PIN PhotoDiodes Market Summary

A PIN photodiode is a semiconductor photodetector built on a P-layer, intrinsic I-layer, and N-layer structure. It converts incoming optical signals into electrical signals with high efficiency and offers fast response speed, low junction capacitance, strong linearity, and high sensitivity. As a result, it has become one of the most important receiving-side components in modern optoelectronic systems. It is widely used in industrial inspection and analytical instruments, communications and data transmission, consumer electronics, and other high-reliability applications, serving as both a key interface in signal transmission links and a core sensing component in intelligent systems. The global market has already evolved into a product structure led by silicon PIN photodiodes, InGaAs PIN photodiodes, and other specialized products, showing that this is not simply a standardized discrete device market, but a hybrid market combining the characteristics of foundational electronic components and high-performance optoelectronic devices. With the continued upgrading of digital infrastructure, deeper industrial automation, and the steady evolution of intelligent terminals, PIN photodiodes are moving from relatively low-profile supporting components to a position that directly influences system performance, product upgrading, and industrial competitiveness.

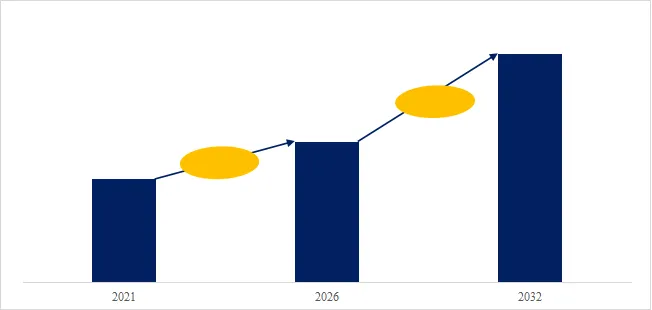

According to the new market research report “Global PIN PhotoDiodes Market Report 2025-2031″, published by QYResearch, the global PIN photodiode industry has entered a growth stage defined by stronger quality and clearer structural momentum. According to the attached data, the global market stood at approximately USD 673 million in 2021, increased to USD 810 million in 2025, and is projected to reach USD 1,493 million by 2032, representing a compound annual growth rate of about 8.41% for 2026–2032. This level of growth indicates that the market is no longer driven mainly by traditional replacement demand or inventory normalization, but is instead entering a phase of structural expansion supported by multiple high-growth applications. More importantly, this growth is not built on a single end market. It is supported simultaneously by industrial inspection, communications and data transmission, consumer electronics, and other specialized fields. Such a demand structure gives the industry both growth elasticity and operational resilience, while also suggesting that future value creation will come increasingly from product mix upgrading, deeper penetration into higher-end applications, and a rising share of premium products rather than from shipment growth alone.

Figure00001. Global PIN PhotoDiodes Market Size (US$ Million), 2021-2032

Above data is based on report from QYResearch: Global PIN PhotoDiodes Market Report 2025-2031 (published in 2025). If you need the latest data, plaese contact QYResearch.

Industrial Inspection and Analytical Instruments Remain the Largest Application Segment and Form the Foundation of the Market

From the downstream demand structure, industrial inspection and analytical instruments have become the largest application segment for global PIN photodiodes. In 2025, this segment reached USD 361 million and accounted for about 44.61% of the global market. By 2032, it is expected to rise further to USD 649 million, maintaining its position as the largest application area. Communications and data transmission represented about USD 200 million in 2025, accounting for 24.70% of the market, and is projected to grow to USD 393 million by 2032. Consumer electronics reached approximately USD 149 million in 2025, representing 18.37%, and is expected to increase to USD 267 million by 2032. Other applications accounted for around USD 100 million in 2025, or 12.32%, and are projected to approach USD 184 million by 2032. This market structure shows that PIN photodiodes are not dependent on a single high-profile application cycle, but are deeply embedded in a wide range of long-term demand scenarios including industrial measurement, equipment monitoring, optical signal reception, and intelligent terminal sensing. Industrial inspection and analytical instruments in particular, with their high market share, strong customer stickiness, and demanding technical requirements, form the most stable demand base for the industry.

Communications and Data Transmission Demand Is Accelerating and Pushing the Industry Toward Higher-Performance Competition

While industrial inspection remains the foundation of the market, communications and data transmission is becoming the most important incremental growth engine. The attached data show that this segment is expected to deliver a compound annual growth rate of about 9.18% during 2026–2032, above the global market average and higher than major application areas such as industrial inspection and analytical instruments and consumer electronics. The deeper reason behind this trend is that data centers, high-speed interconnects, cloud computing infrastructure, and next-generation communication network upgrades are all raising the performance threshold for optical receiving devices. Market competition will increasingly focus on higher speed, smaller size, lower noise, higher sensitivity, and stronger reliability. As a result, the industry is gradually moving beyond conventional discrete device competition toward a broader contest centered on transmission performance and system-level compatibility. For manufacturers, the ability to enter high-bandwidth, high-speed, and high-value communication links will play a decisive role in determining their position in the next stage of industry upgrading.

Barriers Across the Value Chain Are High, and Competitive Strength Is Shifting from Manufacturing Scale to Coordinated Capability

Although PIN photodiodes are physically small devices, the industry’s value chain is far from simple. Upstream requirements include key materials such as high-purity silicon and InGaAs, together with multiple process steps including epitaxy, growth, doping, lithography, chip fabrication, packaging, testing, and reliability control. The midstream segment requires not only stable mass production capability, but also long-term consistency, yield control, and customization capacity. Downstream demand comes from industrial equipment, communication systems, consumer devices, and specialized detection applications, with each customer group having different requirements for performance, lifetime, package type, and qualification procedures. This means competition in the industry is no longer a straightforward manufacturing contest. It has become a system-level competition based on material understanding, device design, packaging expertise, application adaptation, and customer validation. The further the market moves into higher-end applications, the more essential it becomes for suppliers to build coordinated development capability from chip to package and from product to end-use scenario. That capability is one of the industry’s most durable long-term barriers.

A Leading-Player Structure Has Already Emerged, and the Market Is Moving from Product Competition to Platform Competition

From the perspective of the competitive landscape, the global PIN photodiode market has already formed a multi-layered group of leading participants. Major companies currently active in the market include Hamamatsu Photonics, MACOM, Broadcom, Lumentum, ams-OSRAM, OSI Optoelectronics, Excelitas, TE Connectivity, Dexerials, Vishay, Ushio, onsemi, Albis Optoelectronics, EVERLIGHT, CLPT, LASER COMPONENTS Detector Group, SiFotonics, Marktech Optoelectronics, KODENSHI, and Optoway. These companies span the United States, Japan, Germany, Switzerland, Taiwan China, and other countries and regions, underscoring the highly international nature of the market. In terms of product coverage, some companies are active in both silicon-based and InGaAs products and serve industrial inspection, communications and data transmission, consumer electronics, and other applications, while others focus more deeply on specific high-end niches, building barriers in areas such as high-speed reception, long-wavelength detection, or specialized modules. Going forward, the key competitive issue will no longer be whether a company has a broad enough product catalog, but whether it can build platform-level capability across multiple high-growth application areas, serve industrial inspection, communication reception, intelligent terminals, and other specialized markets at the same time, and translate technology accumulation and customer collaboration into higher-quality growth.

Growth and Differentiation Will Coexist, and the Industry Will Become Increasingly Concentrated in High-Performance and High-Value Segments

Over the next several years, the global PIN photodiode market is likely to show simultaneous growth and differentiation. On one hand, total market size is expected to maintain solid expansion, especially with continued demand from industrial inspection, communications and data transmission, and other high-reliability specialized markets. On the other hand, lower-end standardized products may still face price pressure, while higher-end products are more likely to preserve stronger margins through performance advantages, qualification barriers, and customer stickiness. The attached data also indicate that by 2032, industrial inspection and analytical instruments together with communications and data transmission will generate a combined market size of more than USD 1 billion, further strengthening their dominance in the overall market structure. It is therefore reasonable to expect that the future direction of the industry will not be defined simply by shipment expansion, but by the simultaneous advance of higher performance, application specialization, regional supply chain diversification, and platform-based competition. For those watching the upgrading of the global optoelectronics industry, the PIN photodiode market now represents more than the growth of a single component category. It reflects the continued appreciation in value of optical sensing and high-speed receiving capability in the next phase of industrial transformation.

About The Authors

Ms Zhao. Senior Analyst

Beijing Hengzhou Bozhi International Information Consulting Co.,Ltd. (QYResearch CO.,LIMITED)

Room C1501,U-Center Building,No.28 Chengfu Road, Haidian District,Beijing,100083,China

Tel:+86-15600075800 (9.00am-6.00pm UTC+8), zhaopeihong@qyresearch.com

Website: www.qyresearch.com Hot Line:4006068865

Tel:+1-6262952442(US) +81-9038009273(JP) +44-8081110143(UK)

+86-1082945717(CN) +82-1075511278(KR) +91-9766478224(IN)

About QYResearch

QYResearch founded in California, USA in 2007.It is a leading global market research and consulting company. With over 17 years’ experience and professional research team in various cities over the world QY Research focuses on management consulting, database and seminar services, IPO consulting (data is widely cited in prospectuses, annual reports and presentations), industry chain research and customized research to help our clients in providing non-linear revenue model and make them successful. We are globally recognized for our expansive portfolio of services, good corporate citizenship, and our strong commitment to sustainability. Up to now, we have cooperated with more than 60,000 clients across five continents. Let’s work closely with you and build a bold and better future.

QYResearch is a world-renowned large-scale consulting company. The industry covers various high-tech industry chain market segments, spanning the semiconductor industry chain (semiconductor equipment and parts, semiconductor materials, ICs, Foundry, packaging and testing, discrete devices, sensors, optoelectronic devices), photovoltaic industry chain (equipment, cells, modules, auxiliary material brackets, inverters, power station terminals), new energy automobile industry chain (batteries and materials, auto parts, batteries, motors, electronic control, automotive semiconductors, etc.), communication industry chain (communication system equipment, terminal equipment, electronic components, RF front-end, optical modules, 4G/5G/6G, broadband, IoT, digital economy, AI), advanced materials industry Chain (metal materials, polymer materials, ceramic materials, nano materials, etc.), machinery manufacturing industry chain (CNC machine tools, construction machinery, electrical machinery, 3C automation, industrial robots, lasers, industrial control, drones), food, beverages and pharmaceuticals, medical equipment, agriculture, etc.

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 18 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp