QY Research Inc. (Global Market Report Research Publisher) announces the release of 2025 latest report “Scratch Resistant Laminating Films- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. Based on current situation and impact historical analysis (2020-2024) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Scratch Resistant Laminating Films market, including market size, share, demand, industry development status, and forecasts for the next few years.

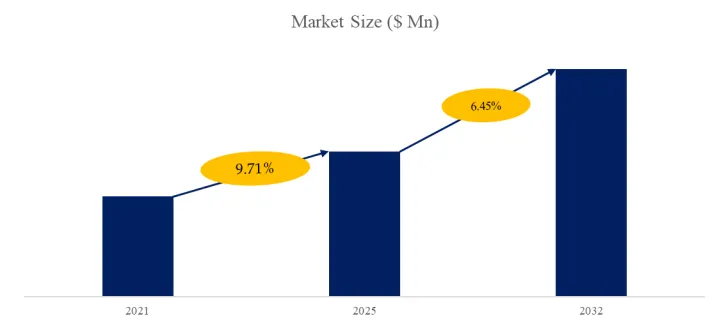

The global market for Scratch Resistant Laminating Films was estimated to be worth US$ 1999 million in 2025 and is projected to reach US$ 3133 million, growing at a CAGR of 6.5% from 2026 to 2032.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/6701061/scratch-resistant-laminating-films

Scratch Resistant Laminating Films Market Summary

Definition and Scope

Scratch resistant laminating films refer to transparent or semi-transparent film materials that attach to substrate surfaces through lamination processes and provide resistance to mechanical scratching and abrasion. The primary function of these products is to provide a durable protective layer on protected surfaces without significantly altering optical appearance, extending product service life and maintaining exterior quality. The core performance metrics of scratch resistant laminating films include surface hardness, scratch resistance, optical transmittance, haze, and interlaminar adhesion strength with the substrate.

From a material system perspective, scratch resistant laminating films are mainly classified into several types. Polyester film is one of the most widely used substrate materials for scratch resistant laminating films, offering excellent mechanical strength, dimensional stability, and chemical resistance. Polycarbonate film provides higher impact resistance and good optical transparency, suitable for applications requiring both scratch resistance and impact protection. Triacetyl cellulose film occupies an important position in display surface protection due to its excellent optical properties and low haze. Additionally, the development of ultraviolet curable hard coating technology has made it possible to achieve high hardness and high transparency scratch resistant surfaces on various film substrates.

From a product structure perspective, scratch resistant laminating films typically consist of a base film layer, a hard coating layer, and a pressure sensitive adhesive layer. The base film layer provides mechanical support and dimensional stability. The hard coating layer imparts scratch resistance through the addition of nano-inorganic particles or the use of high cross-linking density resin systems. The pressure sensitive adhesive layer enables firm adhesion between the film and the substrate. Some high-end products also incorporate additional functional layers such as anti-fingerprint coatings, anti-glare coatings, or anti-reflective coatings on the outer surface of the hard coating. Scratch resistant laminating films are applied across multiple industries including consumer electronics, automotive interiors, construction materials, optical lenses, medical devices, and packaging printing.

Figure00001. Global Scratch Resistant Laminating Films Market Size (US$ Million), 2021-2032

Above data is based on report from QYResearch: Global Scratch Resistant Laminating Films Market Report 2022-2031 (published in 2025). If you need the latest data, plaese contact QYResearch.

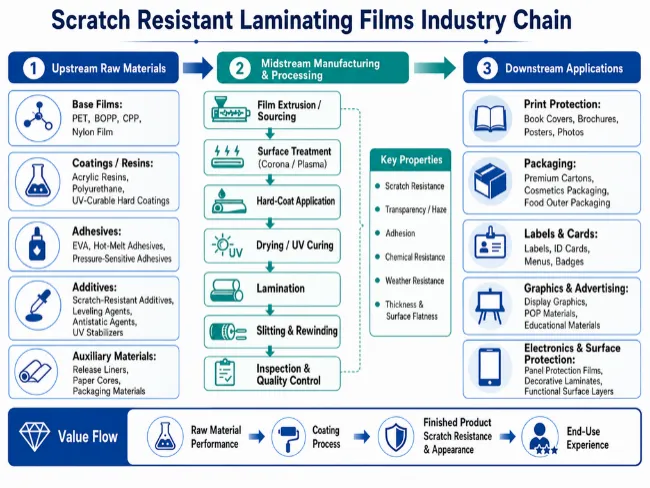

Industry Chain Analysis

Upstream segment: base film materials and functional coating raw material suppliers.

The upstream segment includes suppliers of base film materials such as polyester film, polycarbonate film, and triacetyl cellulose film, as well as suppliers of coating raw materials including UV curable resins, nano-inorganic particles, functional additives, and solvents. Base film quality directly affects film mechanical and optical properties. High-end base film supply is concentrated among a few companies with optical-grade film production capabilities. The number of suppliers capable of providing consistent quality nano-particle dispersions is limited. Upstream suppliers possess relatively strong bargaining power, and their price fluctuations and supply stability significantly impact midstream enterprises.

Midstream segment: coating processing and die-cutting manufacturers.

The midstream segment encompasses coating processing and die-cutting, representing the core value link of the industry chain. Coating processors transform base films and coating raw materials into functional film rolls through precision coating processes. Core competencies include coating precision, formulation development capability, cleanliness control, and cost management. Die-cutting manufacturers convert film rolls into finished products of specific shapes and sizes according to customer drawings, providing application accessories and services. Some large enterprises possess both coating and die-cutting capabilities, achieving vertical integration from raw materials to finished products. Die-cutting factories of various sizes are distributed across consumer electronics manufacturing clusters, forming closely integrated industry ecosystems.

Downstream segment: end-application brand owners and assembly manufacturers.

The downstream segment includes consumer electronics brand owners and their assembly factories, automotive component suppliers, optical device manufacturers, and surface treatment providers in other industrial fields. Consumer electronics demand focuses on screen protection for phones, tablets, laptops, and wearables. Automotive demand centers on center console displays and interior panels. Optical demand focuses on lens and optical component surface protection. Downstream customers vary significantly in their performance requirements, quality standards, and procurement volumes, requiring suppliers to develop differentiated product strategies and customer service approaches for different market segments.

Value distribution and future trends.

From a value distribution perspective, companies mastering upstream core base film technology and specialty coating raw material production enjoy higher profit margins. Midstream coating processing faces intense competition with squeezed margins. Die-cutting captures relatively lower value-added but requires high customer responsiveness. Future trends include intensified vertical integration, product structure upgrading toward multi-functional composite coatings, environmental pressure driving green technology transition, and increasing adoption of customization and small-batch production models requiring flexible manufacturing and rapid response capabilities.

Figure00002. Resistant Laminating Films Industrial Chain

Above data is based on report from QYResearch: Global @@@@ Market Report 2022-2031 (published in 2025). If you need the latest data, plaese contact QYResearch.

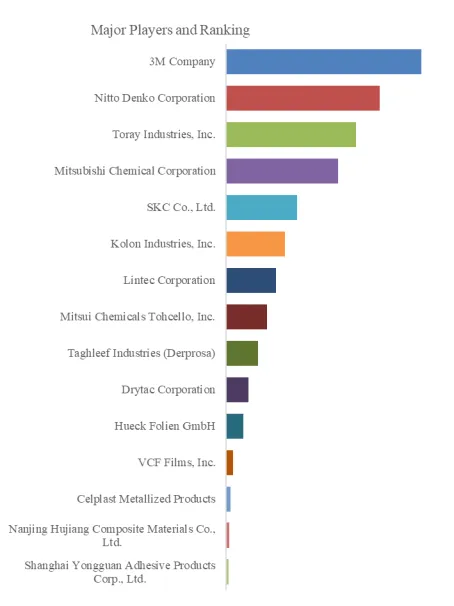

Figure00003. Global Scratch Resistant Laminating Films Top 15 Players Ranking and Market Share (Ranking is based on the revenue of 2025, continually updated)

Above data is based on report from QYResearch: Global Scratch Resistant Laminating Films Market Report 2025-2031 (published in 2025). If you need the latest data, plaese contact QYResearch.

Overall Industry Development

The global scratch resistant laminating film market is in a steady growth phase at a mature development stage. Market expansion is driven by multiple factors including consumer electronics product iteration, automotive interior quality upgrades, increasing durability requirements for construction and decoration materials, and continuous technological progress in functional films. From a market structure perspective, consumer electronics represents the largest application market for scratch resistant laminating films, with demand scale directly influenced by global shipments of smartphones, tablets, and wearable devices. The automotive sector has shown notable growth momentum in recent years, primarily due to the proliferation of large center console displays and rising consumer expectations for vehicle interior quality.

From a product evolution perspective, the scratch resistant laminating film market is undergoing a transition from single-function to multi-function integration. Early products focused only on basic requirements of surface hardness and scratch resistance. As end applications demand thinner profiles, lighter weight, and improved display quality, film products must maintain scratch resistance while further reducing thickness, increasing transmittance, decreasing haze, improving touch feel, and incorporating additional functions such as anti-fingerprint and anti-glare properties. This trend toward multi-function integration imposes higher requirements on material formulation design and precision coating processes.

From a regional distribution perspective, the Asia-Pacific region is the largest production and consumption market for scratch resistant laminating films globally. This region concentrates substantial consumer electronics manufacturing capacity and automotive component supporting industries, generating the world’s largest demand for film products. The North American and European markets focus primarily on high-end applications with more stringent requirements for optical performance, durability, and environmental compliance. In recent years, as global supply chains undergo regional restructuring, some film production capacity has been relocating to Southeast Asia and South Asia.

Key Development Characteristics

Characteristic One: Continuous Technology Evolution Toward Balancing High Hardness and High Transparency.

The core technical challenge in scratch resistant laminating films lies in balancing surface hardness and optical transparency. Improving surface hardness typically requires adding more nano-inorganic particles to the hard coating or using higher cross-linking density resin systems, but these measures often lead to increased film haze and decreased transmittance, compromising display quality. In recent years, through optimization of nano-particle size distribution, surface modification, and dispersion processes, along with development of novel organic-inorganic hybrid resin systems, film products continue to reduce haze levels while maintaining pencil hardness grades. This continuous progress enables wider adoption of scratch resistant laminating films in demanding optical applications such as high-end displays and optical lenses.

Characteristic Two: Thickness Reduction and Flexibility Becoming Important Development Directions.

As consumer electronics evolve toward thinner and foldable form factors, the thickness of scratch resistant laminating films is being compressed from traditional micron levels to much thinner dimensions. Thinner film products require the hard coating to maintain sufficient hardness and scratch resistance at extremely low coating thicknesses, posing significant challenges to coating formulation design and application precision. Furthermore, foldable screens impose entirely new requirements for film flexural endurance, demanding that films not crack or delaminate during folding while maintaining optical transparency and surface hardness after millions of folding cycles. The development of flexible scratch resistant laminating films is one of the key technical focus areas in the industry.

Characteristic Three: Environmental and Sustainability Requirements Driving Solvent-Free and Waterborne Technology Adoption.

Traditional scratch resistant laminating film production uses substantial organic solvents, releasing volatile organic compounds during coating formulation, application, and drying processes. As global environmental regulations tighten and downstream brand owners focus on supply chain sustainability, solvent-free ultraviolet curing technology and waterborne coating technology are progressively replacing conventional solvent-based processes. Ultraviolet curing technology initiates rapid coating cross-linking through UV exposure, significantly reducing organic solvent usage. Waterborne coating technology uses water as the dispersion medium, eliminating volatile organic compound emissions at the source. These environmental technologies not only reduce the environmental footprint of production but also decrease residual volatile organic compounds in finished products, contributing to improved environmental safety ratings of end products.

Characteristic Four: Multi-Functional Composite Coatings Becoming Primary Means of Product Differentiation.

As basic scratch resistance performance becomes relatively homogeneous across products, additional functions have become key to product differentiation. Anti-fingerprint coatings reduce oil and fingerprint adhesion through surface energy reduction and microstructure optimization. Anti-glare coatings reduce specular reflection of ambient light on screen surfaces through controlled surface roughness and topography, improving outdoor readability. Anti-reflective coatings reduce surface reflectance through optical interference principles, improving display contrast. Antimicrobial coatings incorporate silver ions or other antimicrobial agents to inhibit bacterial growth on film surfaces.

Favorable Factors for Development

First, consumer electronics market stock replacement and technological innovation drive demand growth.

Although the global consumer electronics market has entered a stock competition phase, technological innovation continues to generate demand for high-performance films. Smartphone bezel-less, foldable, and curved screen designs impose higher requirements on scratch resistance and adhesion precision of screen protection materials. Increasing penetration of tablets and two-in-one devices in education, office, and entertainment applications drives accessory consumption demand. The proliferation of wearable devices such as smart watches and virtual reality headsets opens new application spaces for scratch resistant laminating films. Furthermore, growing consumer awareness of device appearance protection and the widespread global practice of applying screen protectors after purchase form a continuous and stable consumables market.

Second, automotive intelligence and interior quality upgrades drive in-vehicle display film demand.

The automotive industry is transitioning from traditional mechanical instrument clusters to large digital cockpits. The size and number of center console displays, instrument cluster displays, and passenger entertainment screens continue to increase. The surface protection requirements of these displays generate substantial incremental demand for scratch resistant laminating films. Simultaneously, consumer expectations for vehicle interior quality continue rising, with scratch resistance of center console panels, decorative trim, and touch panels having become important indicators of vehicle interior quality.

Third, increasing optical performance requirements drive high-end film product penetration.

As display technology advances toward higher resolution, higher brightness, and wider color gamut, the impact of cover material optical performance on user experience becomes increasingly significant. Poor quality surface protection materials can cause display blur, color distortion, and severe ambient light reflection. Advances in scratch resistant laminating film technology have enabled continuous optimization of film transmittance and haze levels, with high-end film products achieving optical performance approaching or even reaching that of glass covers. This has upgraded films from accessories to standard features in high-end display devices, with product value and market penetration increasing in tandem.

Fourth, advancements in coating and formulation technologies lower production barriers for high-performance films.

Maturation of precision coating technologies has enabled uniform coating at micron-level thickness on wide-width, high-speed production lines. The precision of slot-die coating, micro-gravure coating, and extrusion coating processes continues to improve, with coating defect rates consistently decreasing. Meanwhile, widespread adoption of UV curing technology has significantly reduced coating curing time, improving production efficiency and energy utilization. These process advancements make large-scale, low-cost manufacturing of high-performance scratch resistant laminating films possible, establishing the industrial foundation for market penetration.

Unfavorable Factors for Development

First, upstream raw material price fluctuations affect cost stability.

The prices of core raw materials are influenced by multiple factors including crude oil prices, supply-demand relationships, and international trade policies. Raw material price volatility creates pressure on film manufacturers’ cost control and pricing strategies. In competitive market environments with strong buyer bargaining power, companies struggle to fully pass raw material cost increases to end customers, squeezing profit margins.

Second, intense industry competition leads to product homogeneity and price pressure.

As entry barriers have lowered, the number of participants in the scratch resistant laminating film industry has continued increasing, with mid-to-low end product markets experiencing significant commoditization and homogeneous competition. Many small and medium enterprises offer products with limited performance differentiation, making price the primary competitive tool and pressuring industry profit margins. In some application segments, scratch resistant laminating films have become commodities rather than differentiated products, with limited brand premium capabilities.

Third, end application requirements for thinner, more flexible, and harder products continuously challenge technology limits.

Consumer and automotive electronics requirements are approaching the technical limits of existing material systems. Foldable devices demand simultaneous achievement of high hardness, high flexibility, and high transmittance at extremely low thickness—three objectives with inherent physical contradictions, as increased hardness and reduced thickness typically come at the expense of flexibility. High-end curved displays impose demanding requirements for film adhesion precision and edge adhesion in curved regions, challenging coating process consistency. Resolving these technical challenges requires coordinated breakthroughs in fundamental materials science and process engineering, involving long development cycles, substantial investment, and high uncertainty.

Fourth, competition from alternative protection technologies diverts some market demand.

Scratch resistant laminating films are not the only technical pathway for screen and surface protection. Chemically strengthened glass has significantly improved scratch and impact resistance through ion exchange processes, with some high-end devices adopting strengthened glass covers instead of film solutions. Additionally, alternative technologies including direct spray coating of hard coatings on glass surfaces and in-mold decoration processes for hard surfaces during plastic part injection molding compete with films in specific application segments. Advances in these alternative technologies may divert demand for film products in some market segments.

Entry Barriers

First, precision coating process and equipment technology barriers.

High-performance scratch resistant laminating film production requires high precision and consistency in coating processes. Micron-level coating thickness must be uniformly distributed across wide webs. Coating surface microstructure directly affects optical properties. Elimination of defects such as bubbles, particle contamination, and thickness variation requires extensive process optimization experience. Coating equipment—including coating heads, drying/curing systems, and winding/unwinding devices—is highly specialized and customized, requiring substantial trial-and-error investment for equipment selection and process parameter matching. New entrants lacking process experience face challenges in product quality stability and yield rate control.

Second, formulation design barriers in balancing optical and mechanical properties.

Formulation design for high-performance scratch resistant laminating films requires balancing multiple mutually constraining performance metrics. Increasing surface hardness requires higher cross-linking density or nanoparticle loading, which may lead to brittleness, reduced flexibility, and increased haze. Optimizing transmittance and reducing haze requires reducing particle loading and controlling resin purity, which may compromise scratch resistance. Additionally meeting long-term service performance requirements including weather resistance, chemical resistance, and high-temperature high-humidity reliability further increases formulation design complexity. Mastering well-established formulation systems and accumulating debugging experience requires long-term R&D investment and practical validation, constituting significant technical barriers for new entrants.

Third, downstream customer qualification and supply chain access barriers.

Major downstream customers impose stringent supplier selection processes, requiring multiple rounds of sample testing, reliability validation, and on-site audits. Consumer electronics demands high cleanliness, appearance quality, and batch consistency. The automotive industry requires stringent weather resistance, chemical resistance, and long-term reliability. Once qualified, suppliers typically establish stable relationships with high customer stickiness. New entrants must invest substantial resources in customer development, sample submission, and qualification推进, resulting in long market entry cycles.

Fourth, intellectual property protection and patent portfolio barriers.

The scratch resistant laminating film field has developed a dense patent network over years of development. Core patents cover hard coating formulations, nano-particle dispersion technologies, coating processes, and multi-functional coating composite structures. Leading companies have built relatively strong intellectual property protection systems through early core patent filings and continuous improvement patent applications. New entrants must conduct thorough patent searches and infringement risk assessments when developing new products, implementing design-around strategies or seeking patent licenses based on analysis results. This increases product development complexity and uncertainty.

The report provides a detailed analysis of the market size, growth potential, and key trends for each segment. Through detailed analysis, industry players can identify profit opportunities, develop strategies for specific customer segments, and allocate resources effectively.

The Scratch Resistant Laminating Films market is segmented as below:

By Company

3M Company

Toray Industries, Inc.

Mitsubishi Chemical Corporation

SKC Co., Ltd.

Kolon Industries, Inc.

Lintec Corporation

Nitto Denko Corporation

Mitsui Chemicals Tohcello, Inc.

Taghleef Industries (Derprosa)

Drytac Corporation

Hueck Folien GmbH

VCF Films, Inc.

Celplast Metallized Products

Nanjing Hujiang Composite Materials Co., Ltd.

Shanghai Yongguan Adhesive Products Corp., Ltd.

Segment by Type

Polyester (PET)

Polyethylene (PE)

Polypropylene (PP)

Polyvinyl Chloride (PVC)

Polyurethane (PU)

Segment by Application

Consumer Electronics

Automotive (Interior Displays, Trim)

Furniture & Decorative Surfaces

Luxury Packaging

Building & Construction (Panels, Glass)

Others

Each chapter of the report provides detailed information for readers to further understand the Scratch Resistant Laminating Films market:

Chapter 1: Introduces the report scope of the Scratch Resistant Laminating Films report, global total market size (valve, volume and price). This chapter also provides the market dynamics, latest developments of the market, the driving factors and restrictive factors of the market, the challenges and risks faced by manufacturers in the industry, and the analysis of relevant policies in the industry. (2021-2032)

Chapter 2: Detailed analysis of Scratch Resistant Laminating Films manufacturers competitive landscape, price, sales and revenue market share, latest development plan, merger, and acquisition information, etc. (2021-2026)

Chapter 3: Provides the analysis of various Scratch Resistant Laminating Films market segments by Type, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different market segments. (2021-2032)

Chapter 4: Provides the analysis of various market segments by Application, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different downstream markets.(2021-2032)

Chapter 5: Sales, revenue of Scratch Resistant Laminating Films in regional level. It provides a quantitative analysis of the market size and development potential of each region and introduces the market development, future development prospects, market space, and market size of each country in the world..(2021-2032)

Chapter 6: Sales, revenue of Scratch Resistant Laminating Films in country level. It provides sigmate data by Type, and by Application for each country/region.(2021-2032)

Chapter 7: Provides profiles of key players, introducing the basic situation of the main companies in the market in detail, including product sales, revenue, price, gross margin, product introduction, recent development, etc. (2021-2026)

Chapter 8: Analysis of industrial chain, including the upstream and downstream of the industry.

Chapter 9: Conclusion.

Benefits of purchasing QYResearch report:

Competitive Analysis: QYResearch provides in-depth Scratch Resistant Laminating Films competitive analysis, including information on key company profiles, new entrants, acquisitions, mergers, large market shear, opportunities, and challenges. These analyses provide clients with a comprehensive understanding of market conditions and competitive dynamics, enabling them to develop effective market strategies and maintain their competitive edge.

Industry Analysis: QYResearch provides Scratch Resistant Laminating Films comprehensive industry data and trend analysis, including raw material analysis, market application analysis, product type analysis, market demand analysis, market supply analysis, downstream market analysis, and supply chain analysis.

and trend analysis. These analyses help clients understand the direction of industry development and make informed business decisions.

Market Size: QYResearch provides Scratch Resistant Laminating Films market size analysis, including capacity, production, sales, production value, price, cost, and profit analysis. This data helps clients understand market size and development potential, and is an important reference for business development.

Other relevant reports of QYResearch:

Global Scratch Resistant Laminating Films Market Outlook, In‑Depth Analysis & Forecast to 2032

Global Scratch Resistant Laminating Films Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

Global Scratch Resistant Laminating Films Market Research Report 2026

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 19 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp