Signaling Devices Market Summary

Signaling devices are essential tools used to alert or inform people about specific conditions, hazards, or events in various environments. They can be visual, audible, or a combination of both, depending on the requirements of the situation. Visual signaling devices, such as flashing lights, beacons, are used to capture attention through sight, especially in environments with high noise levels or when auditory signals may not be effective. Audible signaling devices, like horns or sirens, are employed to emit sound in order to warn individuals about an event or emergency, making them critical in places with low visibility or high ambient noise.

In many industrial and safety-critical sectors, signaling devices play a crucial role in enhancing safety and communication. They are commonly used in manufacturing plants, warehouses, and factories, where they alert workers to machine malfunctions, safety breaches, or operational changes. Additionally, signaling devices are a vital part of emergency alarm systems, providing warnings of fires, gas leaks, or other hazardous situations. In environments where there is a risk of explosion, such as chemical plants or oil refineries, these devices are designed to meet strict safety standards to prevent any spark or heat generation that could lead to an explosion.

Signaling devices are also built to withstand harsh environmental conditions, such as extreme temperatures, moisture, dust, or corrosive substances. Some are specifically designed for use in explosive atmospheres and are constructed to meet safety standards like ATEX or IECEx, ensuring that they do not pose a risk in volatile environments. Whether used in industrial, emergency, or transport settings, signaling devices are indispensable in preventing accidents and maintaining a safe working environment.

Market Overview

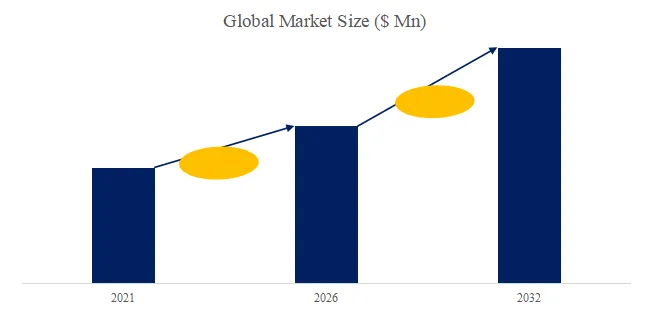

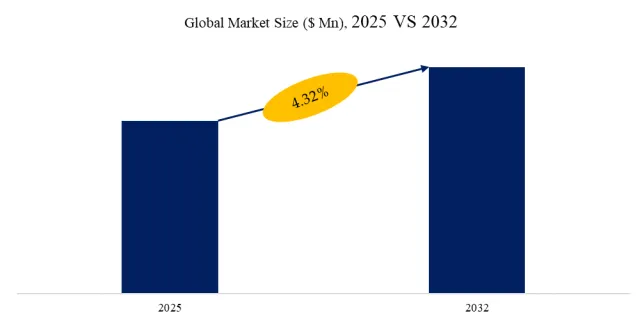

The global market for Signaling Devices was valued at US$ 0.84 billion in 2025 and is projected to reach US$ 1.09 billion, growing at a CAGR of 4.32% from 2026 to 2032.

The global signaling devices market is being primarily driven by stringent safety regulations and industrial compliance requirements across sectors such as manufacturing, oil & gas, energy, and transportation. Increasing awareness of workplace safety and the need to meet international safety standards are accelerating the adoption of advanced signaling devices, including combined audio-visual alarms, and smart IoT-enabled systems.

Rapid industrialization and infrastructure development, particularly in emerging economies, are further supporting market growth. Expansion in sectors such as manufacturing, energy, and logistics is creating higher demand for signaling devices that can enhance operational efficiency, provide real-time alerts, and support automation initiatives, making them essential components of modern industrial environments.

Technological innovation is another key driver. Signaling devices are increasingly incorporating wireless connectivity, predictive maintenance capabilities, energy-efficient designs, and modular configurations. These advances enable easier installation, real-time monitoring, and integration with industrial control systems, gradually replacing traditional mechanical and incandescent solutions.

Regionally, North America, Europe and Asia-Pacific maintain a significant share of the market, largely due to strict regulatory compliance and widespread industrial adoption. At the same time, the Asia-Pacific region is emerging as the fastest-growing market, fueled by rapid industrialization, urban development, and substantial investments in smart infrastructure and industrial automation technologies.

Despite these opportunities, the market faces challenges such as high integration costs, maintenance requirements, and adoption barriers in smaller enterprises. Nevertheless, ongoing technological advancements, increasing global industrialization, and the focus on intelligent safety solutions are expected to sustain long-term growth, positioning signaling devices as essential components of modern industrial and commercial environments.

Table 1. Signaling Devices Market Trends

| Key Trends | Description |

| Integration with IoT and Smart Technologies | The integration of signaling devices with Internet of Things (IoT) and smart technologies is one of the most significant trends in the industry. By connecting signaling devices to networked systems, companies can monitor and control these devices remotely, enabling predictive maintenance and real-time alerts. This integration allows for more efficient operations, reduces downtime, and improves safety by providing instant notifications of potential issues. In industries like manufacturing and logistics, where continuous monitoring is critical, IoT-enabled signaling devices are becoming a standard feature, allowing for better decision-making and automation of alert systems. |

| Enhanced Customization and Flexibility | As industries become more specialized, there is an increasing demand for signaling devices that can be customized to specific needs. Manufacturers are responding by offering devices that can be tailored in terms of color, sound type, and functionality, allowing businesses to create signaling systems that suit their particular operations. Whether it’s adjusting the tone of an audible signal or changing the light’s flashing pattern, customizable signaling devices offer businesses more control over their alert systems. This trend is especially important in complex industrial environments, where different warning signals are needed for different types of events or hazards. |

| Focus on Energy Efficiency and Sustainability | Energy efficiency and sustainability are becoming increasingly important in the signaling devices industry. Manufacturers are developing products that consume less energy while still providing the same level of performance. This is especially relevant for devices that need to operate continuously, such as emergency alarm systems or outdoor warning systems. Low-power options, like LED-based visual signals, are gaining popularity because they not only reduce energy consumption but also have a longer lifespan compared to traditional incandescent bulbs. In addition, more companies are prioritizing eco-friendly materials and recycling practices, aligning with global sustainability goals and regulations. |

| Wireless Signaling Systems | Wireless signaling systems are gaining traction as companies look for ways to reduce installation time, lower costs, and increase flexibility. Traditional wired signaling systems can be complex and costly to install, especially in large facilities or outdoor environments. Wireless solutions eliminate the need for complex wiring, allowing for quicker setup and more scalable systems. These devices can be easily relocated, making them ideal for temporary setups or changing operational conditions. Additionally, wireless signaling devices can be integrated into broader building management or safety systems, enhancing the overall communication infrastructure. |

| Adoption of Explosion-Proof and Hazardous Area Signaling Devices | In industries where explosive atmospheres are a risk, such as oil and gas, chemical plants, and mining, the demand for explosion-proof signaling devices is increasing. These devices are specially designed to operate safely in hazardous environments where the presence of flammable gases or dust could lead to an explosion. The trend towards stricter safety regulations and standards, such as ATEX (European Union) and IECEx (International), is driving the development of more advanced explosion-proof signaling devices. These devices must meet rigorous certifications to ensure they do not pose any risk in dangerous environments, making them essential for industries that prioritize safety and compliance. |

| Real-Time Data and Analytics Integration | With the growing emphasis on data-driven decision-making, the integration of real-time data and analytics into signaling systems is becoming more common. By collecting and analyzing data from signaling devices, companies can gain valuable insights into system performance, maintenance needs, and operational efficiency. This trend is particularly important in industries like manufacturing, where downtime can be costly. By using analytics, companies can identify patterns in system failures or predict potential issues before they escalate. Real-time monitoring also helps improve response times to safety alerts, ensuring a faster and more effective reaction to emergencies. |

| Multi-Functional Signaling Devices | As industries strive for more cost-effective solutions, the trend of multi-functional signaling devices is on the rise. These devices combine multiple features, such as visual and audible alerts, with additional functionalities like message displays or integrated communication systems. Multi-functional devices help streamline safety systems by reducing the number of separate components needed in a facility. For example, a single unit might combine a flashing light, a siren, and a voice announcement, providing a comprehensive alert system in one device. This trend is especially valuable in large-scale operations where space and resources are limited, offering a more efficient and compact solution. |

| Advanced Safety and Compliance Features | As safety regulations continue to tighten across industries, signaling devices are being equipped with more advanced features to ensure compliance. Devices are being developed with enhanced fail-safe mechanisms, redundancy features, and self-testing capabilities to ensure reliability in emergency situations. These features not only improve safety but also help businesses meet increasingly stringent regulatory requirements. For instance, devices that include self-diagnostic functions or systems that automatically notify maintenance teams when a fault occurs are becoming more common, reducing the risk of system failures during critical situations. |

Source: Secondary Sources, Expert Interviews and QYResearch, 2026

Figure00001. Global Signaling Devices Market Size (US$ Million), 2025 vs 2032

Above data is based on report from QYResearch: Global Signaling Devices Market Report 2026-2032 (published in 2026). If you need the latest data, plaese contact QYResearch.

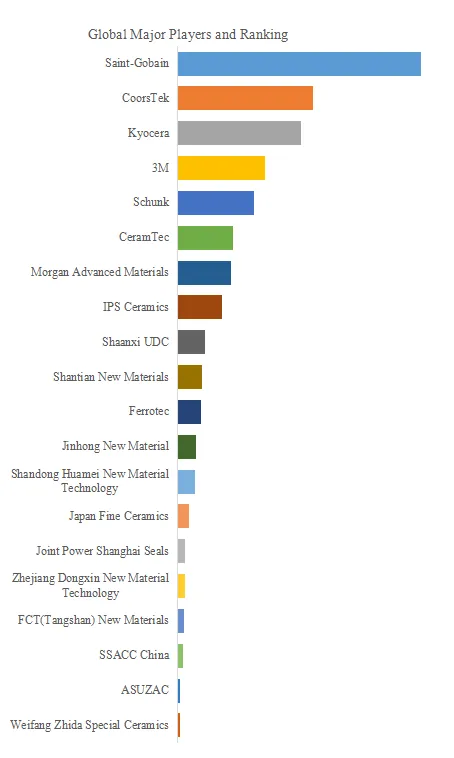

Figure00002. Global Signaling Devices Top 26 Players Ranking and Market Share (Ranking is based on the revenue of 2025, continually updated)

Above data is based on report from QYResearch: Global Signaling Devices Market Report 2026-2032 (published in 2026). If you need the latest data, plaese contact QYResearch.

According to QYResearch Top Players Research Center, the global key manufacturers of Signaling Devices include Patlite, Federal Signal, Werma Signaltechnik, E2S Warning Signals, Eaton, Rockwell Automation, Honeywell, Auer Signal, Qlight, Pfannenberg, etc. In 2025, the global top 10 players had a share approximately 59.0% in terms of revenue.

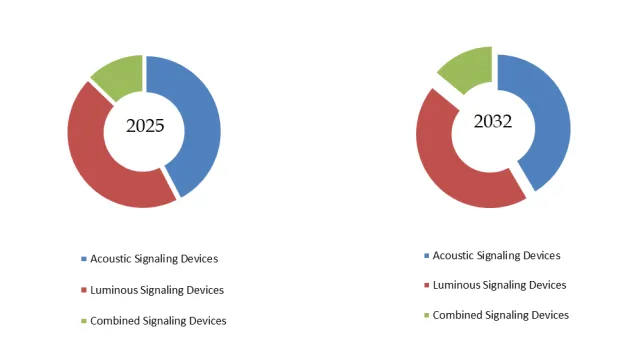

Figure00003. Signaling Devices, Global Market Size, Split by Product Segment

Based on or includes research from QYResearch: Global Signaling Devices Market Report 2026-2032.

In terms of product type, currently Luminous Signaling Device is the largest segment, hold a share of 44.84%.

About QYResearch

QYResearch founded in California, USA in 2007.It is a leading global market research and consulting company. With over 17 years’ experience and professional research team in various cities over the world QY Research focuses on management consulting, database and seminar services, IPO consulting (data is widely cited in prospectuses, annual reports and presentations), industry chain research and customized research to help our clients in providing non-linear revenue model and make them successful. We are globally recognized for our expansive portfolio of services, good corporate citizenship, and our strong commitment to sustainability. Up to now, we have cooperated with more than 60,000 clients across five continents. Let’s work closely with you and build a bold and better future.

QYResearch is a world-renowned large-scale consulting company. The industry covers various high-tech industry chain market segments, spanning the semiconductor industry chain (semiconductor equipment and parts, semiconductor materials, ICs, Foundry, packaging and testing, discrete devices, sensors, optoelectronic devices), photovoltaic industry chain (equipment, cells, modules, auxiliary material brackets, inverters, power station terminals), new energy automobile industry chain (batteries and materials, auto parts, batteries, motors, electronic control, automotive semiconductors, etc.), communication industry chain (communication system equipment, terminal equipment, electronic components, RF front-end, optical modules, 4G/5G/6G, broadband, IoT, digital economy, AI), advanced materials industry Chain (metal materials, polymer materials, ceramic materials, nano materials, etc.), machinery manufacturing industry chain (CNC machine tools, construction machinery, electrical machinery, 3C automation, industrial robots, lasers, industrial control, drones), food, beverages and pharmaceuticals, medical equipment, agriculture, etc.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp