QY Research Inc. (Global Market Report Research Publisher) announces the release of 2025 latest report “Inverter Floor-Standing Air Conditioner- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. Based on current situation and impact historical analysis (2020-2024) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Inverter Floor-Standing Air Conditioner market, including market size, share, demand, industry development status, and forecasts for the next few years.

The global market for Inverter Floor-Standing Air Conditioner was estimated to be worth US$ 2279 million in 2025 and is projected to reach US$ 3543 million, growing at a CAGR of 6.6% from 2026 to 2032.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/6102435/inverter-floor-standing-air-conditioner

An Inverter Floor-Standing Air Conditioner refers to a floor-standing cabinet-type air-conditioning unit equipped with inverter compressor control, variable-speed fan operation, electronic control modules, sensors, and system-level control algorithms to provide cooling and/or heating output based on real-time indoor load. Compared with wall-mounted room air conditioners, floor-standing units typically deliver stronger airflow, wider space coverage, and a more visible interior design function; compared with central air-conditioning systems or large commercial HVAC units, they offer lower installation complexity and greater flexibility for residential and light commercial use. In practical market terms, this product category is not defined solely by its cabinet-style appearance, but by the combination of floor-standing indoor unit structure, inverter-based load adjustment, medium-to-large space coverage, installation service, and after-sales support. Its value proposition is increasingly centered on energy efficiency, low noise, stable temperature control, comfortable airflow, low-temperature heating capability, smart connectivity, exterior design, and brand service capability. The simplified QYResearch material also frames the market through five dimensions: product capacity, application scenario, sales channel, regional market, and competitive structure.

The global inverter floor-standing air conditioner market is a mid-to-high-value segment within the broader room air-conditioning industry. In value terms, the market is already in the multi-billion-dollar range in 2025 and is expected to expand further by 2032, with growth generally supported by a mid-single-digit to relatively high-single-digit CAGR over the forecast period. The central investment logic is not merely higher unit shipments, but a structural shift from low-efficiency, basic cooling/heating products toward higher-efficiency, more comfortable, and more intelligent units. Global cooling demand provides the long-term demand base: the International Energy Agency notes that space cooling is the fastest-growing source of energy demand in buildings and is expected to rise by almost 4% annually to 2035 under today’s policy settings, with most growth coming from emerging and developing economies. At the same time, stricter energy-efficiency requirements, consumer preference for low-noise and stable indoor comfort, and the expansion of smart home ecosystems are pushing the category toward premiumization. In China and other Asia-Pacific markets, demand is supported by household upgrading, high-temperature climate conditions, and small commercial space expansion; in mature markets, replacement demand, energy-efficiency upgrading, and smart-control functions are more important growth levers.

The product structure of inverter floor-standing air conditioners can be segmented by capacity, technical route, energy-efficiency level, heating/cooling function, and smart-control capability. By capacity, small-capacity models around 2P–3P mainly serve residential living rooms and compact spaces, while medium-capacity models around 4P–5P are widely used in larger living rooms, offices, meeting rooms, shops, and light commercial venues. Large-capacity models above 6P are more aligned with open commercial areas, project procurement, and larger indoor spaces. From a technology perspective, full DC inverter products remain the mainstream upgrade route, while enhanced heating/EVI models are more attractive in colder regions where low-temperature heating performance matters. Comfort-airflow products emphasize wide-angle airflow, layered airflow, anti-direct-blow design, and low-noise operation, while smart energy-saving models integrate sensors, connected data, app control, and algorithm-based operating modes. Going forward, the fastest structural growth is expected in high-efficiency inverter models, full DC inverter units, low-noise comfort-airflow products, strong-heating models, and smart connected units, while low-efficiency and basic-function products will gradually lose share as regulatory and consumer requirements rise. The QYResearch material also highlights full DC inverter, enhanced heating/EVI, comfort airflow, and smart energy-saving control as the key technical routes.

By application, inverter floor-standing air conditioners are mainly driven by two demand engines: residential upgrading and light commercial operation. Residential demand is concentrated in large living rooms, open-plan living and dining spaces, duplex apartments, and quality-upgrade housing scenarios. These users tend to prioritize comfort, quiet operation, stable temperature control, appearance, and smart operation. Light commercial demand covers offices, meeting rooms, retail stores, restaurants, service venues, and other small-to-medium commercial spaces. These customers are more sensitive to airflow coverage, operating stability, energy cost, installation convenience, and after-sales response. In the coming years, residential growth will mainly come from replacement demand, housing improvement, and premium consumption, while light commercial growth will be supported by energy-saving renovation, store image upgrading, and regional service-network development. Residential living rooms will remain the core application base, but offices, retail stores, restaurants, and service venues are expected to show stronger incremental elasticity, especially in Asia-Pacific, the Middle East, and other regions with hot climates and active small commercial sectors.

The global inverter floor-standing air conditioner market shows a competitive structure characterized by leading brand concentration in the mid-to-high-end segment, regional-brand participation in the low-to-mid-end segment, and increasing importance of service fulfillment. Leading players generally hold advantages in compressors, inverter control, heat exchangers, airflow design, unit-level control algorithms, manufacturing consistency, energy-efficiency certification, brand recognition, and after-sales networks. Their competitive edge is no longer limited to cooling capacity or price; it is based on the integrated capability of core component coordination, energy-efficiency optimization, low-noise design, smart control, channel access, installation delivery, and service response. Regional manufacturers and channel-oriented brands can still compete through price, local distribution, and fast installation response, but they face pressure as consumers and regulations move toward higher efficiency and better comfort. In general, the premium market is relatively concentrated, while the mid-to-low-end market remains more fragmented. Over time, low-efficiency and weak-service products will face a narrower competitive space, while brands with stronger R&D, quality consistency, channel integration, and service execution will be better positioned to gain share.

From a regional perspective, China is one of the most important production bases and consumer markets for inverter floor-standing air conditioners, supported by a complete supply chain covering compressors, heat exchangers, motors, electronic control modules, plastic parts, metal structures, final assembly, online/offline retail channels, and after-sales service networks. Japan and South Korea are mature markets where users place relatively high emphasis on energy efficiency, quiet operation, comfort airflow, and smart functions. Southeast Asia, the Middle East, and parts of Latin America have stronger growth potential due to hot climates, urbanization, rising household income, and expanding small commercial spaces. Europe and North America are more regulation-driven, with higher requirements for energy efficiency, refrigerants, safety certification, and brand service capability; floor-standing units in these markets are more commonly positioned for specific residential, commercial, or supplementary cooling scenarios. Over the forecast period, incremental sales growth is expected to be stronger in Asia-Pacific, the Middle East, and selected emerging markets, while mature markets will be driven more by replacement, energy-efficiency upgrading, and premium smart products. The IEA’s analysis that cooling demand growth is concentrated in emerging and developing economies supports this regional growth logic.

Inverter Floor-Standing Air Conditioner Market Structure

Figure from QYResearch: Global Inverter Floor-Standing Air Conditioner Market Report 2026-2032.

From the perspective of market structure, inverter-based floor-standing air conditioners should not be viewed merely as a generic category of “floor-standing AC products”; rather, they constitute a comprehensive sub-segment of the home appliance market, shaped collectively by product capacity, application scenarios, sales channels, regional demand, and brand competition. In terms of capacity, lower-horsepower models primarily target residential living rooms and small-to-medium-sized spaces, while medium-to-high-horsepower models predominantly serve light commercial settings—such as offices, conference rooms, retail shops, dining establishments, and service venues. Regarding sales channels, a diverse ecosystem comprising brand-owned outlets, appliance retail chains, e-commerce platforms, bulk procurement for engineering projects, and regional distributors collectively handles customer acquisition, delivery, and after-sales service functions. Within this ecosystem, online channels have enhanced price transparency and outreach efficiency, while offline networks remain indispensable for installation, commissioning, and after-sales support responsiveness. Regionally, demand structures vary across markets such as China, Japan and South Korea, Southeast Asia, Europe, North America, and the Middle East: mature markets prioritize energy efficiency, comfort, and brand-specific services, whereas emerging markets and regions with high temperatures are driven primarily by rising cooling demand, urbanization, and the expansion of small-to-medium-sized commercial spaces. The International Energy Agency (IEA) notes that the growth rate of energy demand for cooling in buildings over the past decade has exceeded double the growth rate of overall building energy demand, indicating that air conditioning products continue to possess a solid foundation for long-term demand. Furthermore, China’s ongoing promotion of “trade-in” policies for home appliances—which now extend subsidies to a broader range of product categories—is also conducive to the replacement and upgrading of existing units with high-efficiency inverter-based floor-standing air conditioners. Consequently, the core of market competition for inverter-based floor-standing air conditioners is shifting away from a singular focus on price and cooling capacity toward a comprehensive competitive landscape encompassing “energy efficiency performance, user comfort experience, installation and after-sales support, channel synergy, and brand credibility.”

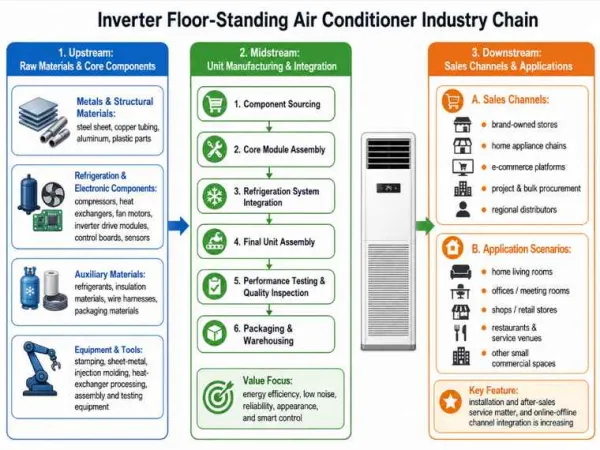

Inverter Floor-Standing Air Conditioner Industry Chain

Figure from QYResearch: Global Inverter Floor-Standing Air Conditioner Market Report 2026-2032.

From the perspective of the industrial chain, inverter-type floor-standing air conditioners represent a quintessential appliance category characterized by the synergy of “core components + complete unit integration + channel services.” The upstream segment primarily comprises metals and structural materials, refrigeration and electronic control components, auxiliary materials, and production equipment. Among these, compressors, heat exchangers, fan motors, inverter drive modules, control boards, and sensors collectively determine the unit’s energy efficiency, temperature control stability, noise levels, and overall reliability. According to disclosures from leading appliance manufacturers—such as Midea—core components including compressors, motors, chips, valves, and inverter drives have become integral elements of the industrial chain strategies adopted by major appliance conglomerates. The core of the midstream segment extends beyond mere assembly; it involves cultivating system integration capabilities centered on component procurement, core component assembly, refrigeration system integration, complete unit assembly, performance testing, and quality inspection. Ultimately, these capabilities manifest as key product competitive advantages in areas such as energy efficiency, quiet operation, reliability, aesthetic design, and intelligent control. The downstream segment reaches end-use environments—including home living rooms, offices, conference rooms, retail shops, dining establishments, and service venues—through a collective network comprising brand-owned direct outlets, appliance retail chains, e-commerce platforms, large-scale project procurement channels, and regional distributors. Given that the IEA has noted a continued rise in global energy demand for space cooling, high-efficiency refrigeration equipment plays a critical role in alleviating pressure on electricity grids. Consequently, the future value growth within the inverter-type floor-standing air conditioner industrial chain will increasingly focus on high-efficiency inverter control, low-noise airflow systems, intelligent temperature regulation, installation and delivery services, and after-sales support capabilities—shifting away from a sole reliance on manufacturing cost or price competition.

Working Principles of Inverter Floor-Standing Air Conditioners Based on Different Technical Approaches

Figure from QYResearch: Global Inverter Floor-Standing Air Conditioner Market Report 2026-2032.

From a technical perspective, the value chain for inverter-type cabinet air conditioners is not concentrated solely in the final assembly stage; rather, it forms a comprehensive technical chain extending from upstream core components to midstream system integration, and finally to the delivery of a superior downstream user experience—all centered around “inverter compressor control, heat exchange system enhancement, airflow distribution optimization, and intelligent energy-saving algorithms.” The critical aspect of the upstream segment lies in the performance matching of key components—including compressors, fan motors, inverter drive modules, control boards, sensors, heat exchangers, expansion valves, and refrigerant circuits. Among these, the speed modulation capabilities of the compressor and motor directly determine the unit’s overall energy efficiency and load response performance. Midstream manufacturers must integrate technical approaches—such as full-DC inverter technology, low-temperature high-output heating (including EVI enthalpy injection), comfort-optimized airflow, and intelligent energy-saving controls—into their product platforms. By leveraging control algorithms, air duct design, heat exchange efficiency, noise suppression, and reliability testing, they establish a differentiated product competitive edge. Industry insights regarding inverter technology indicate that these systems automatically adjust compressor speed to precisely match cooling or heating demands, thereby achieving more stable temperature control, reduced noise levels, and higher energy efficiency. This signifies that the core competitive battleground for inverter-type cabinet air conditioners is shifting away from a singular focus on cooling capacity toward a comprehensive capability encompassing “core component synergy + system control + user comfort experience.” Furthermore, the International Energy Agency (IEA) notes that space cooling represents one of the fastest-growing areas of end-use energy demand within the building sector. Consequently, high-efficiency cooling equipment will play a pivotal role in alleviating pressure on power grids in the future. As such, future growth within the inverter-type cabinet air conditioner value chain will be driven primarily by advancements in high-efficiency inverter control, low-temperature heating performance, intelligent energy conservation, comfort-optimized airflow, and installation/after-sales service capabilities—rather than relying solely on price-based competition.

China’s policy environment is broadly supportive of high-efficiency, intelligent, and green household appliances, including inverter air conditioners. Over the past five years, policies related to green consumption, consumer-goods trade-in, equipment renewal, energy efficiency, green cooling, recycling of used appliances, and low-carbon development have strengthened the replacement logic for high-efficiency products. The State Council launched the large-scale equipment renewal and consumer goods trade-in action plan in 2024, and official releases have emphasized the role of home-appliance trade-ins in supporting domestic demand and upgrading consumption. China’s Green and High-Efficiency Cooling Action Plan also set long-term targets for improving the efficiency of cooling products and increasing the market share of green and efficient cooling equipment. Under the 15th Five-Year Plan period, policy direction is expected to continue emphasizing green consumption, energy conservation, carbon reduction, smart appliances, and resource recycling, which will support demand for high-efficiency inverter floor-standing AC products.

Relevant Chinese Policies

| Policy Direction | Period | Core Focus | Impact on the Inverter Floor-Standing AC Industry |

| Green and high-efficiency cooling | Recent years and continuing | Improve cooling-product efficiency and expand green cooling adoption | Supports high-efficiency inverter units, low-noise systems, and advanced control technologies |

| Large-scale equipment renewal and consumer goods trade-in | Since 2024 | Promote replacement of durable consumer goods, including home appliances | Stimulates replacement demand and accelerates upgrading toward efficient products |

| Home-appliance trade-in subsidies | 2024–2026 extension trend | Encourage consumers to replace old appliances with efficient new models | Directly benefits air conditioners with higher energy-efficiency ratings |

| Green and smart home-appliance consumption | Recent five years | Promote green, smart, and quality-oriented appliances | Expands demand for intelligent inverter floor-standing ACs |

| Energy-efficiency standard upgrading | Ongoing | Tighten efficiency requirements and phase out inefficient products | Raises product barriers and supports premiumization |

| Resource recycling and used-appliance treatment | 2024–2026 | Improve recycling, dismantling, and reuse systems for used appliances | Links old-unit replacement with new-unit demand and circular economy development |

| Green buildings and efficient equipment promotion | 15th Five-Year Plan period | Encourage efficient cooling and low-carbon building equipment | Supports light commercial and public-space demand for efficient AC units |

| Green consumption and low-carbon lifestyle | 15th Five-Year Plan period | Expand green product supply and consumer adoption | Improves consumer acceptance of high-efficiency and smart AC products |

| Digital and intelligent manufacturing | 15th Five-Year Plan period | Promote digitalization, smart manufacturing, and quality upgrading | Pushes manufacturers to improve process consistency, product reliability, and smart-control capabilities |

The industry’s growth is driven by rising cooling demand, energy-efficiency regulation, consumption upgrading, light commercial expansion, smart home penetration, and the integration of online and offline service channels. However, the market also faces challenges such as real estate-cycle fluctuation, intense price competition in lower-end segments, cost pressure from energy-efficiency upgrades, installation and after-sales complexity, raw-material volatility, and regional certification differences. In practical terms, the market is not short of demand; rather, demand is becoming more selective. Basic low-end demand is becoming more stable, while mid-to-high-end upgrading and light commercial demand show better resilience. Companies with strong product R&D, energy-efficiency technology, cost control, channel integration, and local service execution will have a stronger ability to gain share through the cycle.

Growth Drivers, Restraints/Challenges

| Type | Factor | Manifestation | Industry Impact |

| Growth Driver | Rising cooling demand and hotter climates | Higher reliance on cooling and stable indoor comfort | Expands baseline demand for medium-to-large capacity units |

| Growth Driver | Energy-efficiency regulation | Higher standards and stronger policy support for efficient appliances | Accelerates inverter replacement of low-efficiency products |

| Growth Driver | Residential upgrade demand | Large living rooms and quality housing require quiet, comfortable, and attractive AC units | Supports premium floor-standing AC sales |

| Growth Driver | Light commercial expansion | Offices, stores, restaurants, and service venues need flexible cooling and heating solutions | Supports project, distribution, and regional-service demand |

| Growth Driver | Smart control and connectivity | Sensors, app control, AI energy saving, and scenario modes become selling points | Increases product value and brand differentiation |

| Growth Driver | Online-offline channel integration | Online traffic, offline delivery, installation, and after-sales are combined | Improves customer reach and service retention |

| Barrier/Challenge | Real estate and decoration-cycle fluctuation | New housing delivery, renovation, and store openings may fluctuate | Affects the pace of new demand |

| Barrier/Challenge | Low-end price competition | Regional and channel brands compete aggressively on price | Pressures margins and weakens R&D/service investment |

| Barrier/Challenge | Cost pressure from efficiency upgrades | High-efficiency compressors, electronic controls, and heat exchangers increase cost | Tests scale, cost control, and pricing strategy |

| Barrier/Challenge | Installation and after-sales complexity | Floor-standing units require installation, commissioning, maintenance, and service response | Weak service networks may damage customer experience |

| Barrier/Challenge | Raw-material and component-cost volatility | Copper, aluminum, steel, compressors, and electronic modules fluctuate | Affects gross margin and pricing decisions |

| Barrier/Challenge | Regional standards and certification differences | Energy efficiency, refrigerant, safety, and environmental rules vary by market | Raises export compliance and product-adaptation costs |

The inverter floor-standing air conditioner industry is moving from a traditional cooling/heating equipment category toward an energy-efficient, comfortable, intelligent, and service-oriented indoor climate solution. Over the next several years, the global market is expected to maintain steady growth, supported by climate-driven cooling demand, replacement of low-efficiency products, residential upgrading, light commercial expansion, and smart-control penetration. Competition in the mid-to-high-end segment will increasingly center on full DC inverter control, enhanced heating/EVI, quiet and comfortable airflow, smart energy-saving algorithms, exterior design, quality consistency, and service networks. The premium segment is likely to become more concentrated around brands with stronger technology and service capabilities, while the low-to-mid-end market will remain more fragmented but face margin and efficiency pressure. For manufacturers, the key to future competitiveness will not be low price alone, but the integrated capability to deliver energy efficiency, comfort, intelligence, reliable installation, and after-sales service. For the broader air-conditioning market, inverter floor-standing ACs will remain a structurally attractive segment with stable scale and ongoing product-upgrade potential.

The report provides a detailed analysis of the market size, growth potential, and key trends for each segment. Through detailed analysis, industry players can identify profit opportunities, develop strategies for specific customer segments, and allocate resources effectively.

The Inverter Floor-Standing Air Conditioner market is segmented as below:

By Company

Samsung

Philips

Mitsubishi Heavy Industries

Hitachi

LG

Haier

TCL

Midea

GREE

xiaomi

Panasonic

AUX

Changhong

Sanlux

Segment by Type

1-HP

2-HP

3-HP

4-HP

5-HP

Segment by Application

Home Use

Commercial Use

Each chapter of the report provides detailed information for readers to further understand the Inverter Floor-Standing Air Conditioner market:

Chapter 1: Introduces the report scope of the Inverter Floor-Standing Air Conditioner report, global total market size (valve, volume and price). This chapter also provides the market dynamics, latest developments of the market, the driving factors and restrictive factors of the market, the challenges and risks faced by manufacturers in the industry, and the analysis of relevant policies in the industry. (2021-2032)

Chapter 2: Detailed analysis of Inverter Floor-Standing Air Conditioner manufacturers competitive landscape, price, sales and revenue market share, latest development plan, merger, and acquisition information, etc. (2021-2026)

Chapter 3: Provides the analysis of various Inverter Floor-Standing Air Conditioner market segments by Type, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different market segments. (2021-2032)

Chapter 4: Provides the analysis of various market segments by Application, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different downstream markets.(2021-2032)

Chapter 5: Sales, revenue of Inverter Floor-Standing Air Conditioner in regional level. It provides a quantitative analysis of the market size and development potential of each region and introduces the market development, future development prospects, market space, and market size of each country in the world..(2021-2032)

Chapter 6: Sales, revenue of Inverter Floor-Standing Air Conditioner in country level. It provides sigmate data by Type, and by Application for each country/region.(2021-2032)

Chapter 7: Provides profiles of key players, introducing the basic situation of the main companies in the market in detail, including product sales, revenue, price, gross margin, product introduction, recent development, etc. (2021-2026)

Chapter 8: Analysis of industrial chain, including the upstream and downstream of the industry.

Chapter 9: Conclusion.

Benefits of purchasing QYResearch report:

Competitive Analysis: QYResearch provides in-depth Inverter Floor-Standing Air Conditioner competitive analysis, including information on key company profiles, new entrants, acquisitions, mergers, large market shear, opportunities, and challenges. These analyses provide clients with a comprehensive understanding of market conditions and competitive dynamics, enabling them to develop effective market strategies and maintain their competitive edge.

Industry Analysis: QYResearch provides Inverter Floor-Standing Air Conditioner comprehensive industry data and trend analysis, including raw material analysis, market application analysis, product type analysis, market demand analysis, market supply analysis, downstream market analysis, and supply chain analysis.

and trend analysis. These analyses help clients understand the direction of industry development and make informed business decisions.

Market Size: QYResearch provides Inverter Floor-Standing Air Conditioner market size analysis, including capacity, production, sales, production value, price, cost, and profit analysis. This data helps clients understand market size and development potential, and is an important reference for business development.

Other relevant reports of QYResearch:

Global Inverter Floor-Standing Air Conditioner Market Outlook, In‑Depth Analysis & Forecast to 2032

Global Inverter Floor-Standing Air Conditioner Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

Global Inverter Floor-Standing Air Conditioner Market Research Report 2026

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 19 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp