Floor Edgers Market Summary

A floor edger is a specialized power tool used in floor sanding and finishing, designed to sand, smooth, or refinish the edges and corners of a floor that a larger drum sander cannot reach.

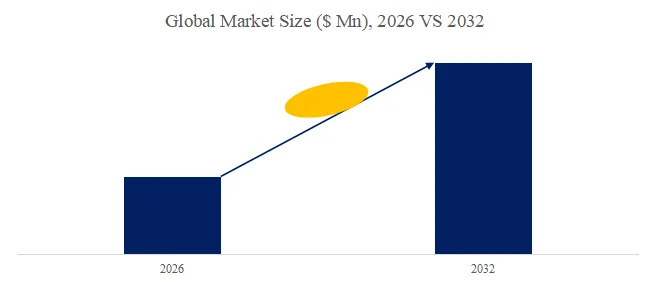

According to the new market research report “Global Floor Edgers Market Report 2026-2032”, published by QYResearch, the global Floor Edgers market size is projected to reach USD 0.64 billion by 2032, at a CAGR of 3.1% during the forecast period.

Figure00001. Global Floor Edgers Market Size (US$ Million), 2026 VS 2032

Above data is based on report from QYResearch: Global Floor Edgers Market Report 2026-2032 (published in 2025). If you need the latest data, plaese contact QYResearch.

Market Drivers:

The floor edgers market is primarily driven by the increasing demand for efficient and high-quality floor maintenance solutions across residential, commercial, and industrial sectors. Rapid urbanization and the expansion of commercial infrastructure, including offices, hotels, hospitals, and airports, are boosting the need for professional cleaning equipment that can maintain polished, safe, and aesthetically appealing flooring. Growing awareness of hygiene, cleanliness, and workplace safety standards, particularly in healthcare, hospitality, and public facilities, is further fueling adoption of advanced floor maintenance tools. Additionally, the trend toward automated and semi-automated cleaning solutions, combined with technological advancements such as ergonomic designs, improved battery life, and low-noise operation, is enhancing operational efficiency and user convenience. Rising investments in facility management services and the increasing availability of rental and leasing models for cleaning equipment also expand accessibility for small and medium enterprises, further supporting market growth. Overall, the convergence of infrastructure development, hygiene awareness, technological innovation, and service-oriented solutions is driving robust demand in the floor edgers market.

Restraint:

The floor edgers market faces several restraints that could limit its growth despite rising demand for efficient floor maintenance solutions. One of the primary challenges is the high initial cost of advanced or automated floor edgers, which can deter small businesses or budget-conscious consumers from adopting these products. Operational challenges, such as the need for trained personnel to safely and effectively use the equipment, also limit widespread adoption, particularly in regions with low technical skills availability. Maintenance and replacement costs for brushes, pads, batteries, and other components further increase the total cost of ownership, reducing appeal among cost-sensitive users. Additionally, the presence of alternative cleaning methods, such as traditional manual mopping, basic polishers, or robotic cleaners, creates competition that can slow market penetration. Environmental factors, such as uneven or delicate flooring surfaces, may also restrict the use of certain floor edgers, requiring specialized equipment for different floor types. Collectively, these factors—high upfront investment, operational complexity, maintenance costs, and alternative solutions—act as key restraints on the floor edgers market.

Opportunity:

The floor edgers market presents significant opportunities driven by the growing emphasis on hygiene, cleanliness, and facility maintenance across residential, commercial, and industrial sectors. The rapid expansion of commercial infrastructure, including offices, hotels, airports, hospitals, and retail spaces, is increasing demand for professional-grade floor maintenance equipment capable of delivering polished, safe, and aesthetically appealing flooring. Technological advancements, such as battery-powered, low-noise, ergonomic, and semi-automated or fully automated floor edgers, are enhancing operational efficiency and user convenience, creating opportunities for premium product offerings. Additionally, the rise of facility management and outsourcing services, coupled with flexible rental and leasing models, allows smaller businesses and institutions to access high-quality floor maintenance equipment without heavy upfront investment. Emerging markets in Asia, Africa, and Latin America, where urbanization and commercial development are accelerating, provide further growth potential for new installations and equipment upgrades. Moreover, increasing awareness of sustainable and eco-friendly cleaning solutions presents opportunities for innovation in energy-efficient, low-water, and low-emission floor edger designs. Overall, infrastructure growth, technological innovation, service-oriented business models, and sustainability trends collectively create a strong opportunity landscape for the floor edgers market.

Industry Chain

The floor edgers industry chain encompasses a comprehensive ecosystem of raw material suppliers, component manufacturers, equipment assemblers, distributors, and end-users. At the upstream level, the industry relies on suppliers of metals, plastics, electronic components, motors, batteries, brushes, pads, and other consumables required for manufacturing durable and efficient floor edgers. The midstream segment consists of floor edger manufacturers who integrate these materials and components into a variety of products, ranging from manual and semi-automated edgers to advanced battery-powered and fully automated models. This stage often involves precision assembly, quality testing, and incorporation of ergonomic and technological features, such as noise reduction, digital controls, and energy-efficient motors. Downstream, distributors, retailers, and facility management companies deliver the equipment to commercial, industrial, and residential end-users, including hotels, hospitals, airports, offices, and educational institutions. After-sales support, maintenance services, and consumables like replacement pads and brushes form an integral part of the value chain, ensuring recurring revenue and sustained customer engagement. The growth of the industry is further reinforced by rental and leasing models, which provide access to advanced equipment for small and medium-sized enterprises without significant upfront investment. Overall, the floor edgers industry chain is characterized by close collaboration between raw material suppliers, manufacturers, and service providers to meet the evolving demand for efficient, reliable, and technologically advanced floor maintenance solutions.

Barriers to Entry

The floor edgers market presents several barriers to entry that can challenge new entrants and limit competition. One of the primary obstacles is the high initial capital investment required for designing, manufacturing, and testing durable and technologically advanced floor edgers, including automated or battery-powered models. Developing reliable and efficient products also requires expertise in motor systems, electronics, ergonomics, and material durability, which creates a significant technical barrier for newcomers without engineering experience. Brand recognition and customer trust are critical in the commercial and industrial segments, as facility managers and institutions prefer established manufacturers with proven product reliability and after-sales service, making market penetration difficult for new entrants. Additionally, establishing a distribution network, offering maintenance services, and providing consumables like brushes, pads, and replacement parts require logistical capabilities and long-term partnerships, further raising entry barriers. Compliance with safety, quality, and environmental standards in different regions adds regulatory complexity, increasing both time and cost to enter new markets. Collectively, high capital requirements, technical expertise, brand credibility, service infrastructure, and regulatory compliance constitute significant barriers for new players attempting to enter the floor edgers market.

About QYResearch

QYResearch founded in California, USA in 2007.It is a leading global market research and consulting company. With over 17 years’ experience and professional research team in various cities over the world QY Research focuses on management consulting, database and seminar services, IPO consulting, industry chain research and customized research to help our clients in providing non-linear revenue model and make them successful. We are globally recognized for our expansive portfolio of services, good corporate citizenship, and our strong commitment to sustainability. Up to now, we have cooperated with more than 60,000 clients across five continents. Let’s work closely with you and build a bold and better future.

QYResearch is a world-renowned large-scale consulting company. The industry covers various high-tech industry chain market segments, spanning the semiconductor industry chain (semiconductor equipment and parts, semiconductor materials, ICs, Foundry, packaging and testing, discrete devices, sensors, optoelectronic devices), photovoltaic industry chain (equipment, cells, modules, auxiliary material brackets, inverters, power station terminals), new energy automobile industry chain (batteries and materials, auto parts, batteries, motors, electronic control, automotive semiconductors, etc.), communication industry chain (communication system equipment, terminal equipment, electronic components, RF front-end, optical modules, 4G/5G/6G, broadband, IoT, digital economy, AI), advanced materials industry Chain (metal materials, polymer materials, ceramic materials, nano materials, etc.), machinery manufacturing industry chain (CNC machine tools, construction machinery, electrical machinery, 3C automation, industrial robots, lasers, industrial control, drones), food, beverages and pharmaceuticals, medical equipment, agriculture, etc.

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 18 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp