Inhaled Nitric Oxide Market Summary

Inhaled Nitric Oxide, or iNO, should be understood first as a medical gas product for inhalation rather than as a hardware-based therapy platform. Its core clinical value lies in its role as a selective pulmonary vasodilator that improves oxygenation and reduces pulmonary vascular resistance, especially in neonatal hypoxic respiratory failure associated with pulmonary hypertension and other highly specialized critical care scenarios. From a market research perspective, the correct statistical boundary is the commercial value of the gas product itself, excluding delivery systems, monitoring devices, and other hardware revenues. Once that boundary is clarified, the industry logic becomes much clearer. This is not a conventional pharmaceutical market driven by broad patient penetration. It is a high-barrier specialized therapeutic gas market shaped by clinical necessity, regulatory qualification, purity control, supply reliability, and hospital access capability.

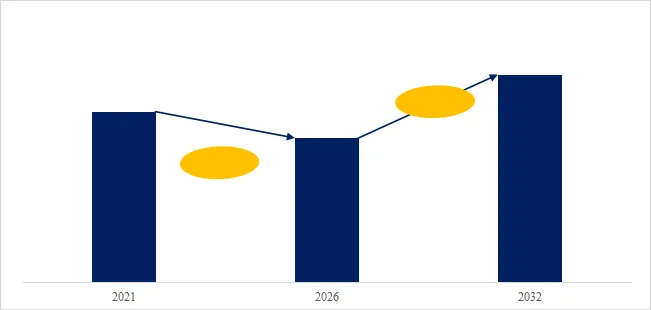

At the global level, Inhaled Nitric Oxide is not among the loudest healthcare segments, yet it is one of the clearest examples of a high-quality specialty market with durable value. The global iNO market is about USD 730 million in 2025 and is expected to reach approximately USD 1.08 billion by 2032. What matters is not only that the market is expanding, but that its expansion is supported by the strengthening role of Inhaled Nitric Oxide as a high-value therapeutic gas in critical care. The category is moving beyond its earlier identity as a narrowly defined specialist treatment segment and is becoming a higher-quality therapeutic gas market shaped by clinical necessity, supply capability, and professional value. For corporate leaders and investors, that makes the category more attractive than its absolute size alone might suggest. Growth is not driven by blind expansion, but by rigid critical care demand, deeper standardization of hospital use, and the growing indispensability of specialized therapeutic gas in advanced healthcare systems.

Figure00001. Global Inhaled Nitric Oxide Market Size (US$ Million), 2021-2032

Above data is based on report from QYResearch: Global Inhaled Nitric Oxide Market Report 2025-2031 (published in 2025). If you need the latest data, plaese contact QYResearch.

Demand is supported not only by patient need, but by hospital dependence on high-standard therapeutic gas supply

The most important structural driver of the iNO market is the stability of its clinical demand base. Its core established use remains concentrated in neonatal hypoxic respiratory failure and related pulmonary vascular support, giving the category a highly visible foundation of medical necessity. At the same time, neonatal persistent pulmonary hypertension remains the most important pillar supporting global demand and clearly outweighs broader exploratory uses. That concentration is highly meaningful. It shows that demand is not scattered across speculative indications, but concentrated in high-evidence, high-barrier, and high-priority clinical scenarios. Markets with that kind of demand structure are often more resilient, more profitable, and easier to defend over time. As NICU, PICU, and advanced critical care capabilities continue to improve globally, demand for high-purity, stable, and consistently supplied nitric oxide gas products is likely to remain firm.

High-purity products dominate, and specialized supply capability defines the competitive ceiling

Inhaled Nitric Oxide is not simply an extension of the industrial gases market. It is a specialty therapeutic gas segment with exceptionally demanding requirements for purity, compliance, consistency, and clinical suitability. High-purity iNO holds the dominant share of the global market, while standard-purity products account for only a small portion. This is a critical signal because it shows that competition is not primarily about who can supply gas in generic terms. It is about who can reliably provide clinically acceptable, high-quality medical gas under strict regulatory and hospital standards. In practical terms, the competitive ceiling is determined less by nominal production capacity than by compliance systems, quality assurance, purity management, cylinder supply, regional logistics, and hospital-facing commercial execution. For CEOs and marketing leaders, this is exactly what makes the market strategically attractive. It is much less vulnerable to simple low-price disruption and far more likely to concentrate value in qualified leaders.

The competitive landscape is highly concentrated, with leadership built on qualification, channels, and supply capability

The global iNO market already shows a very strong concentration profile. Major competitors are concentrated in leading companies with strong foundations in medical gases, hospital channel access, and global supply capability. Such concentration does not mean the market lacks opportunity. It means that the threshold for meaningful participation is extremely high. Products must meet medical-grade purity and registration requirements. Supply systems must be stable enough to support hospitals without interruption. In critical care, customers are highly sensitive to brand credibility, validation history, and compliance records. This makes early movers and established suppliers much harder to displace. In this sense, Inhaled Nitric Oxide is better understood as a high-regulation, high-trust, and high-fulfillment therapeutic gas market rather than a standard specialty gas category. The advantage of leaders is reflected not only in sales and revenue, but in the deep and durable trust they have built with hospital systems.

North America remains the anchor market, and regional growth depends on clinical infrastructure maturity

Regional structure further confirms the professional nature of this market. North America remains the dominant global market, followed by Europe and Asia-Pacific, while the rest of the world represents a relatively small share. This pattern is not surprising. The use of Inhaled Nitric Oxide depends heavily on mature neonatal intensive care systems, reliable hospital procurement capacity, and developed medical gas distribution networks. North America’s long-standing leadership is therefore a reflection of strong hospital infrastructure, advanced specialty care pathways, and standardized clinical use. The same logic will continue to shape future regional growth. Markets with stronger critical care systems will be better positioned to translate clinical need into real gas product demand. For Asia-Pacific and other emerging regions, opportunity will depend less on population size alone and more on specialty care expansion, hospital upgrading, and improved access to high-end therapeutic gas supply.

The supply chain is clear, and the core barrier lies not in hardware, but in therapeutic gas production and supply

Under the correct statistical boundary, the iNO supply chain should be understood in direct relation to the gas product itself. Upstream activities include nitric oxide production, medical gas raw material support, purification, cylinders and packaging systems, and related quality control. Midstream consists of the production, filling, registration, and supply of Inhaled Nitric Oxide gas products. Downstream demand comes from NICUs, PICUs, ICUs, and hospital procurement and distribution systems. In this market, the key value in the supply chain does not sit in hardware complexity, but in the ability to build a compliant, stable, continuous, and hospital-oriented commercial network for therapeutic gas. In other words, the business model is first a gas product sales model and then a scale model built on regional channels, hospital access, and long-term supply relationships. The real prize is not abstract platform ownership, but long-term share of therapeutic gas demand in high-level hospital systems.

What QYResearch highlights is not only market expansion, but the long-term value of a high-quality specialty segment

Taken together, the market size trajectory, application structure, product mix, competitive concentration, and regional distribution all point to the same conclusion. Inhaled Nitric Oxide is a classic example of a market that is moderate in size but exceptionally high in quality. It does not rely on mass-market penetration, nor is it an easily substitutable standardized category. It is a long-duration specialty market grounded in clear indications, therapeutic gas characteristics, hospital access barriers, and supply capability. For corporate leadership, it represents a strategic high ground within medical gases. For marketing executives, it is a long-term opportunity built on specialist hospital penetration and trust. For investors, it is a concentrated, resilient, and clearly structured niche with meaningful room for expansion. That is why the most important story is not only how the market grows from 2025 to 2032, but how its strategic position and long-term value within global critical care continue to be redefined.

About The Authors

Ms Zhao. Senior Analyst

Beijing Hengzhou Bozhi International Information Consulting Co.,Ltd. (QYResearch CO.,LIMITED)

Room C1501,U-Center Building,No.28 Chengfu Road, Haidian District,Beijing,100083,China

Tel:+86-15600075800 (9.00am-6.00pm UTC+8), zhaopeihong@qyresearch.com

Website: www.qyresearch.com Hot Line:4006068865

Tel:+1-6262952442(US) +81-9038009273(JP) +44-8081110143(UK)

+86-1082945717(CN) +82-1075511278(KR) +91-9766478224(IN)

About QYResearch

QYResearch founded in California, USA in 2007.It is a leading global market research and consulting company. With over 17 years’ experience and professional research team in various cities over the world QY Research focuses on management consulting, database and seminar services, IPO consulting (data is widely cited in prospectuses, annual reports and presentations), industry chain research and customized research to help our clients in providing non-linear revenue model and make them successful. We are globally recognized for our expansive portfolio of services, good corporate citizenship, and our strong commitment to sustainability. Up to now, we have cooperated with more than 60,000 clients across five continents. Let’s work closely with you and build a bold and better future.

QYResearch is a world-renowned large-scale consulting company. The industry covers various high-tech industry chain market segments, spanning the semiconductor industry chain (semiconductor equipment and parts, semiconductor materials, ICs, Foundry, packaging and testing, discrete devices, sensors, optoelectronic devices), photovoltaic industry chain (equipment, cells, modules, auxiliary material brackets, inverters, power station terminals), new energy automobile industry chain (batteries and materials, auto parts, batteries, motors, electronic control, automotive semiconductors, etc.), communication industry chain (communication system equipment, terminal equipment, electronic components, RF front-end, optical modules, 4G/5G/6G, broadband, IoT, digital economy, AI), advanced materials industry Chain (metal materials, polymer materials, ceramic materials, nano materials, etc.), machinery manufacturing industry chain (CNC machine tools, construction machinery, electrical machinery, 3C automation, industrial robots, lasers, industrial control, drones), food, beverages and pharmaceuticals, medical equipment, agriculture, etc.

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 18 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp