Man-made Leather Market Summary

Man-made leather is a leather-like material formed by combining polyurethane, PVC, and other polymer-based surface systems with woven fabrics, knitted fabrics, nonwovens, or microfiber substrates through coating, lamination, foaming, embossing, and finishing processes. Its value lies not only in replicating the texture, appearance, and tactile qualities of genuine leather, but also in delivering thickness consistency, color stability, strong processing adaptability, scalable continuous production, and the ability to optimize performance in areas such as abrasion resistance, weatherability, low-VOC behavior, cleanability, softness, and lightweight construction. After years of technological development, the industry has expanded into multiple product routes, including PVC, conventional PU, microfiber PU, and ecological functional PU, with broad applications across apparel accessories, furnishing, automotive interiors, sports goods, and a wide range of consumer and industrial surface applications. At this stage of industrial upgrading, man-made leather is no longer merely an alternative to genuine leather. It has become an important advanced materials category positioned at the intersection of green manufacturing, product design, functional performance, and brand value expression.

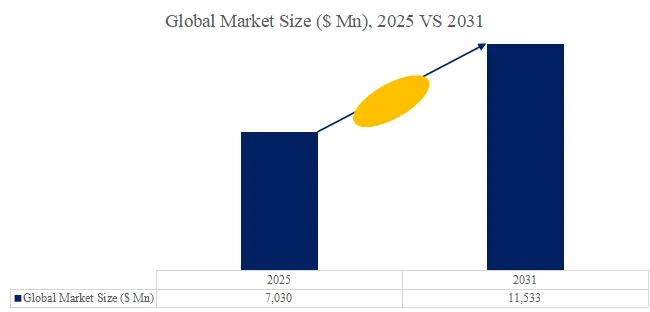

According to QYResearch’s latest report, Global Man-made Leather Market Report 2026-2032, the global and China man-made leather industries have entered a more visible and resilient expansion cycle. Using 2025 as the reference point, the global market is estimated at about USD 23.08 billion and is expected to rise to approximately USD 37.79 billion by 2032, representing a CAGR of about 7.1% during 2026-2032. Over the same period, the China market is estimated at about USD 6.66 billion and is projected to increase to roughly USD 11.54 billion by 2032, with a CAGR of about 8.17%. These figures indicate more than a simple recovery in demand. They reflect a simultaneous upgrade in product structure, application hierarchy, and value creation. The global market continues to expand steadily, while China remains a key arena for manufacturing capability, demand upgrading, and product iteration. For executives, commercial decision-makers, and investors, man-made leather is no longer a conventional materials segment driven mainly by cost advantages. It is increasingly a value-oriented industry supported by technological advancement, consumer upgrading, and manufacturing renewal.

Figure00001. Global Man-made Leather Market Size (US$ Million), 2021-2032

Above data is based on report from QYResearch: Global Man-made Leather Market Report 2025-2031 (published in 2025). If you need the latest data, plaese contact QYResearch.

Premium Applications Are Redefining the Industry’s Value Ceiling

One of the most important shifts in the market is that downstream demand is moving rapidly toward more demanding application scenarios. Apparel accessories remain the largest foundational demand segment worldwide, but the real expansion in industry upside is increasingly coming from automotive interiors, quality-oriented furnishing, athleisure consumption, and consumer applications that place greater emphasis on touch, comfort, and environmental credentials. As new-energy vehicles, integrated home furnishing solutions, premium sports-inspired lifestyles, and brand-focused design strategies continue to develop, customer expectations for materials have shifted from simple replacement to clear upgrading. Abrasion resistance, hydrolysis resistance, low odor, low emissions, lightweight construction, color consistency, easy maintenance, and reliable large-scale delivery are becoming central requirements for entry into high-quality customer systems. For that reason, future competition in man-made leather will no longer revolve mainly around price and appearance. It will increasingly be defined by a comprehensive mix of functional performance, green attributes, and application-specific suitability.

China’s Role Has Moved Far Beyond That of a Single Regional Market

China continues to strengthen its strategic role within the global industry map. Its importance is defined not only by scale, but also by its ability to shape the direction of industry upgrading. China combines relatively complete capabilities in resin systems, substrate supply, lamination and coating, surface finishing, and large-scale manufacturing, while also maintaining close coordination with downstream clusters in footwear, bags, furnishing, automotive components, and consumer product manufacturing. This ecosystem advantage allows China to respond more quickly to international customer requirements for new materials, new processes, and highly consistent delivery standards. It also gives domestic producers stronger resilience in new product introduction, process improvement, and commercial ramp-up. Over the coming years, China is expected to remain one of the world’s most important supply centers for man-made leather, while also serving as the most representative market for observing structural upgrading, downstream application shifts, and changes in customer preferences. The global market will continue to be defined by expansion, while China will continue to be defined by upgrading.

Green Processing and Material Upgrading Are Reshaping Competitive Thresholds

Toward 2032, competitive positioning will be determined far less by installed capacity alone and far more by green manufacturing capability and material upgrading capacity. As brand owners, automotive supply chains, and consumer goods markets continue to tighten their requirements around environmental compliance, traceability, low emissions, and sustainable materials, man-made leather producers are facing not only cost pressure, but also a deeper need to redesign both process systems and product portfolios. Conventional grades will remain an important part of the commercial base, but microfiber, ecological, and functional materials are becoming the more dynamic growth directions. The companies that gain stronger market recognition will not simply be those with larger installed capacity, but those able to build an integrated capability set across resin systems, substrate engineering, surface treatment, green processing, quality control, and collaborative customer development. This means that the industry’s future value creation will be driven increasingly by technical depth, customer quality, and product mix improvement rather than by low-cost substitution alone.

In a Fragmented Market, the Real Winners Will Emerge from High-Value Niches

The global man-made leather market still maintains a relatively low level of concentration. Leading manufacturers are strengthening their positions, but the market has not entered a highly monopolized stage. On a cautious 2025 basis, the combined market share of the global top five players is estimated at around 10%, indicating that the overall market remains broad and that many niche segments still offer room for continued restructuring. This is not a weakness. On the contrary, it suggests that premium niches remain highly capable of producing structural winners. The most competitive companies in the coming years are unlikely to be those trying to dominate every product line at once. They are more likely to be those establishing distinctive strengths in areas such as automotive-grade interior materials, microfiber synthetic leather, ecological functional PU, premium furnishing surfaces, or performance-oriented materials for sports-related consumer products. For corporate decision-makers, this is a competition shaped by product routes, customer quality, and long-term technical investment. For investors, it remains an industry with meaningful potential for the emergence of niche leaders and valuation re-rating opportunities.

Toward 2032, the Industry’s Appeal Will Be Defined by an Upgrading Logic Rather than a Substitution Logic

QYResearch’s latest market analysis makes one point especially clear: from a 2026 publication perspective, the defining feature of the global and China man-made leather markets is no longer simple substitution, but accelerated upgrading. The industry still retains its original role as an alternative to genuine leather, yet the real drivers of future growth are now green manufacturing, functional innovation, deeper penetration into premium applications, and stronger industry-chain coordination. The central question in the past was whether substitution could happen. The central question today is whether upgrading can be delivered. In the past, attention focused on supply scale. Today, attention is shifting toward product mix, customer tier, and long-term sustainability capability. Looking toward 2032, man-made leather is no longer simply a traditional materials industry. It is becoming a value-driven arena shaped simultaneously by new consumption patterns, new vehicles, new furnishing demands, and new manufacturing priorities. The companies that move earlier in green process transformation, enter premium application chains faster, and convert material capability into clearly perceived customer value will be best positioned to lead the next stage of reshaping in both the global and China markets.

About The Authors

Ms Zhao. Senior Analyst

Beijing Hengzhou Bozhi International Information Consulting Co.,Ltd. (QYResearch CO.,LIMITED)

Room C1501,U-Center Building,No.28 Chengfu Road, Haidian District,Beijing,100083,China

Tel:+86-15600075800 (9.00am-6.00pm UTC+8), zhaopeihong@qyresearch.com

Website: www.qyresearch.com Hot Line:4006068865

Tel:+1-6262952442(US) +81-9038009273(JP) +44-8081110143(UK)

+86-1082945717(CN) +82-1075511278(KR) +91-9766478224(IN)

About QYResearch

QYResearch founded in California, USA in 2007.It is a leading global market research and consulting company. With over 17 years’ experience and professional research team in various cities over the world QY Research focuses on management consulting, database and seminar services, IPO consulting (data is widely cited in prospectuses, annual reports and presentations), industry chain research and customized research to help our clients in providing non-linear revenue model and make them successful. We are globally recognized for our expansive portfolio of services, good corporate citizenship, and our strong commitment to sustainability. Up to now, we have cooperated with more than 60,000 clients across five continents. Let’s work closely with you and build a bold and better future.

QYResearch is a world-renowned large-scale consulting company. The industry covers various high-tech industry chain market segments, spanning the semiconductor industry chain (semiconductor equipment and parts, semiconductor materials, ICs, Foundry, packaging and testing, discrete devices, sensors, optoelectronic devices), photovoltaic industry chain (equipment, cells, modules, auxiliary material brackets, inverters, power station terminals), new energy automobile industry chain (batteries and materials, auto parts, batteries, motors, electronic control, automotive semiconductors, etc.), communication industry chain (communication system equipment, terminal equipment, electronic components, RF front-end, optical modules, 4G/5G/6G, broadband, IoT, digital economy, AI), advanced materials industry Chain (metal materials, polymer materials, ceramic materials, nano materials, etc.), machinery manufacturing industry chain (CNC machine tools, construction machinery, electrical machinery, 3C automation, industrial robots, lasers, industrial control, drones), food, beverages and pharmaceuticals, medical equipment, agriculture, etc.

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 18 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp