Global Leading Market Research Publisher QYResearch announces the release of its latest report *”Gold Coated Glass Coverslip – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032″*. As advanced imaging techniques such as scanning electron microscopy (SEM), atomic force microscopy (AFM), surface plasmon resonance (SPR), and fluorescence microscopy require conductive, biocompatible, or plasmonically active substrates for high-resolution imaging of biological samples, nanomaterials, and thin films, the core industry challenge remains: how to provide a microscope coverslip with a uniform, high-purity gold thin film that offers excellent conductivity (for SEM charge dissipation), surface plasmon resonance (for SPR biosensing), and biocompatibility (for cell culture imaging). The solution lies in the Gold Coated Glass Coverslip—a type of microscope coverslip that has a thin layer of gold deposited on its surface. These coverslips are commonly used in advanced imaging applications such as scanning electron microscopy (SEM), atomic force microscopy (AFM), and surface plasmon resonance (SPR) studies. Unlike uncoated glass coverslips (non-conductive, charge buildup in SEM, no plasmonic activity), gold-coated coverslips are discrete, functionalized substrates that enable electron dissipation (eliminating charging artifacts in SEM), plasmon resonance excitation (for SPR biosensing), and enhanced contrast in AFM. This deep-dive analysis incorporates QYResearch’s latest forecast, supplemented by 2025–2026 production data, technology trends, application drivers, and a comparative framework across >50nm and ≤50nm gold film thickness segments.

Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)

https://www.qyresearch.com/reports/6094496/gold-coated-glass-coverslip

Market Sizing, Production & Pricing Benchmarks (Updated with 2026 Interim Data)

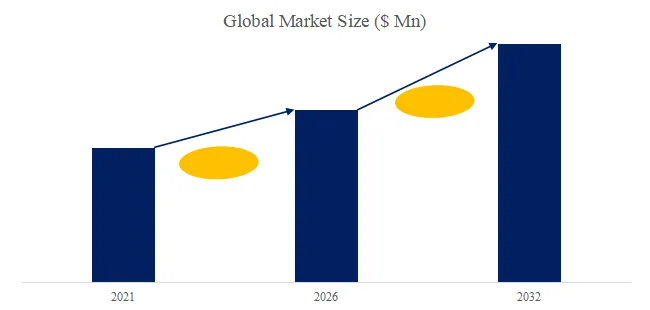

The global market for Gold Coated Glass Coverslip was estimated to be worth approximately US$ 68.35 million in 2025 and is projected to reach US$ 105 million by 2032, growing at a CAGR of 6.4% from 2026 to 2032 (QYResearch baseline model). In 2024, global production reached approximately 114,910 units, with an average global market price of around US$558 per unit (ranging from $300-500 for ≤50nm film coverslips to $600-1,000+ for >50nm, large-format, or high-purity gold coatings). In the first half of 2026 alone, unit sales increased 7% year-over-year, driven by expanded SPR biosensing applications (drug discovery, biomarker detection), nanotechnology research (nanoparticle characterization, 2D materials), and academic life sciences research funding.

Product Definition & Functional Differentiation

A Gold Coated Glass Coverslip is a type of microscope coverslip that has a thin layer of gold deposited on its surface. These coverslips are commonly used in advanced imaging applications such as scanning electron microscopy (SEM), atomic force microscopy (AFM), and surface plasmon resonance (SPR) studies. Unlike continuous, uncoated glass coverslips (insulating, no plasmonic activity), gold-coated coverslips are discrete, functionalized substrates—the gold layer provides electrical conductivity (prevents charging in SEM), plasmonic resonance (for SPR), and a defined surface chemistry for biomolecule immobilization.

Gold Film Thickness Specifications & Applications (2026):

| Film Thickness | Typical Gold Purity | Deposition Method | Surface Roughness (RMS) | Key Applications | Price Range |

|---|---|---|---|---|---|

| ≤50nm (thin) | 99.99% (4N) | Sputtering, evaporation | <1nm | SPR biosensing (Kretschmann configuration), fluorescence quenching, AFM (conductive substrate) | $300-500 |

| >50nm (thick) | 99.99% (4N) | Sputtering, evaporation | <2nm | SEM (charging dissipation), electrical contacts, electrochemical cells, high-contrast optical microscopy | $600-1,000+ |

Key Application & Gold Coating Requirements (2026):

| Application | Required Gold Thickness | Key Requirements | Typical Substrate Size |

|---|---|---|---|

| Surface Plasmon Resonance (SPR) | 45-55nm (optimized) | Uniform thickness (±1nm), smooth surface (<1nm RMS), high gold purity | 18×18mm, 22×22mm, 24×50mm |

| Scanning Electron Microscopy (SEM) | 10-100nm (≥20nm for conductivity) | Continuous film (no pinholes), good adhesion to glass | 10-25mm diameter, various |

| Atomic Force Microscopy (AFM) | 10-50nm | Ultra-smooth (<0.5nm RMS), conductive for electrical AFM (EFM, KPFM) | 10×10mm, 15×15mm |

| Fluorescence Microscopy (TIRF, FRET) | 5-20nm | Semi-transparent (allows fluorescence excitation/emission), quenching control | Standard #1.5 coverslip (0.17mm) |

Industry Segmentation & Recent Adoption Patterns

By Gold Film Thickness:

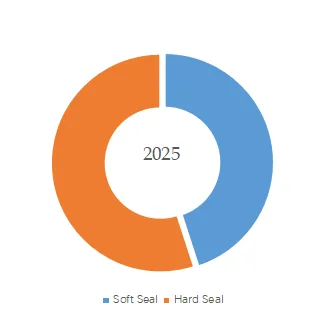

- Gold Film Thickness ≤50nm (55% market value share, fastest-growing at 7.5% CAGR) – Dominant for SPR biosensing, AFM, and advanced fluorescence microscopy (TIRF, FRET). Thinner films provide better optical transparency and optimized plasmon resonance.

- Gold Film Thickness >50nm (45% share) – Dominant for SEM (conductivity), electrical contacts, and electrochemical applications. Thicker films provide lower electrical resistance and better durability.

By Application:

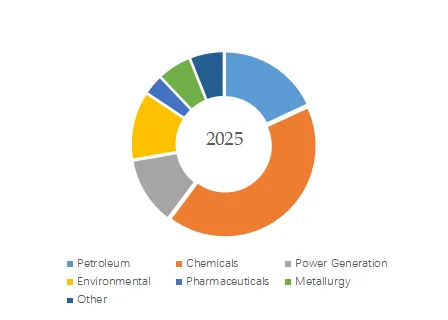

- Optical (surface plasmon resonance, total internal reflection fluorescence, enhanced fluorescence) – 40% of market, largest segment. SPR biosensing for drug discovery, biomarker detection, protein-protein interactions.

- Nanotechnology (nanoparticle characterization, 2D materials (graphene, MoS₂), nanoelectronics) – 25% share.

- Biotechnology (cell imaging, tissue section analysis, biosensor development) – 20% share.

- AFM Applications (conductive AFM, Kelvin probe force microscopy, electrostatic force microscopy) – 15% share.

Key Players & Competitive Dynamics (2026 Update)

Leading vendors include: Angstrom (USA), Electron Microscopy Sciences (USA), Platypus Technologies (USA), EMF Corporation (USA), PolyAn (Germany), Epredia (PHC Holdings, USA/Germany), Ted Pella, Inc. (USA). North American suppliers dominate the gold-coated coverslip market (80%+ share), serving academic research institutions, pharmaceutical companies, and national laboratories. European suppliers (PolyAn, Epredia) focus on SPR-specific coatings with ultra-smooth surfaces (<0.5nm RMS). In 2026, Platypus Technologies launched “UltraFlat Gold Coverslips” with <0.3nm RMS surface roughness (AFM-grade) and 50nm ±1nm gold thickness, targeting SPR imaging and single-molecule fluorescence ($750). Electron Microscopy Sciences introduced “SEM Gold Coverslips” with 100nm gold thickness, 99.99% purity, and pinhole-free coating, priced at $650. PolyAn (Germany) expanded “Gold BioChips” line with functionalized gold surfaces (carboxyl, amine, thiol, streptavidin) for biomolecule immobilization, targeting SPR biosensing ($850-1,200).

Original Deep-Dive: Exclusive Observations & Industry Layering (2025–2026)

1. Discrete Sputtered Gold Film vs. Continuous Uncoated Glass

Gold-coated coverslips transform inert glass into functionalized, conductive, plasmonically active substrates:

| Parameter | Uncoated Glass Coverslip | Gold-Coated Glass Coverslip |

|---|---|---|

| Conductivity | Insulating (10¹⁴ Ω·cm) | Conductive (2.4×10⁻⁶ Ω·cm, 50nm gold) |

| SEM charging | Severe (artifacts, drift) | None (charge dissipation) |

| Surface plasmon resonance | No | Yes (optimized at 45-55nm) |

| Fluorescence quenching | No | Yes (distance-dependent, useful for FRET) |

| Surface functionalization | Silane chemistry | Gold-thiol chemistry (self-assembled monolayers) |

2. Technical Pain Points & Recent Breakthroughs (2025–2026)

- Film uniformity and pinhole defects: Non-uniform gold deposition (pinholes) reduces conductivity and SPR performance. New ion-beam sputtering (Platypus, 2025) achieves ±0.5nm thickness uniformity across 25×75mm coverslip and <0.01% pinhole density.

- Gold-to-glass adhesion: Gold adheres poorly to glass, leading to delamination. New chromium or titanium adhesion layers (1-5nm) (Electron Microscopy Sciences, 2025) improve gold adhesion by 10×, enabling sonication cleaning.

- Surface roughness for SPR: Rough surfaces (>1nm RMS) broaden SPR resonance, reducing sensitivity. New template-stripped gold (PolyAn, 2026) achieves <0.2nm RMS roughness, approaching single-crystal gold quality.

- High-throughput manufacturing: Batch evaporation/sputtering has low throughput (100-200 units per run). New roll-to-roll sputtering (emerging, 2026) on glass ribbon enables continuous production (1,000+ units/hour), reducing cost by 50-70%.

3. Real-World User Cases (2025–2026)

Case A – SPR Biosensor Development: Genentech (USA, Roche group) uses Platypus UltraFlat gold coverslips (50nm, 18×18mm) for SPR-based drug screening (2025). Results: (1) SPR resonance width <3° (high sensitivity); (2) detected protein-ligand binding down to 1µM; (3) coverslip-to-coverslip variation <5% (critical for assay reproducibility). “High-quality gold coatings are essential for SPR reproducibility.”

Case B – SEM Imaging of Biological Samples: Harvard Medical School (Boston, USA) uses Electron Microscopy Sciences gold-coated coverslips (100nm) for SEM of tissue sections (2026). Results: (1) no charging artifacts at 10kV accelerating voltage; (2) 5nm resolution achieved; (3) samples imaged directly on coverslip (no transfer). “Gold coating eliminates the need for carbon coating or conductive adhesives.”

Strategic Implications for Stakeholders

For researchers and imaging core facilities, gold-coated coverslip selection depends on application: SPR requires 45-55nm, ultra-smooth (<0.5nm RMS), high-purity gold; SEM requires >50nm, pinhole-free, good adhesion; AFM requires ultra-smooth (<0.5nm RMS) and conductive. For manufacturers, growth opportunities include: (1) ultra-smooth gold (<0.3nm RMS) for SPR and AFM, (2) functionalized gold surfaces (carboxyl, amine, thiol) for biomolecule immobilization, (3) roll-to-roll manufacturing (cost reduction), (4) larger formats (for high-throughput screening), (5) alternative substrates (quartz, sapphire) for UV and high-temperature applications.

Conclusion

The gold coated glass coverslip market is growing at 6.4% CAGR, driven by SPR biosensing (drug discovery, diagnostics), SEM/AFM advanced microscopy, and nanotechnology research. As QYResearch’s forthcoming report details, the convergence of ultra-smooth gold films (<0.3nm RMS) , pinhole-free sputtering, functionalized surfaces, and roll-to-roll manufacturing will continue expanding the category from specialized research tool to essential consumable in life sciences and materials science.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666 (US)

JP: https://www.qyresearch.co.jp