QY Research Inc. (Global Market Report Research Publisher) announces the release of 2025 latest report “Online Tutoring Service- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. Based on current situation and impact historical analysis (2020-2024) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Online Tutoring Service market, including market size, share, demand, industry development status, and forecasts for the next few years.

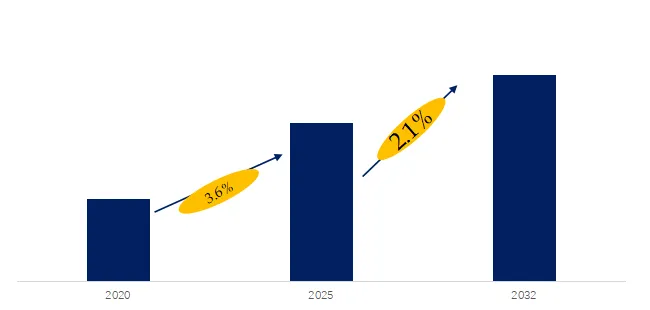

The global market for Online Tutoring Service was estimated to be worth US$ 14004 million in 2025 and is projected to reach US$ 16181 million, growing at a CAGR of 2.1% from 2026 to 2032.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/6035737/online-tutoring-service

1. Online Tutoring Service Market Summary

Online tutoring services refer to educational guidance and academic support services provided via the internet, designed to help students achieve better academic results and gain a deeper understanding of specific subject content. These services are typically delivered through video calls, instant messaging, homework assistance, mock tests, and customized learning plans, covering all levels from elementary school to university and even career development. Tutoring services can provide personalized guidance to individual students or be conducted in small groups, supporting a wide range of subject areas, including mathematics, science, language arts, and programming. The flexibility, convenience, and broad range of content offered by online tutoring make it an increasingly important part of the modern education system.

According to the latest research report from QYResearch, in terms of market size, the global Online Tutoring Service market size is projected to grow from USD 14 billion in 2025 to USD 14.2 billion by 2032, at a CAGR of 2.1% during the forecast period.

Figure00001. Global Online Tutoring Service Market Revenue Growth Rate, 2021-2032

Above data is based on report from QYResearch: Global Online Tutoring Service Market Report 2026-2032 (published in 2025). If you need the latest data, plaese contact QYResearch.

2 Introduction of Major Manufacturers of Online Tutoring Service

| Serial Number |

Company |

| 1 |

Acadecraft |

| 2 |

Gaotu Techedu Inc. |

| 3 |

New Oriental |

| 4 |

Beijing Fenbi Lantian Technology Company Ltd. |

| 5 |

Beijing Huatu Hongyang Network Technology Co., Ltd. |

| 6 |

Chegg, Inc |

| 7 |

TutorEye, Inc |

| 8 |

Varsity Tutors LLC |

| 9 |

Think & Learn Private Limited |

| 10 |

Vedantu Innovations Private Limited |

| 11 |

Xueda Education Group |

| 12 |

K12 Inc(Stride ) |

| 13 |

Unacademy |

| 14 |

Knowbox |

| 15 |

Ruanguru |

| 16 |

GoStudent |

| 17 |

ClubZ |

Source: Third-party data, QYResearch Research Team

According to a survey by QYResearch’s Leading Enterprise Research Center, global Online Tutoring Service manufacturers include Acadecraft, Gaotu Techedu Inc., New Oriental, Beijing Fenbi Lantian Technology Company Ltd., Beijing Huatu Hongyang Network Technology Co., Ltd., etc. By 2025, the top five global manufacturers will hold approximately 27% of the market share.

Introduction to Key Companies

Company 1

|

Description |

| Company Introduction |

Acadecraft is a leading global educational technology company focused on providing customized educational solutions. It is committed to providing high-quality content creation and training services to educational institutions, businesses, and individuals. The company boasts a professional team of educational experts who combine advanced technology to provide online learning solutions, curriculum development, assessment services, and educational content localization services. Acadecraft’s services cover all levels from K-12 to higher education and corporate training, providing innovative, flexible, and personalized learning experiences to clients worldwide. |

| Product Introduction |

Acadecraft’s online tutoring service aims to help students improve their academic performance through personalized learning support. The company offers online tutoring in various subjects, with course content tailored to students’ needs. Tutoring methods are flexible and diverse, including one-on-one live tutoring, interactive learning platforms, and self-paced learning resources. Acadecraft’s tutoring service combines real-time assessment and feedback to help students consolidate knowledge, solve learning difficulties, and boost confidence, providing comprehensive learning support and assurance of progress. |

Source: Third-party data, QYResearch Research Team

Company 2

|

Description |

| Company Introduction |

Gaotu is a leading online education company in China, focusing on providing online learning services in the K-12 and adult education sectors. The company offers online courses in subjects including Chinese, mathematics, and English through its advanced educational platform, utilizing AI technology and data analytics to provide students with personalized learning experiences. Gaotu Techedu aims to help students improve their academic performance, cultivate their comprehensive abilities, and drive the digital transformation of education in China through innovative teaching methods and efficient online educational resources. |

| Product Introduction |

Gaotu’s online tutoring service provides personalized learning support for K-12 students. Through real-time interactive live online classes, students can communicate directly with experienced teachers to resolve learning questions. Furthermore, Gaotu’s intelligent platform customizes personalized tutoring plans based on students’ learning progress and needs, helping them achieve better results in all subjects. Services include comprehensive subject tutoring, test preparation, and skills enhancement, aiming to provide students with all-round academic support to ensure maximum learning outcomes. |

Source: Third-party data, QYResearch Research Team

Company 3

|

Description |

| Company Introduction |

New Oriental Education & Technology Group, one of China’s largest comprehensive education and training institutions, was founded in 1993 and is committed to providing students with diversified educational products and services. The company offers a full range of services from language training to academic tutoring, vocational training, and overseas study consulting. With its rich educational experience and advanced teaching philosophy, New Oriental has nurtured a large number of students in China and globally, helping them achieve their academic and career goals. New Oriental’s teaching methods emphasize innovation and personalization, aiming to be a lifelong learning partner for students. |

| Product Introduction |

New Oriental’s online tutoring services provide students with flexible and efficient learning support, covering multiple areas including K-12 subjects, language learning, and test preparation. Through interactive online classrooms, students can interact with experienced teachers anytime, anywhere, resolve difficulties, and develop personalized learning plans based on their individual needs. New Oriental’s online tutoring services not only provide real-time teaching support but also incorporate an intelligent assessment system to provide students with accurate learning feedback, helping them make significant progress in exams, academics, and skills enhancement. |

Source: Third-party data, QYResearch Research Team

3 Online Tutoring Service Industry Chain Analysis

| Industry Chain |

Description |

| Upstream |

The upstream of the online tutoring industry chain mainly includes curriculum content development institutions, intellectual property providers, teacher resource platforms, and technology infrastructure suppliers. Educational publishing institutions and curriculum development teams are responsible for developing standardized curriculum systems, question banks, and assessment tools based on national teaching syllabi. Independent teachers or contracted lecturers provide professional knowledge output through platforms, and some top teachers develop personal brands. Technology infrastructure includes cloud service providers, video live streaming engines, AI algorithm companies, and learning management system developers, providing underlying support for course transmission, interactive teaching, and intelligent Q&A. The content quality and technological stability of the upstream links directly determine the service experience and user reputation of the midstream platforms. |

| Midstream |

The midstream of the industry chain is the core delivery link of online tutoring services, including online education platform operators, course service integrators, and teaching quality management institutions. Platforms aggregate high-quality course resources and teachers through self-operated or onboarded models, providing various formats such as live classes, recorded classes, and one-on-one tutoring for different tracks such as K-12, vocational education, and adult hobbies. Platform operators are responsible for the entire process of services, including course scheduling, student matching, classroom interaction, post-class assessment, and learning data analysis, while establishing teacher selection, training, and assessment mechanisms to ensure teaching quality. The core competitiveness of the midstream segment lies in the efficiency of supply and demand matching, improved course completion rates, and user retention capabilities, achieved through technological means to realize personalized learning path planning. |

| Downstream |

The downstream of the industry chain covers individual learners and institutional clients worldwide, including primary and secondary school students, university students, working professionals, senior citizens, and corporate training departments. Individual users choose course products based on their needs for further education, certification, and skills enhancement, and their payment decisions are influenced by multiple factors such as word-of-mouth reviews, trial learning experiences, and price sensitivity. Corporate clients purchase online training courses for their employees for skills upgrading and compliance training. Furthermore, the downstream segment has spawned value-added services such as learning communities, study abroad consulting, career planning, and educational finance, forming a service ecosystem centered around lifelong learning. The continuous accumulation of user learning behavior data, in turn, empowers upstream content iteration and midstream recommendation algorithm optimization. |

Source: Third-party data, QYResearch Research Team

4 Online Tutoring Service Industry Development Trends, Opportunities, Obstacles and Industry Barriers

Development Trends:

1. Rapid Market Expansion. A Trillion-Dollar Sector is Taking Shape. The global online tutoring market is experiencing explosive growth. This expansion is primarily driven by the widespread adoption of digital learning tools and the deep penetration of artificial intelligence (AI) technology. Globally, over 74% of students are seeking flexible, technology-driven educational alternatives, and online tutoring is evolving from a supplementary form to a mainstream educational model. North America, Asia Pacific, and Europe are the three core markets, with the Asia Pacific region leading the global growth rate.

2. Deep AI Penetration. Personalized Learning Becomes Standard. Artificial intelligence is moving from concept to full-scale implementation. 68% of online tutoring platforms have integrated AI-driven adaptive learning tools, dynamically adjusting learning paths based on student levels. Leading edtech companies have invested tens of billions in R&D for AI learning systems, achieving a leap from a “one-size-fits-all” approach to a “personalized learning experience” through knowledge graph construction and intelligent learning analysis. Personalized recommendations have increased student performance and engagement by over 59%, and AI tutors, intelligent Q&A, and automatic grading are reshaping the global teaching and learning landscape.

3. Mobile and Gamification Reshaping the Learning Experience. Mobile-based tutoring apps now account for 64% of all online learning, with smartphones and tablets becoming the primary gateways for students to access educational services, especially in mobile-first emerging markets such as Southeast Asia and Latin America. Gamified learning solutions have increased student engagement by over 40%, and interactive content and real-time feedback mechanisms have significantly improved the learning experience. 59% of platforms utilize gamified elements such as progress badges and leaderboards, driving online education towards greater immersion and self-motivation.

Development Opportunities:

1. Lifelong learning demand is driving the market across all age groups. Demand for in-service education and corporate training continues to rise globally, with 58% of companies utilizing online tutoring platforms for leadership development and employee skills enhancement. The surge in adults seeking career transitions and seniors learning new skills has been fully activated, making vocational education and adult training new growth drivers. Corporate skills enhancement programs and flexible learning modules are propelling the in-service education segment to expand steadily at a CAGR of 23.1%, extending its reach from K-12 to the entire life cycle.

2. Explosive growth in education demand in emerging markets. Emerging markets such as Southeast Asia, India, Latin America, and Africa are experiencing the dual benefits of a expanding middle-income group and increased investment in education. The uneven distribution of quality educational resources and the high cost of offline tutoring in these regions provide a huge market penetration opportunity for online tutoring. Localized language support, culturally adapted content design, and low subscription prices enable online platforms to reach hundreds of millions of potential users who previously lacked access to quality educational resources, resulting in a vast market growth potential.

3. Technological inclusion is driving educational equity. Online tutoring has broken down geographical barriers, enabling students in rural and remote areas to access high-quality global educational resources. The widespread adoption of remote learning systems, smart teaching terminals, and offline learning capabilities is bridging the digital divide. International non-profit organizations are collaborating with edtech companies to provide free or low-cost learning solutions to underdeveloped regions, creating a synergy between the social and economic value of online education and fostering a virtuous cycle of educational equity and technological development.

Barriers:

1. Research and Development Barriers & Content Quality. Education is far more than just problem-solving skills. While large models can handle hundreds of millions of questions, they struggle to accurately grasp the complex test points and teaching logic within K-12 curricula worldwide. Leading education companies possess decades of accumulated research and development experience, forming a systematic content organization and verification mechanism covering the entire resource chain from curriculum outlines to question banks. This deep research capability and localized curriculum adaptation experience are core barriers that new entrants cannot easily replicate in the short term.

2. Technology, Algorithms, and Data Governance Barriers. Personalized recommendations require massive amounts of high-quality data and long-term industry know-how accumulation. The AI illusion problem has not been completely eliminated, and for students lacking discernment, correcting such misleading information is extremely costly. Simultaneously, facing increasingly stringent data security regulations and algorithm bias auditing requirements, vendors must invest heavily in ensuring the accuracy and compliance of their systems. Iterative optimization of algorithm models requires continuous feedback from real-world teaching scenarios, creating a data flywheel effect.

3. Brand Trust and Customer Acquisition Cost Barriers. Online education platforms require sustained and substantial investment to build brand trust, especially in the K-12 sector where parents make informed decisions. Leading institutions have invested billions of dollars in market education, constructing comprehensive smart education systems covering teaching, assessment, and management. For new brands, convincing users to entrust their learning data while bearing the high costs of global traffic acquisition is extremely difficult. Building a positive reputation and increasing referral rates requires a long period, and new entrants face significant trust barriers.

The report provides a detailed analysis of the market size, growth potential, and key trends for each segment. Through detailed analysis, industry players can identify profit opportunities, develop strategies for specific customer segments, and allocate resources effectively.

The Online Tutoring Service market is segmented as below:

By Company

Acadecraft

Gaotu Techedu Inc.

New Oriental

Beijing Fenbi Lantian Technology Company Ltd.

Beijing Huatu Hongyang Network Technology Co., Ltd.

Chegg, Inc

TutorEye, Inc

Varsity Tutors LLC

Think & Learn Private Limited

Vedantu Innovations Private Limited

Xueda Education Group

K12 Inc(Stride )

Unacademy

Knowbox

Ruanguru

GoStudent

ClubZ

Segment by Type

One-on-One Tutoring

Group Tutoring

Self-Study Platform Tutoring

Segment by Application

Preschool

Kindergarten

Primary School

Junior High School

High School

University

Others

Each chapter of the report provides detailed information for readers to further understand the Online Tutoring Service market:

Chapter 1: Introduces the report scope of the Online Tutoring Service report, global total market size (valve, volume and price). This chapter also provides the market dynamics, latest developments of the market, the driving factors and restrictive factors of the market, the challenges and risks faced by manufacturers in the industry, and the analysis of relevant policies in the industry. (2021-2032)

Chapter 2: Detailed analysis of Online Tutoring Service manufacturers competitive landscape, price, sales and revenue market share, latest development plan, merger, and acquisition information, etc. (2021-2026)

Chapter 3: Provides the analysis of various Online Tutoring Service market segments by Type, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different market segments. (2021-2032)

Chapter 4: Provides the analysis of various market segments by Application, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different downstream markets.(2021-2032)

Chapter 5: Sales, revenue of Online Tutoring Service in regional level. It provides a quantitative analysis of the market size and development potential of each region and introduces the market development, future development prospects, market space, and market size of each country in the world..(2021-2032)

Chapter 6: Sales, revenue of Online Tutoring Service in country level. It provides sigmate data by Type, and by Application for each country/region.(2021-2032)

Chapter 7: Provides profiles of key players, introducing the basic situation of the main companies in the market in detail, including product sales, revenue, price, gross margin, product introduction, recent development, etc. (2021-2026)

Chapter 8: Analysis of industrial chain, including the upstream and downstream of the industry.

Chapter 9: Conclusion.

Benefits of purchasing QYResearch report:

Competitive Analysis: QYResearch provides in-depth Online Tutoring Service competitive analysis, including information on key company profiles, new entrants, acquisitions, mergers, large market shear, opportunities, and challenges. These analyses provide clients with a comprehensive understanding of market conditions and competitive dynamics, enabling them to develop effective market strategies and maintain their competitive edge.

Industry Analysis: QYResearch provides Online Tutoring Service comprehensive industry data and trend analysis, including raw material analysis, market application analysis, product type analysis, market demand analysis, market supply analysis, downstream market analysis, and supply chain analysis.

and trend analysis. These analyses help clients understand the direction of industry development and make informed business decisions.

Market Size: QYResearch provides Online Tutoring Service market size analysis, including capacity, production, sales, production value, price, cost, and profit analysis. This data helps clients understand market size and development potential, and is an important reference for business development.

Other relevant reports of QYResearch:

Global Online Tutoring Service Market Outlook, In‑Depth Analysis & Forecast to 2032

Global Online Tutoring Service Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

Global Online Tutoring Service Market Research Report 2026

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 19 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp