Active Phased Array Transmit Receive Module Product Definition

Active Phased Array Transmit Receive Module is a self-contained radio frequency building block used in electronically steered antennas that performs both transmit and receive functions for an individual radiating element or a small group of elements. It integrates transmit power amplification, low-noise receive amplification, switching between transmit and receive paths, and precise phase and gain control so the antenna can steer and shape beams electronically. The module also typically includes bias and power management, digital control interfaces, calibration features, and health monitoring to support stable performance and maintainability in demanding radar, electronic warfare, and satellite communications environments.

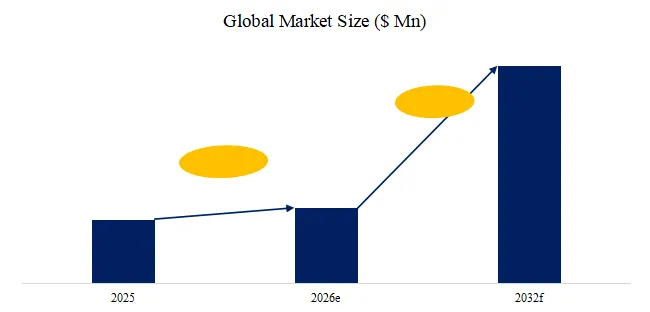

Figure00001. Global Active Phased Array Transmit Receive Module Market Size (US$ Million), 2021-2032

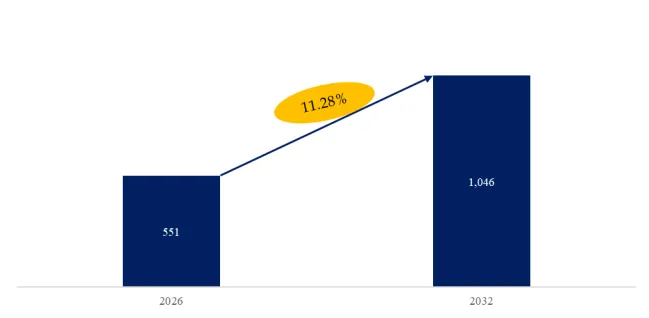

According to the new market research report “Global Active Phased Array Transmit Receive Module Market Report 2026-2032″, published by QYResearch, the global Active Phased Array Transmit Receive Module market size is reached to USD 1,812.35 million in 2025, at a CAGR of 19.36% during the forecast period.

Above data is based on report from QYResearch: Global Active Phased Array Transmit Receive Module Market Report 2026-2032 (published in 2026). If you need the latest data, plaese contact QYResearch.

Active Phased Array Transmit Receive Module Market Summary

Research Background:

Active phased array transmit receive modules are the fundamental building blocks that enable active electronically scanned array systems to electronically steer beams without mechanically moving an antenna. In modern defense and aerospace, they sit at the center of the shift from mechanically scanned radars to AESA architectures, driven by requirements for faster beam agility, multi-target tracking, greater reliability, and improved electronic counter-countermeasure performance. This transition is being reinforced by the move toward higher power and efficiency semiconductor technologies such as GaN for RF power amplification, which supports longer detection ranges and smaller, lighter array apertures for a given performance level.

Development Status:

The market is in a phase of accelerated engineering optimization and industrialization rather than basic feasibility. Across defense radar modernization and adjacent applications such as electronic warfare and satellite communications, suppliers are pushing higher levels of integration, improved thermal design, and manufacturability to reduce lifecycle cost while sustaining high channel counts and high duty-cycle operation. Technology roadmaps increasingly emphasize GaN-based RF front ends for higher power density and efficiency, alongside advanced packaging approaches such as multi-layer and 3D integration to shorten interconnects and improve RF performance in compact form factors.

Future Trends:

GaN penetration expands from premium to mainstream programs as defense-driven demand continues to prioritize power density, efficiency, and bandwidth for AESA radar and compact EW systems, pulling the ecosystem toward higher-volume, more standardized GaN RF supply chains.

Higher integration and packaging innovation become the main battleground, with more channels per module, tighter RF-to-digital co-design, and 3D or system-in-package style implementations that improve performance while reducing size, mass, and assembly complexity.

From hardware modules to software-defined array building blocks, where calibration, health monitoring, and digital beamforming cooperation are increasingly embedded into the module and tile architecture, enabling predictive maintenance and faster field upgrades for multi-mission arrays.

Supply Chain Analysis:

l Upstream

The upstream chain is anchored by RF semiconductor devices and materials, especially GaN and GaAs MMICs, plus supporting components such as phase shifters, attenuators, LNAs, power amplifiers, control ICs, high-frequency substrates, thermal interface materials, and advanced packaging and interconnect processes. Critical upstream capabilities include wafer supply, RF device design, high-reliability assembly, and thermal management engineering for sustained high-power operation.

l Downstream

Downstream, transmit receive modules are integrated into antenna panels or tiled arrays, then into full radar or communication payloads, and finally into platforms such as air and missile defense systems, airborne and naval radars, electronic warfare suites, and high-throughput satellite terminals. Value capture downstream is shaped by system-level qualification, ruggedization, calibration, and long-term sustainment, because module performance and reliability directly determine array availability and mission readiness over the equipment lifecycle.

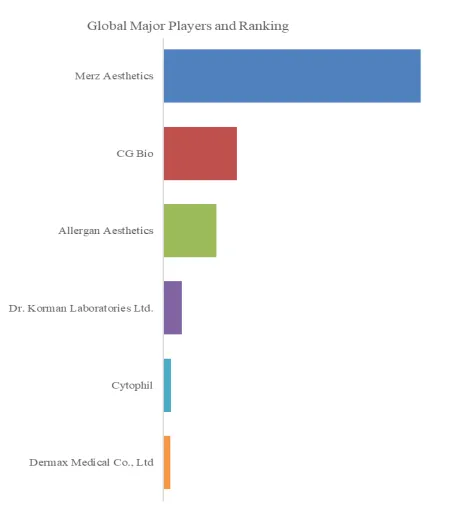

Introduction of Leading Companies in the Industry

HENSOLDT is a German defense and sensor technology company specializing in the development and manufacture of radar systems, electro-optical sensors, electronic warfare solutions, and airborne defence technologies. Its portfolio spans high-end sensing and battlefield awareness products, with a strong presence in Europe and international markets. As a key sensor supplier in military electronics, HENSOLDT has extensive expertise in phased-array radar, modular RF systems, and advanced signal processing.

HENSOLDT Active Phased Array Transmit Receive Module Product Introduction:

HENSOLDT has developed standardized modular Active Phased Array Transmit/Receive Modules for modern phased-array radar and synthetic aperture systems. These modules provide high transmit power amplification, low-noise signal reception, precise phase and gain control, decoupled transmit/receive paths, and a compact design suitable for fully array-compatible integration. They incorporate radiation-tested components and demonstrate robustness under demanding environmental conditions, making them fundamental building blocks for high-density active antenna arrays.

Technically, HENSOLDT’s T/R modules support high power output and precise signal control to enable rapid electronic beam steering and multi-target tracking in phased-array systems. In its airborne radar products such as the PrecISR family, the company uses advanced GaN-based T/R functions and modular array design to double transmit power while maintaining compact, efficient systems. These features make HENSOLDT’s transmit/receive modules competitive for military radar, earth observation, and surveillance applications.

About QYResearch

QYResearch founded in California, USA in 2007.It is a leading global market research and consulting company. With over 17 years’ experience and professional research team in various cities over the world QY Research focuses on management consulting, database and seminar services, IPO consulting (data is widely cited in prospectuses, annual reports and presentations), industry chain research and customized research to help our clients in providing non-linear revenue model and make them successful. We are globally recognized for our expansive portfolio of services, good corporate citizenship, and our strong commitment to sustainability. Up to now, we have cooperated with more than 60,000 clients across five continents. Let’s work closely with you and build a bold and better future.

QYResearch is a world-renowned large-scale consulting company. The industry covers various high-tech industry chain market segments, spanning the semiconductor industry chain (semiconductor equipment and parts, semiconductor materials, ICs, Foundry, packaging and testing, discrete devices, sensors, optoelectronic devices), photovoltaic industry chain (equipment, cells, modules, auxiliary material brackets, inverters, power station terminals), new energy automobile industry chain (batteries and materials, auto parts, batteries, motors, electronic control, automotive semiconductors, etc.), communication industry chain (communication system equipment, terminal equipment, electronic components, RF front-end, optical modules, 4G/5G/6G, broadband, IoT, digital economy, AI), advanced materials industry Chain (metal materials, polymer materials, ceramic materials, nano materials, etc.), machinery manufacturing industry chain (CNC machine tools, construction machinery, electrical machinery, 3C automation, industrial robots, lasers, industrial control, drones), food, beverages and pharmaceuticals, medical equipment, agriculture, etc.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp