Introduction: Addressing Installation Flexibility, Confined Space Wiring, and Dynamic Application Pain Points

For electrical contractors, industrial automation engineers, and facility managers, low voltage power distribution (up to 1kV) presents a persistent installation challenge. Traditional solid-conductor cables are stiff, difficult to bend (minimum bending radius 8–12× cable diameter), and prone to damage when routed through conduit bends, cable trays, or machinery cable chains. In confined spaces (building risers, industrial control panels, robotic arms), solid cables require extra clearance, longer pull lengths, and multiple junction boxes—increasing installation time 30–50% and labor costs $500–2,000 per project. For dynamic applications (robotic arms, cable carriers, moving machinery), solid conductors fail within weeks (work hardening, strand breakage), causing unplanned downtime ($5,000–50,000 per hour in automotive plants). The result: contractors over-specify cable size to reduce voltage drop, or accept premature failure, warranty claims, and safety risks. Global Leading Market Research Publisher QYResearch announces the release of its latest report “Low Voltage Flexible Power Cable – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032″. Based on current situation and impact historical analysis (2021-2025) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Low Voltage Flexible Power Cable market, including market size, share, demand, industry development status, and forecasts for the next few years.

For electrical distributors, cable manufacturers, and industrial end-users, the core pain points include reducing installation labor (flexible cables bend easily, pull through conduit with less force), ensuring reliability in dynamic applications (robotic arms, cable carriers, wind turbine pitch control), and balancing cost with performance (stranded copper vs. solid, PVC vs. XLPE insulation). Low voltage flexible power cables address these challenges as electrical cables designed to transmit power at low voltage levels (typically up to 1 kV) while offering high flexibility for easy installation in confined spaces or dynamic applications—featuring stranded copper or aluminum conductors, PVC, rubber, or thermoplastic insulation, and protective sheaths for durability and safety. As industrial automation expands (robotics, conveyor systems, packaging machinery), building construction recovers (commercial, residential, infrastructure), and renewable energy installations grow (solar, wind, battery storage), the flexible power cable market is experiencing steady growth, with multi-core flexible cables gaining share in space-constrained applications.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/6096876/low-voltage-flexible-power-cable

Market Sizing and Recent Trajectory (Q1–Q2 2026 Update)

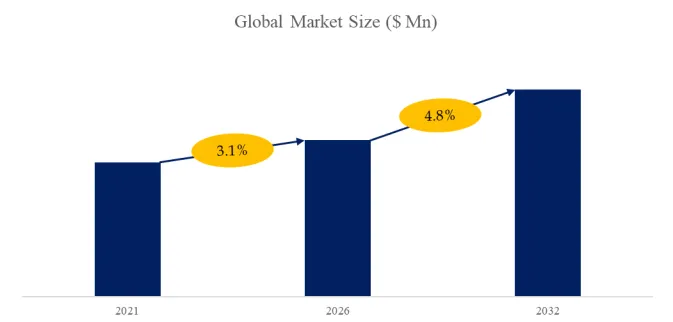

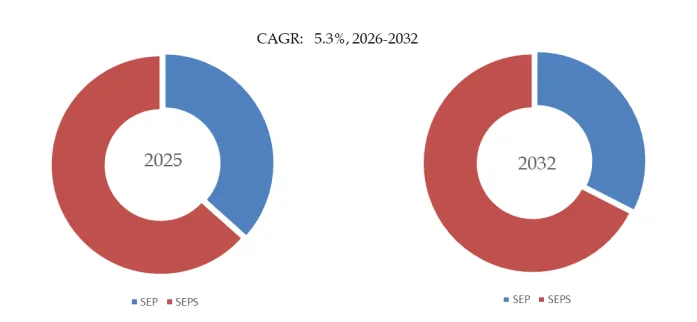

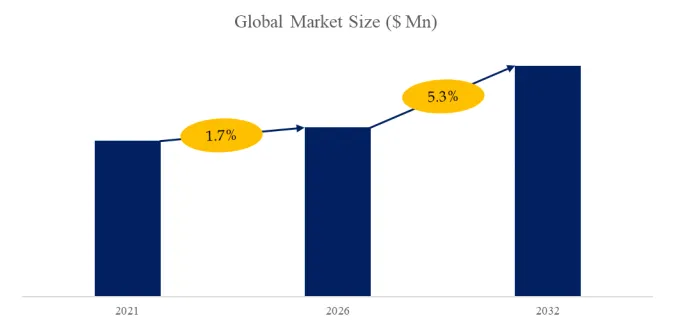

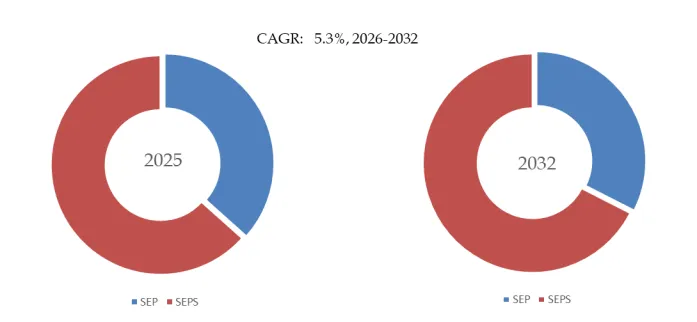

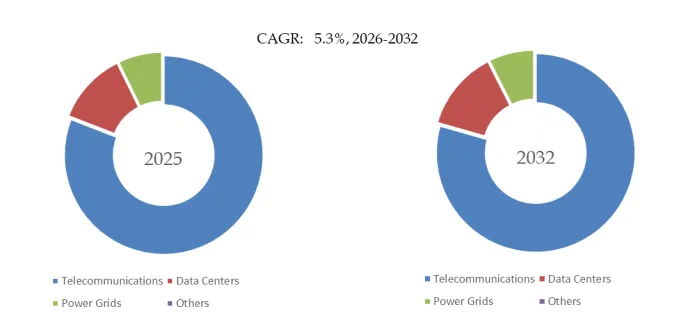

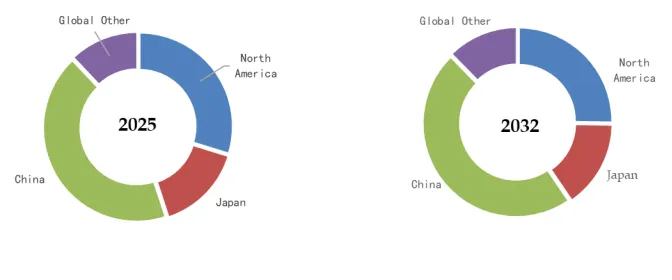

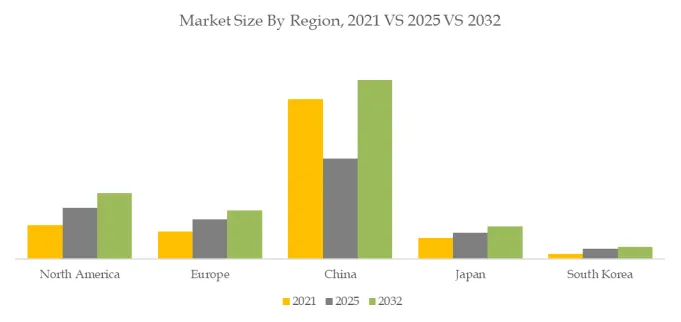

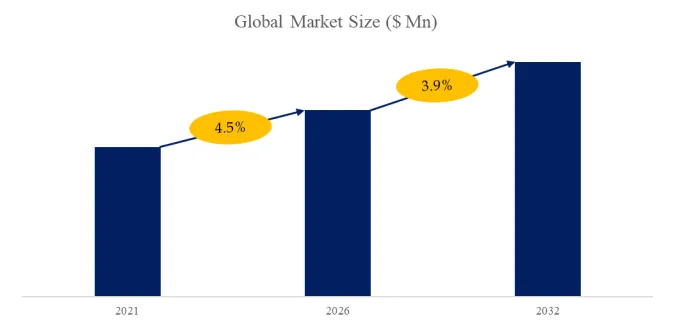

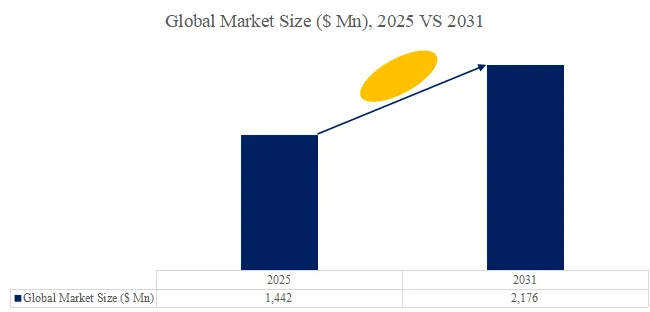

The global market for Low Voltage Flexible Power Cable was estimated to be worth US$ 5,301 million in 2025 and is projected to reach US$ 8,004 million, growing at a CAGR of 6.2% from 2026 to 2032. In 2024, global production reached approximately 493,310 km, with an average global market price of around US$ 10.65 per meter. Preliminary data for the first half of 2026 indicates accelerating demand in building construction (commercial office, residential multifamily, infrastructure) and industrial automation (robotics, conveyor systems, packaging machinery). The multi-core segment (cables with 2–50+ conductors) dominates (55% of revenue, fastest-growing at CAGR 7.2%) for control wiring, power+signal combinations, and space-constrained installations. The single-core segment (35% of revenue, CAGR 5.5%) serves simple power distribution (machinery leads, panel wiring). The others segment (10% of revenue, CAGR 4.8%) includes specialized flexible cables (welding, marine, mining). The building application segment leads (45% of revenue), followed by industrial automation (30%, fastest-growing at CAGR 7.8%), energy (15%), and others (10%).

Product Mechanism: Stranded Conductors, PVC vs. XLPE Insulation, and Flexibility Ratings

A Low Voltage Flexible Power Cable is an electrical cable designed to transmit electrical power at low voltage levels (typically up to 1 kV) while offering high flexibility for easy installation in confined spaces or dynamic applications. These cables usually feature stranded copper or aluminum conductors, PVC, rubber, or thermoplastic insulation, and protective sheaths to ensure durability and safety.

A critical technical differentiator is conductor stranding, insulation material, and bending radius:

- Single-Core Flexible Cable – One insulated conductor (stranded copper). Advantages: simple, lower cost ($8–15/meter for 6mm²), easier termination. Disadvantages: requires separate cables for multi-phase circuits (more space, higher labor). Applications: motor leads, panel wiring, battery cables. Market share: 35% of revenue (CAGR 5.5%).

- Multi-Core Flexible Cable – Multiple insulated conductors (2–50+ cores) within one sheath. Advantages: space-saving (one cable vs. multiple singles), easier routing, color-coded cores (identification). Disadvantages: higher cost ($15–30/meter for 5-core 6mm²), larger minimum bending radius than equivalent single-core. Applications: industrial control cabinets, building distribution, robotics. Market share: 55% of revenue (fastest-growing, CAGR 7.2%).

- Conductor Stranding – Solid conductor: 1 strand, stiff, breaks under repeated bending. Stranded conductor: multiple fine wires twisted (Class 5 or 6 stranding, 50–200+ strands). Flexibility increases with strand count (Class 6 > Class 5 > Class 2). Fine stranding (0.1–0.3mm diameter wires) for robotic/dynamic applications.

- Insulation Materials – PVC (polyvinyl chloride): cost-effective ($0.50–2/meter), good flexibility, -40°C to +70°C, flame-retardant. XLPE (cross-linked polyethylene): higher temperature rating (+90°C continuous, +250°C short circuit), better current rating, higher cost (+20–30%). Rubber (EPR, neoprene): extreme flexibility, oil/chemical resistance, higher cost. Thermoplastic elastomer (TPE): high flexibility, low temperature (-50°C), UV resistance.

- Minimum Bending Radius – Solid conductor: 8–12× cable diameter (e.g., 10mm cable requires 80–120mm bend). Stranded (Class 2): 6–8× diameter. Fine stranded (Class 5/6): 4–6× diameter. Ultra-flexible (drum winding): 3–4× diameter.

Recent technical benchmark (March 2026): Prysmian’s FlexiCore multi-core cable (5×6mm², Class 6 stranding, PVC insulation, $18/meter) achieved 4× cable diameter bending radius (50mm for 12.5mm cable), 10 million flex cycles (robotic cable carrier test), and -40°C to +80°C rating. Independent testing (UL 62) confirmed 90°C wet/dry rating.

Real-World Case Studies: Industrial Robotics, Building Construction, and Wind Energy

The Low Voltage Flexible Power Cable market is segmented as below by cable type and application:

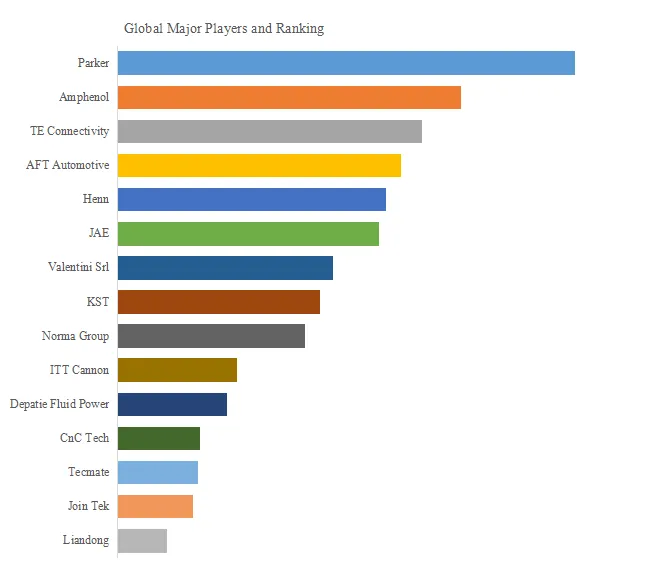

Key Players (Selected):

Prysmian Group, Nexans, Southwire, General Cable, LS Cable & System, NKT Cables, KEI Industries, Polycab, Finolex Cables, Havells, Riyadh Cables Group, Elsewedy Electric, Sumitomo Electric, Furukawa Electric, Belden, Leoni, TPC Wire & Cable, RR Kabel, Ducab

Segment by Type:

- Single-core – Simple power distribution. 35% of revenue (CAGR 5.5%).

- Multi-core – Control + power, space-saving. 55% of revenue (CAGR 7.2%).

- Others – Welding, marine, mining. 10% of revenue (CAGR 4.8%).

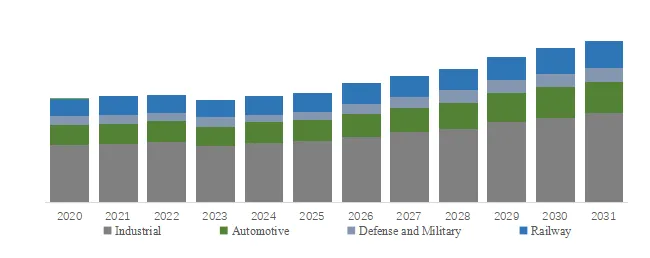

Segment by Application:

- Building – Commercial, residential, infrastructure. 45% of revenue.

- Industrial Automation – Robotics, conveyors, packaging. 30% of revenue (CAGR 7.8%).

- Energy – Solar, wind, battery storage. 15% of revenue.

- Others – Marine, mining, transportation. 10% of revenue.

Case Study 1 (Industrial Automation – Robotic Assembly Line): Automotive assembly plant (50 robotic cells) uses multi-core flexible cables (Leoni, 5×4mm², Class 6 stranding, TPE insulation, $22/meter) for power+control (robotic arm, gripper, sensors). Requirements: 10 million+ flex cycles (cable carrier), oil/coolant resistance, small bending radius (50mm). Solid or Class 2 cables fail within 6 months. Flexible cable: 5-year life. Plant consumes 50km of flexible cable annually ($1.1M). Industrial automation segment (30% of revenue) fastest-growing (CAGR 7.8%).

Case Study 2 (Building – Commercial Office Tower): 50-story commercial office tower (Chicago) uses multi-core flexible cables (Southwire, 12-core 2.5mm², PVC, $10/meter) for lighting control and power distribution. Requirements: flexible for conduit bending (multiple bends per run), color-coded cores (reduce termination errors), and UL 94 V-0 flame rating. Building consumes 200km of flexible cable ($2M). Building segment (45% of revenue) stable at 5% CAGR.

Case Study 3 (Energy – Wind Turbine Pitch Control): Vestas V150 wind turbine (4.2MW) uses single-core flexible cables (NKT, 50mm², Class 6 stranding, rubber insulation, $25/meter) for pitch control (blade angle adjustment). Requirements: extreme flexibility (rotating hub, ±180° rotation), -40°C to +90°C operation (offshore, onshore), and 20-year life. Cable undergoes 10⁸ flex cycles over turbine life. Each turbine uses 500 meters of flexible cable ($12,500). Wind segment (subset of energy, 15% of revenue) growing 8% CAGR.

Case Study 4 (Industrial Automation – Conveyor System, Food Processing): Food processing plant (sanitary environment) uses multi-core flexible cables (Belden, 7×1.5mm², TPE insulation, $15/meter) for conveyor motor power + encoder feedback. Requirements: washdown resistance (IP69K, high-pressure hot water), oil/grease resistance, and small bending radius (conveyor tight spaces). Plant uses 10km of flexible cable ($150,000). Industrial automation segment drives flexible cable demand.

Industry Segmentation: Multi-Core vs. Single-Core and Application Perspectives

From an operational standpoint, multi-core flexible cables (55% of revenue, fastest-growing) dominate industrial automation (robotics, conveyors) and building (lighting control, power distribution) where space-saving and ease of routing outweigh cost premium. Single-core flexible cables (35% of revenue) dominate motor leads, panel wiring, and battery cables (simple point-to-point power). Industrial automation (30% of revenue, fastest-growing at 7.8% CAGR) driven by robotics expansion (500,000+ industrial robots installed annually) and conveyor system upgrades. Building (45% of revenue) driven by commercial construction recovery (office, retail, hospitality) and residential multifamily.

Technical Challenges and Recent Policy Developments

Despite strong growth, the industry faces four key technical hurdles:

- Strand corrosion in fine-strand cables: Fine strands (0.1–0.3mm) have higher surface area, more susceptible to corrosion (especially in marine/offshore). Solution: tinned copper strands (Sn coating) +20–30% cost premium.

- Termination difficulty for fine-strand cables: Fine strands (Class 6) can break under screw terminals, require ferrule crimping (additional labor, cost). Solution: pre-insulated ferrules (add $0.50–2 per termination) or spring-clamp terminals.

- Voltage drop in long flexible cable runs: Stranded conductors have slightly higher resistance than solid (due to inter-strand gaps). For long runs (>100m), may require larger gauge. Solution: specify stranded conductor with same cross-section as solid (resistance difference <2%).

- Fire safety regulations for PVC cables: PVC emits dense smoke, HCl gas when burning. Low smoke zero halogen (LSZH) compounds required in public buildings (airports, stations, hospitals). LSZH cables cost 30–50% more than PVC. Policy update (March 2026): EU Construction Products Regulation (CPR) updated fire safety classes for cables (B2ca, Cca, Dca), driving LSZH adoption in commercial buildings.

独家观察: Multi-Core Flexible Cables Gaining Share in Industrial Automation

An original observation from this analysis is multi-core flexible cables gaining share over single-core in industrial automation due to space constraints (control cabinets, cable carriers, robotic arms). Multi-core cables (power + control + signal + data in one jacket) reduce cable count from 5–10 singles to 1–2 multi-cores. Installation time reduced 40–60%, panel space reduced 50–70%. In automotive plants, multi-core adoption grew from 30% of flexible cable (2015) to 60% (2025). Multi-core premium (+20–30% vs. equivalent singles) offset by labor savings.

Additionally, ultra-flexible cables (Class 6 stranding) for robotic applications fastest-growing subsegment (CAGR 10%). Robotic arms require cables with 10–20 million flex cycles (vs. 1–2 million for standard flexible). Ultra-flexible cables use extra-fine stranding (0.05–0.1mm), special lay lengths, and low-friction jackets (TPE, PUR). Ultra-flexible cost 2–3× standard flexible ($30–50/meter vs. $10–20/meter) but essential for high-speed robots (pick-and-place, assembly). Looking toward 2032, the market will likely bifurcate into standard flexible cables (Class 5 stranding, PVC insulation) for building, general industrial, and energy applications (cost-driven, 4–6% annual growth) and high-flex/ultra-flexible cables (Class 6 stranding, TPE/PUR jackets) for robotics, cable carriers, and dynamic applications (performance-driven, 8–10% annual growth), with multi-core configurations dominating both segments.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp