualified suppliers. Panel yield sensitivity also increases material qualification cycles, making customers cautious when adopting new materials. Additionally, price pressure from consumer electronics manufacturers and competition from advanced LCD technologies, such as Mini-LED backlighting, limit the pricing power of material suppliers and slow adoption in mid-range devices.

Opportunity:

Significant opportunities arise from the expansion of OLED into new application areas, including automotive displays, AR/VR devices, wearable electronics, and large-area IT panels. The shift toward high-efficiency phosphorescent and next-generation hyperfluorescent blue emitters is expected to substantially increase material value per display. Moreover, the development of tandem OLED structures and higher-resolution panels requires more complex material stacks, increasing demand for advanced host, dopant, and transport materials. As panel makers diversify suppliers to secure supply chains, new entrants with innovative materials or cost-effective synthesis technologies have opportunities to gain market share.

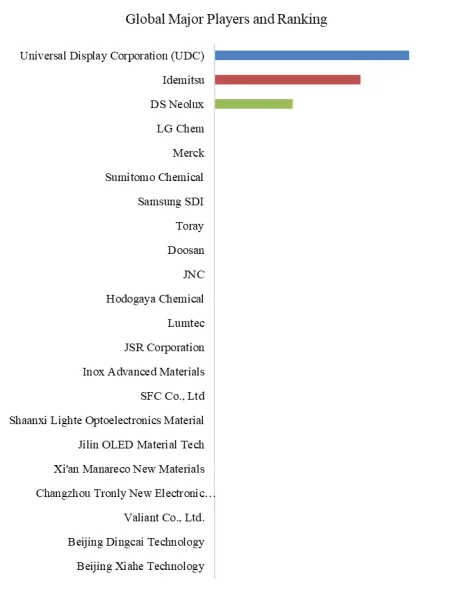

Global OLED Front-end Materials Top 22 Players Ranking and Market Share (Ranking is based on the revenue of 2025, continually updated)

Above data is based on report from QYResearch: Global OLED Front-end Materials Market Report 2026-2032 (published in 2025). If you need the latest data, plaese contact QYResearch.

This report profiles key players of OLED Front-end Materials such as Universal Display Corporation (UDC),

Idemitsu, DS Neolux.

In 2025, the global top five OLED Front-end Materials players account for 67.52% of market share in terms of revenue. Above figure shows the key players ranked by revenue in OLED Front-end Materials.

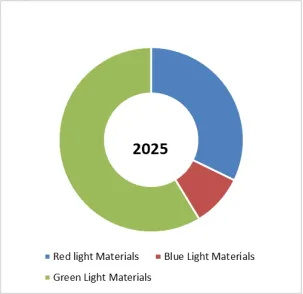

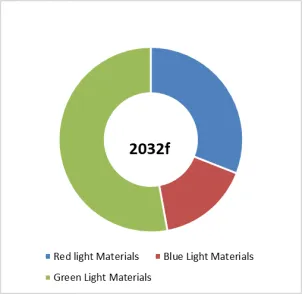

OLED Front-end Materials, Global Market Size, Split by Product Segment

Based on or includes research from QYResearch: Global OLED Front-end Materials Market Report 2026-2032.

In terms of product type, Green Light Materials is the largest segment, hold a share of 58.7%,

OLED Front-end Materials, Global Market Size, Split by Application Segment

Based on or includes research from QYResearch: Global OLED Front-end Materials Market Report 2026-2032.

In terms of product application, Consumer Electronics is the largest application, hold a share of 50.2%,

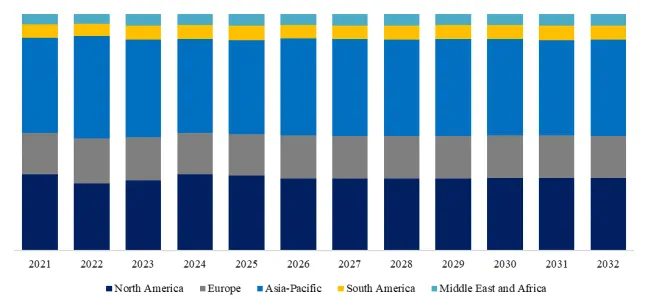

OLED Front-end Materials, Global Market Size, Split by Region

Based on or includes research from QYResearch: Global OLED Front-end Materials Market Report 2026-2032.

OLED Front-end Materials Supply Chain

The global OLED front-end materials (sublimated terminal materials) market is characterized by high technical barriers and an oligopolistic landscape, with core patents and market shares dominated by companies from the US, Japan, South Korea, and Germany (such as UDC, DuPont, Idemitsu Kosan, LG Chem, and Merck), particularly in red/green phosphorescent and high-performance blue emitters. While Chinese suppliers lead in the production of intermediates and precursors and have achieved breakthroughs in common auxiliary layers, the localization rate of critical light-emitting materials remains relatively low. With the expansion of high-generation OLED production lines in 2026, the supply chain is accelerating its transition towards high-efficiency, long-lifetime materials and localized domestic substitution.

About QYResearch

QYResearch founded in California, USA in 2007.It is a leading global market research and consulting company. With over 17 years’ experience and professional research team in various cities over the world QY Research focuses on management consulting, database and seminar services, IPO consulting, industry chain research and customized research to help our clients in providing non-linear revenue model and make them successful. We are globally recognized for our expansive portfolio of services, good corporate citizenship, and our strong commitment to sustainability. Up to now, we have cooperated with more than 60,000 clients across five continents. Let’s work closely with you and build a bold and better future.

QYResearch is a world-renowned large-scale consulting company. The industry covers various high-tech industry chain market segments, spanning the semiconductor industry chain (semiconductor equipment and parts, semiconductor materials, ICs, Foundry, packaging and testing, discrete devices, sensors, optoelectronic devices), photovoltaic industry chain (equipment, cells, modules, auxiliary material brackets, inverters, power station terminals), new energy automobile industry chain (batteries and materials, auto parts, batteries, motors, electronic control, automotive semiconductors, etc.), communication industry chain (communication system equipment, terminal equipment, electronic components, RF front-end, optical modules, 4G/5G/6G, broadband, IoT, digital economy, AI), advanced materials industry Chain (metal materials, polymer materials, ceramic materials, nano materials, etc.), machinery manufacturing industry chain (CNC machine tools, construction machinery, electrical machinery, 3C automation, industrial robots, lasers, industrial control, drones), food, beverages and pharmaceuticals, medical equipment, agriculture, etc.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp