Global Leading Market Research Publisher QYResearch announces the release of its latest report “Fermented Corn Flour – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032″. Based on current situation and impact historical analysis (2021-2025) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Fermented Corn Flour market, including market size, share, demand, industry development status, and forecasts for the next few years.

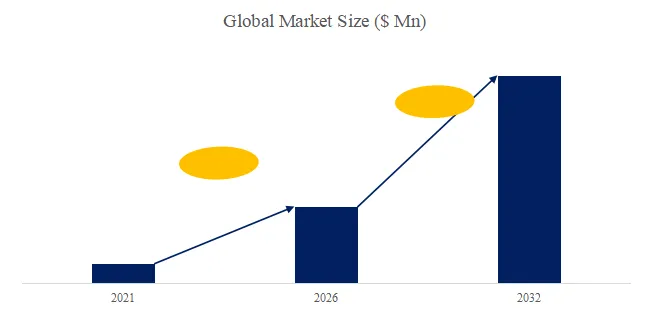

The global market for Fermented Corn Flour was estimated to be worth US185millionin2025andisprojectedtoreachUS185millionin2025andisprojectedtoreachUS275 million by 2032, growing at a CAGR of 5.8% from 2026 to 2032. For food industry executives, gluten-free product developers, and ethnic cuisine ingredient buyers, the core business imperative lies in offering fermented corn flour that addresses the growing demand for naturally fermented, gluten-free, and traditionally processed grain ingredients with enhanced nutritional profile (increased bioavailability of minerals, reduced anti-nutrients) and distinctive sour, tangy flavor (sourdough-like) used in baked goods, condiments, sauces, and traditional fermented beverages. Fermented corn flour is produced by soaking whole corn kernels in water (typically 12-48 hours), allowing natural lactic acid bacteria (LAB) and wild yeasts to ferment the grain, followed by drying and milling into fine flour. The fermentation process (traditional method across Africa (ogi, ogi-baba), Latin America (masa agria, sour masa), and Asia (Korean nokdumuk, Chinese fermented corn starch)) breaks down phytic acid (improving mineral absorption), degrades anti-nutrient compounds, partially hydrolyzes starches and proteins, and produces organic acids (lactic, acetic) creating characteristic sour, tangy flavor and extending shelf life (natural preservation). Applications include baked goods (sourdough-style cornbread, gluten-free bread, muffins, pancakes), condiments and sauces (fermented corn paste, African ogi porridge, Latin American sour atole), beverages (traditional fermented corn drinks), and others (thickening agent, porridge base, weaning food for infants).

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/5985694/fermented-corn-flour

The Fermented Corn Flour market is segmented as below:

Prathista Industries

Nkulenu Industries

Racines Bio

Oloye

LEVEKING

Segment by Type

Organic

Conventional

Segment by Application

Baked Goods

Condiments and Sauces

Beverage

Others

1. Market Drivers: Gluten-Free Demand, Clean Label Fermentation, and Traditional Foods Revival

Several powerful forces are driving the fermented corn flour market:

Gluten-free and ancient grain trends – Corn is naturally gluten-free (celiac disease 1%, gluten sensitivity 6-10%). Fermented corn flour positioned as heritage, naturally processed, clean label alternative to wheat flour (no additives, enzymes, dough conditioners). Gluten-free bakery sector (US$6+ billion) growing 8-10% annually. Fermented corn flour used in gluten-free breads (improved texture, moisture retention, flavor complexity).

Clean label and natural fermentation – Consumers avoid artificial preservatives (calcium propionate, sorbic acid, potassium sorbate) used in commercial bread. Naturally fermented corn flour has longer shelf life (lactic acid bacteria produce organic acids, natural mold inhibitors). Fermentation process perceived as “traditional,” “artisanal,” “minimally processed.” Bakers adopt for sourdough-style gluten-free products (distinguishing from mass-market gluten-free with starches, gums, artificial texture agents).

Functional and nutritional enhancement – Fermentation reduces phytic acid (20-50%), increasing bioavailability of iron, zinc, calcium. Increases protein digestibility (partial hydrolysis). Produces short-chain fatty acids (potential gut health benefits). Nutrient-enhanced fermented corn flour positioned for infant weaning foods (ogi, African fermented corn porridge), elderly nutrition (easier digestibility), and health-conscious consumers.

Recent market data (December 2025): According to Global Info Research analysis, conventional (non-organic) fermented corn flour dominates with approximately 72% revenue share, produced at scale (larger fermentation vessels, controlled drying, lower cost), used in food manufacturing and food service. Organic holds 28% share, fastest-growing (8-9% CAGR), with organic certification premium (30-50% higher price). Geographic consumption: Africa (35-40% of global volume, ogi, kenkey, banku domestic consumption), Asia (25-30%, China fermented corn starch, Korea), Latin America (15-20%, masa agria), North America and Europe (10-15%, growing specialty/ethnic grocery).

Application insights (November 2025): Baked goods represents largest segment with approximately 45% of fermented corn flour demand (gluten-free bread, cornbread, muffins, pancakes, cookies). Condiments and sauces account for 20% share (fermented corn paste, African ogi thickened sauces, sour masas for tamales). Beverages hold 15% share (traditional fermented corn drinks), fastest-growing (7-8% CAGR) in craft beverage and functional drink segments. Others (porridge base, weaning foods, thickening agent) at 20%.

2. Product Segmentation and Fermentation Process

| Type | Fermentation Method | Time | Flavor Profile | Key Regions | Share |

|---|---|---|---|---|---|

| Organic | Traditional submerged or dry fermentation, certified organic corn | 24-48 hours | Tangy, sour, complex | Export US/EU | ~28% |

| Conventional | Industrial scale (controlled tanks), or traditional small-scale | 12-48 hours | Mild to tangy | Domestic Africa/Asia/LatAm | ~72% |

Fermentation process: Dried corn kernels (field corn/dent corn, not sweet corn) cleaned, water-soaked (12-48 hours, steep water changed daily). Lactic acid bacteria (Lactobacillus plantarum, L. fermentum, L. casei) and yeasts (Candida, Saccharomyces) naturally present on grain initiate fermentation. Temperature 25-35°C. Fermentation progress monitored by pH drop (6.0 to 3.5-4.5), lactic acid accumulation, and flavor development (sour, acidic). Fermented corn drained, dried (sun-dried traditional, hot air oven industrial), milled to fine flour (60-150 mesh). Traditional wet-milled version (ogi) not dried, consumed as fermented paste; flour version dried for shelf stability.

Exclusive observation (Global Info Research analysis): Fermented corn flour remains predominantly traditional, small-scale, and localized in Africa (ogi in Nigeria, Ghana; kenkey in Ghana; uji in East Africa; banku in Ghana) and Latin America (masa agria, sour masa for tamales, Colombia, Mexico). Industrialized fermentation (controlled lactic acid bacteria starter cultures, standardized drying, milling) is limited but growing, primarily for export to North America and Europe diaspora markets and gluten-free bakery ingredient.

User case – Nigerian ogi production (December 2025): Nigerian traditional ogi (fermented corn starch porridge, weaning food). Process: corn wet-milled, fermented (2-3 days), sieved to remove bran, decanted (starch settles), paste dried. Ogi powder (instant, consumer adds hot water). Prathista Industries (Nigeria) produces packaged fermented corn flour (ogi powder) for urban convenience. Retail price (500g) US$1.50-2.50. Exported to UK/US (Nigerian diaspora).

User case – gluten-free sour cornbread (January 2026): US gluten-free bakery produces sourdough cornbread (fermented corn flour + rice flour + potato starch). Product: tangy, moist, 100% gluten-free. Fermented corn flour supplier: Racines Bio (France) or LEVEKING (China). Annual volume: 50 metric tons fermented corn flour. Specification: organic, pH 4.2-4.5, lactic acid 1.5-2.0%, fine grind (100 mesh). Marketing: “traditional fermentation, no preservatives, natural sourdough, made with heirloom corn.” Retail price US$6-8 per loaf (premium gf bread).

3. Technical Challenges

Fermentation control and standardization – Traditional natural fermentation (wild LAB and yeast) produces variable flavor, acidity, drying time, final flour quality (baking performance). Industrial producers use defined starter cultures (single or mixed LAB strains) and controlled temperature and time (fermentation tanks, pH monitoring) for consistent product. Starters increase cost but enable B2B food manufacturing (consistent baking results).

Aflatoxin contamination risk – Corn susceptible to aflatoxin (mold Aspergillus flavus, A. parasiticus) during field growth, harvest, and storage. Aflatoxin heat-stable, survives fermentation, drying, baking. Contaminated fermented corn flour causes acute toxicity (liver damage) and chronic cancer risk. African and Asian suppliers face aflatoxin monitoring (export rejected if exceeds EU/Japan/US limits). Good Agricultural Practices (GAP), rapid drying, proper storage, sorting, testing essential. Exporters contract third-party lab testing (ELISA, HPLC).

Technical difficulty – flavor intensity balance: Typical fermented corn flour pH 3.8-4.5 (moderately sour). Traditional African ogi pH 3.5-4.0 (strong sour flavor). North American/European consumers prefer milder sourness (pH 4.5-5.0) for baked goods (cornbread, muffins) and sauces. Manufacturers offer “mild” (shorter fermentation, pH 4.5-5.0) and “traditional” (longer, pH 3.5-4.5) product lines. Application dependent: sauces and condiments can tolerate stronger sourness, baked goods prefer mild.

Technical development (October 2025): LEVEKING (China) developed standardized starter culture for fermented corn flour (L. plantarum + L. brevis + yeast Torulaspora delbrueckii). Starter added to corn steeping water, controls fermentation time (12-18 hours), final pH target 4.2-4.5 ±0.2. Reduces batch-to-batch variation, enables industrial scale production (multi-ton fermentation vessels). Starters available for export to Africa and Latin America.

4. Competitive Landscape

Key players include: Prathista Industries (Nigeria – ogi, fermented corn flour, African market), Nkulenu Industries (Ghana – traditional fermented corn products (kenkey, banku), export diaspora), Racines Bio (France – organic fermented corn flour, gluten-free bakery ingredient, Europe), Oloye (Nigeria – ogi), LEVEKING (China – fermented corn flour, industrial starter cultures, export). Many small-scale local producers (unbranded, informal sector) not listed control significant domestic volume (Africa, Latin America, Asia). Formal industrial producers serve urban retail and export.

Regional dynamics: Africa largest producer, consumer (50-55% global volume) primarily for domestic ogi, kenkey, banku, porridge (subsistence and informal markets). Asia (China, Korea, Japan) 25-30% share (fermented corn starch, traditional beverages). Latin America (15-20%, Colombia, Mexico, Brazil). North America, Europe (5-10%, growth importing for gluten-free bakery and diaspora communities). Formal industrial sector (packaged, branded) growing 8-10% CAGR with urbanization and convenience demand.

5. Outlook

Fermented corn flour market will grow at 5.8% CAGR to US$275 million by 2032, driven by gluten-free bakery demand, clean label natural fermentation, and traditional foods commercialization (African, Latin American cuisine expanding globally). Technology trends: defined starter cultures (consistent fermentation, industrial scale), aflatoxin mitigation (biocontrol, rapid testing, GAP), and organic certified production (export premium). Regional growth: North America, Europe fastest-growing (8-10% CAGR) from small base; Africa, Asia, LatAm moderate (5-6% CAGR). Applications diversification: gluten-free bread, functional beverages, and clean-label sauces.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp