Basic Power Distribution Unit Market Summary

Basic Power Distribution Units are non-intelligent power distribution units that provide multiple outlets to distribute electricity from a single input feed to IT and electrical loads in racks or equipment rooms. They typically include a metal housing, circuit breaker or fuse protection, power cord and plug, and standardized outlet types, but do not include network monitoring or outlet-level metering. Basic PDUs are valued for simplicity, low cost, and reliable power delivery, and are widely used in small server rooms, edge cabinets, telecom closets, labs, and cost-sensitive data center deployments where remote management is not required.

The industrial chain of Basic Power Distribution Units includes upstream sheet metal and plastics, copper busbars and wiring, outlets and connectors, breakers and fuses, power cords, plugs, indicators, and fasteners. Midstream covers electrical and mechanical design, punching and bending, assembly and wiring harnessing, insulation and grounding, safety and EMC compliance testing, and factory QA. Downstream users include enterprise IT rooms, colocation and edge sites, telecom equipment rooms, and industrial cabinets. Supporting services include configuration selection, installation, maintenance, spare parts, and replacement.

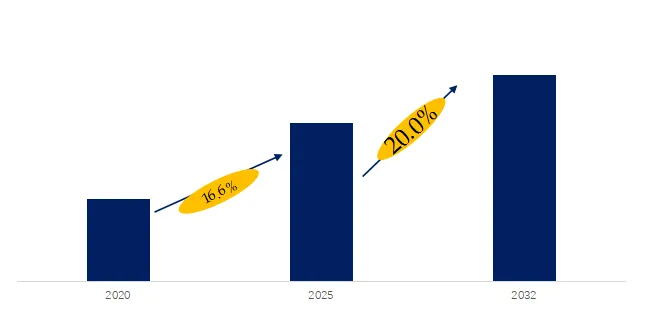

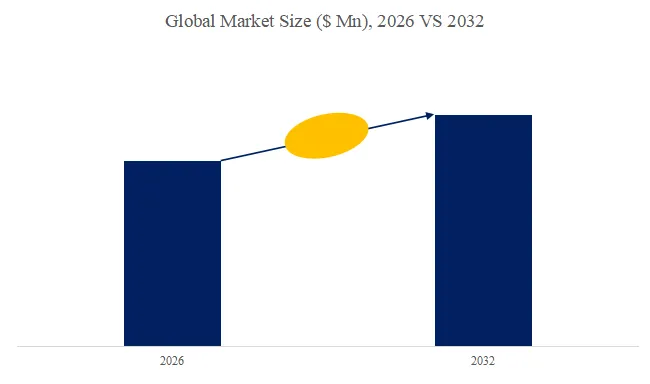

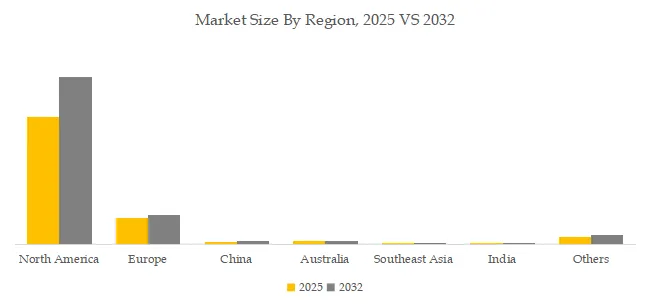

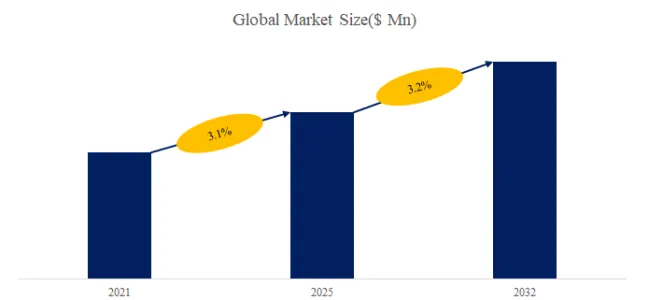

In 2025, global Basic Power Distribution Unit production reached approximately 3,300 k units,with an average global market price of around US$ 220 per unit, and a gross profit margin of approximately 20%-40%. According to the new market research report “Global Basic Power Distribution Unit Market Report 2026-2032”, published by QYResearch, the global Basic Power Distribution Unit market size is projected to reach USD 0.91 billion by 2032, at a CAGR of 3.2% during the forecast period.

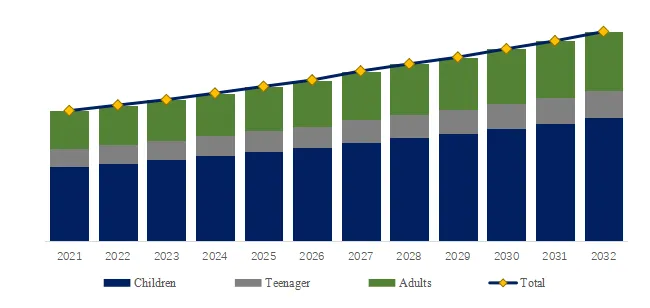

Global Basic Power Distribution Unit Market Size (US$ Million), 2020-2031

Above data is based on report from QYResearch: Global Basic Power Distribution Unit Market Report 2021-2032 (published in 2025). If you need the latest data, plaese contact QYResearch.

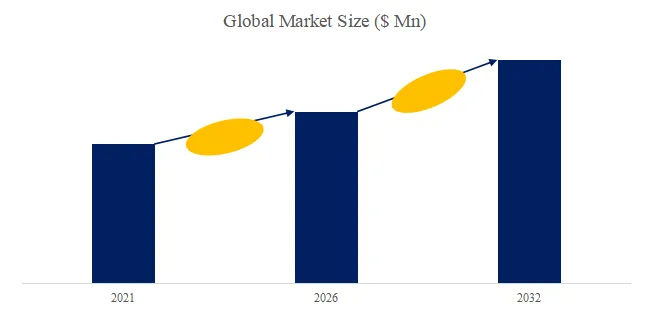

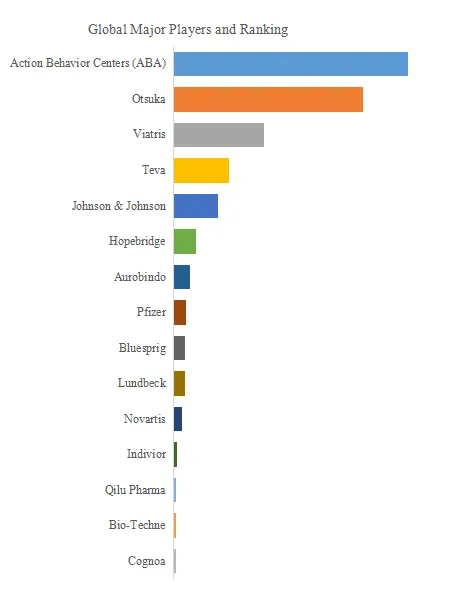

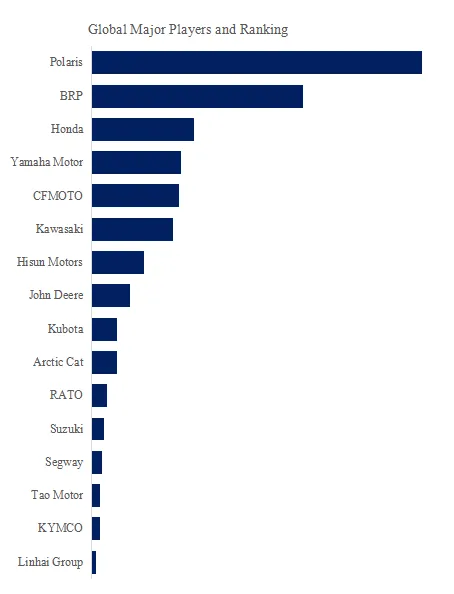

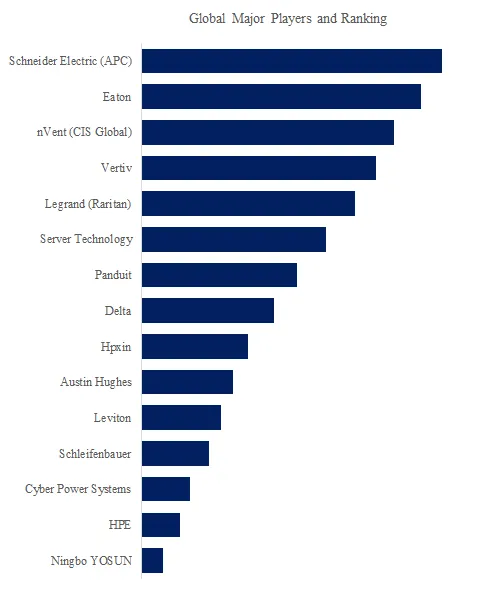

Global Basic Power Distribution Unit Top 5 Players Ranking and Market Share (Ranking is based on the revenue of 2025, continually updated)

Above data is based on report from QYResearch: Global Basic Power Distribution Unit Market Report 2026-2032 (published in 2025). If you need the latest data, plaese contact QYResearch.

According to QYResearch Top Players Research Center, the global key manufacturers of Basic Power Distribution Unit include Schneider Electric (APC), Eaton, nVent (CIS Global), Vertiv, Legrand (Raritan), Server Technology, Panduit, Delta, Hpxin, Austin Hughes, etc. In 2025, the global top five players had a share approximately 51.0% in terms of revenue.

Basic Power Distribution Unit Market Trends

1. Cost-effective and legacy demand keeps basic PDUs widely adopted

Basic PDUs remain widely used due to their simplicity, affordability, and compatibility with legacy data center infrastructure. Basic PDUs continue to dominate many installations because they provide a straightforward and low-cost solution for power distribution, especially in small to medium-sized facilities and developing markets. Their plug-and-play nature reduces installation complexity and minimizes operational risks, making them attractive for organizations that prioritize stability over advanced functionality. In large-scale deployments, standardized procurement strategies also favor basic units, as they simplify maintenance, spare parts management, and technician training across multiple sites.

2. Gradual shift toward compact, high-density rack configurations

Basic PDUs are evolving toward slimmer, high-outlet-density designs to support increasing rack power density. As data centers continue to increase computing capacity within limited rack space, there is a growing need for PDUs that can deliver power efficiently without occupying excessive physical space. This has driven the development of vertical and space-saving designs that allow more outlets per unit while maintaining airflow efficiency. Even in the basic PDU segment, manufacturers are improving structural durability and optimizing layouts to support higher device density and thermal demands.

3. Increasing integration readiness with intelligent and hybrid systems

Basic PDUs are increasingly designed to align with future upgrades toward intelligent power management systems. While basic PDUs lack advanced monitoring capabilities, market evolution is pushing vendors to design products that can coexist with or transition into smarter systems. This includes compatibility with broader data center infrastructure management (DCIM) frameworks and modular upgrade paths. As operators gradually adopt intelligent PDUs for critical workloads, basic units are often retained in less critical environments, creating hybrid deployment models. This transitional role ensures continued demand while enabling operators to balance cost and functionality.

Basic Power Distribution Unit Market Driving Factors and Opportunities

1. Rapid expansion of global data center infrastructure

The continuous growth of data centers worldwide is a primary driver for basic PDU demand. The surge in cloud computing, artificial intelligence, and digital services is leading to a rapid increase in data center construction across both developed and emerging regions. Each new facility requires reliable power distribution at the rack level, creating consistent demand for PDUs. Basic PDUs, due to their cost advantage, are often selected for non-critical or edge deployments where budget constraints are significant. Additionally, enterprise-owned data centers and smaller facilities continue to rely heavily on these solutions. As global digitalization accelerates, the expansion of IT infrastructure will remain a fundamental driver supporting sustained demand for basic PDUs.

2. Strong demand from cost-sensitive and edge computing environments

Basic PDUs benefit from growing adoption in edge and small-scale data center deployments. Edge computing environments, which are typically smaller and distributed, require simple and reliable power solutions without the added cost of advanced monitoring features. Basic PDUs fit well in these scenarios due to their affordability and ease of deployment. Similarly, developing regions and small enterprises often prioritize capital expenditure control, making basic PDUs a preferred choice. This creates a stable demand base even as high-end data centers shift toward intelligent systems. The expansion of edge infrastructure, including telecom sites and localized computing nodes, presents a significant opportunity for continued growth in this segment.

3. Opportunity in hybrid deployment and retrofit markets

Retrofitting legacy systems and hybrid deployments creates ongoing opportunities for basic PDUs. Many existing data centers operate with a mix of old and new infrastructure, requiring flexible and cost-effective upgrade strategies. Basic PDUs are often used in retrofit projects where full system replacement is not economically viable. They also serve as complementary components in hybrid setups, where intelligent PDUs are deployed selectively for critical racks while basic units support secondary loads. This approach allows operators to gradually modernize without significant upfront investment. As a result, retrofit demand and phased upgrade strategies represent a key opportunity area, extending the lifecycle and relevance of basic PDUs in an evolving market landscape.

About The Authors

| Zhangyu – Lead Author |

| Email:zhangyu@qyresearch.com |

About QYResearch

QYResearch founded in California, USA in 2007. It is a leading Global market research and consulting company. With over 17 years’ experience and professional research team in various cities over the world QY Research focuses on management consulting, database and seminar services, IPO consulting, industry chain research and customized research to help our clients in providing non-linear revenue model and make them successful. We are Globally recognized for our expansive portfolio of services, good corporate citizenship, and our strong commitment to sustainability. Up to now, we have cooperated with more than 60,000 clients across five continents. Let’s work closely with you and build a bold and better future.

QYResearch is a world-renowned large-scale consulting company. The industry covers various high-tech industry chain market segments, spanning the semiconductor industry chain (semiconductor equipment and parts, semiconductor materials, ICs, Foundry, packaging and testing, discrete devices, sensors, optoelectronic devices), photovoltaic industry chain (equipment, cells, modules, auxiliary material brackets, inverters, power station terminals), new energy automobile industry chain (batteries and materials, auto parts, batteries, motors, electronic control, automotive semiconductors, etc.), communication industry chain (communication system equipment, terminal equipment, electronic components, RF front-end, optical modules, 4G/5G/6G, broadband, IoT, digital economy, AI), advanced materials industry Chain (metal materials, polymer materials, ceramic materials, nano materials, etc.), machinery manufacturing industry chain (CNC machine tools, construction machinery, electrical machinery, 3C automation, industrial robots, lasers, industrial control, drones), food, beverages and pharmaceuticals, medical equipment, agriculture, etc.

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 18 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp