MOCVD Equipment Market Summary

MOCVD (Metal-Organic Chemical Vapor Deposition) equipment is a critical tool in the semiconductor industry, used to grow high-quality compound semiconductor layers on substrates with atomic-scale precision. These layers, typically composed of materials such as gallium nitride (GaN), indium phosphide (InP), or gallium arsenide (GaAs), form the foundation for a wide range of electronic and optoelectronic devices. By precisely controlling factors such as layer thickness, composition, and doping, MOCVD systems enable the production of highly efficient and reliable devices.

MOCVD technology finds applications in multiple fields, including light-emitting diodes (LEDs), laser diodes, and power electronics. In the LED sector, MOCVD is the primary method for creating epitaxial layers that determine brightness, color quality, and energy efficiency. For power electronics, it enables the growth of GaN layers used in high-voltage transistors, electric vehicles, and renewable energy systems. The equipment is also essential for producing vertical-cavity surface-emitting lasers (VCSELs) and other laser diodes that are widely used in communication, sensing, and industrial applications.

The MOCVD process involves introducing metal-organic precursors and hydride gases into a heated reactor chamber, where they decompose and deposit as crystalline layers on a substrate. Maintaining precise control over temperature, gas flow, and pressure is crucial to achieve uniform, defect-free layers. Modern MOCVD systems often include multi-wafer reactors, automated substrate handling, and real-time process monitoring, which significantly improve productivity and consistency.

As a core technology in the semiconductor industry, MOCVD equipment directly impacts device performance, efficiency, and reliability. Its role continues to expand as demand grows for energy-efficient lighting, high-speed optical communication, and advanced power electronics, making it a cornerstone of modern electronics manufacturing.

Market Overview

Global MOCVD Equipment market size was valued at US$ 489.67 million in 2025 and is forecast to a readjusted size of USD 850.79 million by 2032 with a CAGR of 8.00% during review period.

The MOCVD equipment market has demonstrated sustained growth over recent years and is expected to continue this trajectory through the mid 2020s, driven by broad demand for compound semiconductor devices. Increased adoption of energy efficient LED lighting, demand for high performance laser diodes, and the rapid expansion of Gan based power electronics for electric vehicles and renewable energy systems are key growth catalysts. The expansion of optical communication infrastructure and next generation 5G networks also contributes to strong demand for high quality epitaxial materials produced by MOCVD systems. These synergistic drivers have collectively expanded both unit shipments and overall market value in multiple application segments.

Advancements in reactor design, automation, and process control are central themes identified in industry research. MOCVD equipment suppliers are focusing on improving throughput, uniformity, and multi wafer processing capabilities to meet the production needs of high-volume LED and power device manufacturers. Integration of real time process monitoring, predictive analytics, and advanced gas flow systems enhances yield consistency and reduces operating variability. Moreover, specialized equipment tailored for deep ultraviolet (DUV) LEDs and high efficiency GaN epitaxial layers reflects ongoing innovation aimed at addressing growing niche requirements and new device classes.

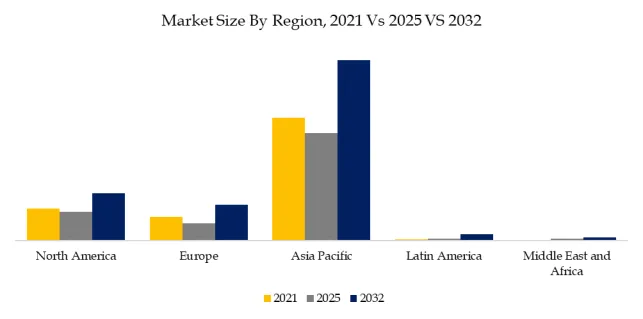

Asia Pacific continues to be the largest regional market for MOCVD equipment, supported by substantial investments in semiconductor manufacturing, LED production, and power device facilities in China, Japan, South Korea, and Taiwan. China, in particular, is increasing domestic MOCVD adoption as part of broader semiconductor self‑sufficiency initiatives, leading to both higher demand and the emergence of local equipment suppliers. North America and Europe remain important markets driven by advanced research, niche production for optical communications, and power electronics sectors. Geographic diversification of demand highlights the global nature of the MOCVD equipment landscape.

The competitive environment for MOCVD equipment is concentrated among well‑established global players who possess deep technological expertise and extensive intellectual property portfolios. High capital intensity, complex technology requirements, and long qualification cycles for new equipment limit the threat of new entrants. Leading suppliers differentiate themselves through advanced technology, after sales support, and strong customer relationships. Regional vendors are increasingly challenging international incumbents by offering cost competitive alternatives and localized service support, but the overall competitive rivalry remains anchored by long standing OEM leaders.

Despite robust growth prospects, the MOCVD equipment market faces constraints including high equipment costs, supply chain dependencies on precursor materials, and operational complexity. Environmental and safety regulations also necessitate ongoing investment in exhaust abatement and gas handling systems. Looking ahead, the market is expected to continue expanding as GaN and other compound semiconductor applications penetrate new sectors such as electric mobility, energy conversion, and LiDAR for autonomous systems. Continued innovation and capacity expansion will be critical for suppliers to address both current demand and emerging applications in the next decade.

Figure00001. Global MOCVD Equipment Market Size (US$ Million), 2025 vs 2032

Above data is based on report from QYResearch: Global MOCVD Equipment Market Report 2026-2032 (published in 2026). If you need the latest data, plaese contact QYResearch.

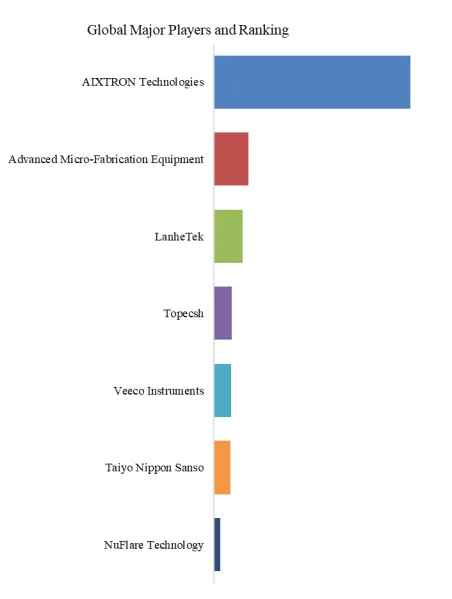

Figure00002. Global MOCVD Equipment Top 7 Players Ranking and Market Share (Ranking is based on the revenue of 2025, continually updated)

Above data is based on report from QYResearch: Global MOCVD Equipment Market Report 2026-2032 (published in 2026). If you need the latest data, plaese contact QYResearch.

According to QYResearch Top Players Research Center, the global key manufacturers of MOCVD Equipment include AIXTRON Technologies, Advanced Micro-Fabrication Equipment, etc. In 2025, the global top three players had a share approximately 81.0% in terms of revenue.

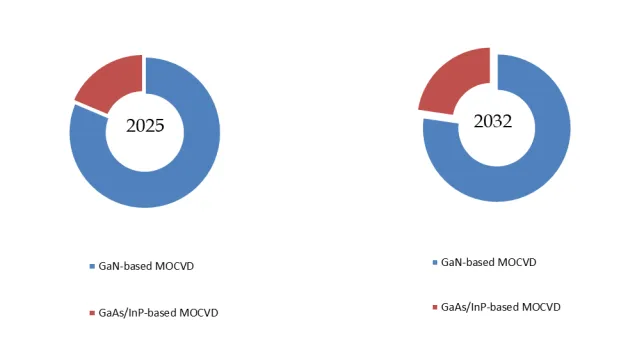

Figure00003. MOCVD Equipment, Global Market Size, Split by Product Segment

Based on or includes research from QYResearch: Global MOCVD Equipment Market Report 2026-2032.

In terms of product type, currently GaN-based MOCVD is the largest segment, hold a share of 81.37%.

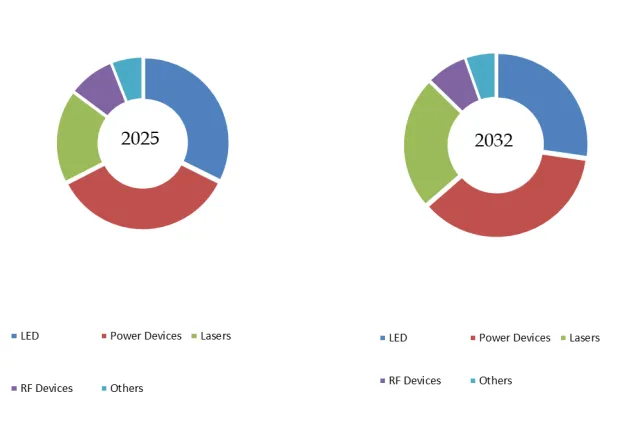

Figure00004. MOCVD Equipment, Global Market Size, Split by Applications Segment

Based on or includes research from QYResearch: Global MOCVD Equipment Market Report 2026-2032.

In terms of product application, currently Power Devices are the largest segment, hold a share of 35.10%.

Figure00005. MOCVD Equipment, Global Market Size, Split by Region

Based on or includes research from QYResearch: Global MOCVD Equipment Market Report 2026-2032.

About QYResearch

QYResearch founded in California, USA in 2007.It is a leading global market research and consulting company. With over 17 years’ experience and professional research team in various cities over the world QY Research focuses on management consulting, database and seminar services, IPO consulting (data is widely cited in prospectuses, annual reports and presentations), industry chain research and customized research to help our clients in providing non-linear revenue model and make them successful. We are globally recognized for our expansive portfolio of services, good corporate citizenship, and our strong commitment to sustainability. Up to now, we have cooperated with more than 60,000 clients across five continents. Let’s work closely with you and build a bold and better future.

QYResearch is a world-renowned large-scale consulting company. The industry covers various high-tech industry chain market segments, spanning the semiconductor industry chain (semiconductor equipment and parts, semiconductor materials, ICs, Foundry, packaging and testing, discrete devices, sensors, optoelectronic devices), photovoltaic industry chain (equipment, cells, modules, auxiliary material brackets, inverters, power station terminals), new energy automobile industry chain (batteries and materials, auto parts, batteries, motors, electronic control, automotive semiconductors, etc.), communication industry chain (communication system equipment, terminal equipment, electronic components, RF front-end, optical modules, 4G/5G/6G, broadband, IoT, digital economy, AI), advanced materials industry Chain (metal materials, polymer materials, ceramic materials, nano materials, etc.), machinery manufacturing industry chain (CNC machine tools, construction machinery, electrical machinery, 3C automation, industrial robots, lasers, industrial control, drones), food, beverages and pharmaceuticals, medical equipment, agriculture, etc.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp