Global Leading Market Research Publisher QYResearch announces the release of its latest report *”Transcritical CO2 Cycle Refrigeration System – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032″*.

For facility managers, automotive HVAC engineers, and supermarket refrigeration directors, regulatory pressure to phase out hydrofluorocarbon (HFC) refrigerants has created an urgent operational challenge. Legacy R404A, R134a, and R507 systems face rising costs due to dwindling production quotas under the Kigali Amendment to the Montreal Protocol. The proven solution is the transcritical CO2 cycle refrigeration system—a natural refrigerant technology operating at high pressures (up to 140 bar) to deliver efficient cooling, heating, and refrigeration with a global warming potential (GWP) of 1. This report provides strategic intelligence on market size, component segmentation, and growth drivers to inform capital investment and regulatory compliance roadmaps.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/5764832/transcritical-co2-cycle-refrigeration-system

Market Size & Growth Outlook (2026–2032)

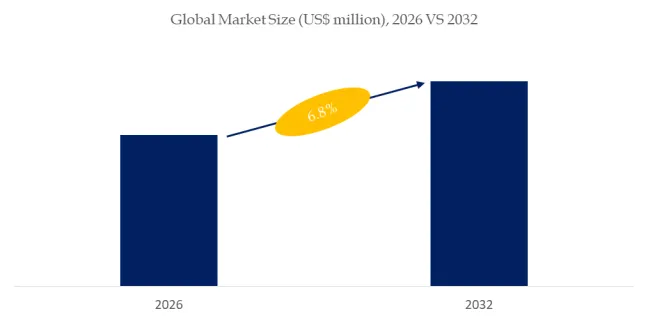

According to QYResearch data, the global market for transcritical CO2 cycle refrigeration systems was valued at approximately USD 3.2 billion in 2025 and is projected to reach USD 7.8 billion by 2032, growing at a compound annual growth rate (CAGR) of 13.6% from 2026 to 2032. This accelerated growth is driven by three converging factors: the accelerating global phase-down of HFC refrigerants under the Kigali Amendment (which entered its final compliance tranche for developed nations in January 2026), improved component reliability and cost reduction, and rising energy efficiency mandates across the EU, North America, and Asia-Pacific.

A transcritical CO2 cycle is defined as a refrigeration or heat pump cycle in which the compressor discharge pressure exceeds the critical pressure of carbon dioxide (73.8 bar). Under these conditions, the refrigerant cannot be condensed via isothermal condensation; instead, it is cooled without phase change in a gas cooler. The cycle operates at high compressor discharge temperatures and pressures (typically 80–120 bar) to enable effective heat exchange with ambient air or water. Unlike subcritical cycles that require a distinct condensing phase, the transcritical approach leverages CO2′s unique thermophysical properties—high volumetric capacity, low viscosity, and excellent heat transfer characteristics—to achieve compact system designs.

Key Industry Characteristics Driving Market Growth

1. Regulatory Acceleration: F-Gas Phase-Down as the Primary Market Catalyst

The regulatory landscape has fundamentally shifted in favor of natural refrigerants. The EU F-Gas Regulation (EU 2024/573), fully effective since January 2025, imposes a steep declining quota for HFCs, with an 80% reduction from 2015 levels by 2030. Similarly, the U.S. American Innovation and Manufacturing (AIM) Act, enforced by the EPA, has progressively restricted HFC production and consumption, with the final 85% step-down scheduled for 2036. In response, leading supermarket chains—including Aldi, Lidl, and Carrefour—have committed to CO2 transcritical systems for all new store openings. In December 2025, Walmart announced a USD 500 million retrofit program to convert 650 U.S. stores to transcritical CO2 systems by 2029, citing a projected 35% reduction in refrigerant-related compliance costs over the decade.

2. Technology Segmentation: Components and Integrated Systems

The report segments the market into four primary technology categories:

- CO2 Compressors (Approx. 38–42% of market value): The most critical component, requiring specialized designs to handle transcritical pressure differentials and high discharge temperatures (up to 160°C). Leading suppliers—including Bitzer, Danfoss, Mitsubishi Heavy Industries, and Panasonic—have introduced second-generation semi-hermetic and scroll compressors with improved oil management and reduced internal leakage. In February 2026, Bitzer launched its new Octagon™ series CO2 compressor, achieving a 15% increase in isentropic efficiency compared to previous models.

- CO2 Air Conditioning Systems (Fastest-growing segment, 18–20% CAGR): Automotive HVAC represents the largest subsegment, driven by the EU MAC Directive (2006/40/EC) which effectively bans high-GWP refrigerants in new vehicle models. Hanon Systems, Valeo, and Sanden now supply transcritical CO2 air conditioning units for electric vehicle platforms, where CO2′s superior heating performance at low ambient temperatures addresses a key EV range limitation. A typical user case: In January 2026, a major German OEM announced that its next-generation EV platform would exclusively use a transcritical CO2 heat pump system, reducing winter range loss by an estimated 30% compared to resistive heating.

- CO2 Heat Pumps (High-growth segment, 15–17% CAGR): Residential and commercial heat pump water heaters using transcritical CO2 cycles achieve coefficient of performance (COP) values of 3.5–4.5 even at outdoor temperatures as low as -15°C. Midea Welling, Panasonic, and OBRIST Engineering GmbH have led commercialization in European and Japanese markets. In November 2025, the Japanese government expanded its subsidy program for CO2 heat pump water heaters (Eco Cute), allocating an additional JPY 45 billion (USD 300 million) through 2027.

- Others: Including electronic expansion valves (EEVs), gas coolers, flash tanks, and system controllers. Sanhua Intelligent Control and CAREL INDUSTRIES have developed proprietary algorithms for transcritical cycle optimization, adjusting high-side pressure in real-time to maximize system COP across varying ambient conditions.

3. Regional Dynamics: Europe Leads, North America & Asia Accelerate

Europe remains the dominant market for transcritical CO2 refrigeration systems, accounting for approximately 55% of global revenue in 2025, driven by the EU’s aggressive F-Gas Regulation and widespread adoption in supermarket refrigeration. North America is the fastest-growing regional market (CAGR 16–18%), as major retailers convert legacy systems. Asia-Pacific, led by Japan and China, represents the largest market for CO2 heat pumps and automotive air conditioning systems.

Key Players & Competitive Landscape (2025–2026 Updates)

Leading global suppliers include Danfoss (market leader in valves and system controls), Bitzer (compressor technology), Panasonic (heat pumps), Mitsubishi Heavy Industries, Hanon Systems (automotive), Valeo, Sanden, DORIN, SRMTEC, OBRIST Engineering GmbH, Midea Welling, MAHLE, SONGZ, Sanhua Intelligent Control, and CAREL INDUSTRIES.

Recent strategic developments (last 6 months):

- Danfoss (March 2026) unveiled its third-generation CO2 adaptive liquid management (ALM) system, which reduces total refrigerant charge by 40% while maintaining system efficiency—a critical advancement for smaller-footprint convenience stores.

- Panasonic (December 2025) announced a strategic partnership with a North American supermarket chain to deploy transcritical CO2 booster systems across 200 locations, integrating waste heat recovery for store heating and hot water.

- Mitsubishi Heavy Industries (February 2026) launched a compact transcritical CO2 chiller for data center cooling, achieving a seasonal energy efficiency ratio (SEER) of 4.2, outperforming HFC-based alternatives by 18%.

- CAREL INDUSTRIES (January 2026) introduced an AI-driven controller for transcritical systems that uses cloud-based weather forecasting to pre-emptively adjust gas cooler fan speeds and high-side pressure, delivering measured energy savings of 12–15% in field trials across 50 Italian supermarkets.

Technical Challenges & Innovation Frontiers

Current technical hurdles include:

- High operating pressures: Transcritical CO2 systems operate at 80–140 bar, compared to 10–20 bar for HFC systems. This requires thicker-walled tubing, burst-proof fittings, and specialized brazing techniques. The industry has responded with standardized components (e.g., ISO 5149-3:2026-certified joints) and automated leak detection systems capable of identifying micro-leaks (below 0.1 oz/year).

- Efficiency degradation at high ambient temperatures: CO2 systems experience COP reduction when outdoor temperatures exceed 30°C due to the high pressure lift required. Ejector cycles and parallel compression architectures have emerged as solutions. In January 2026, a field study published by the European Partnership for Energy and Environment (EPEE) demonstrated that ejector-equipped transcritical systems maintain COP within 15% of HFC baselines even at 40°C ambient, compared to 35% degradation for basic booster systems.

- Compressor durability: The combination of high pressure, high discharge temperature, and the need for rapid cycling in automotive and heat pump applications accelerates wear. Advanced materials—including diamond-like carbon (DLC) coatings on bearing surfaces and aluminum-silicon alloy pistons—have extended compressor service intervals to 10,000+ hours in commercial applications.

Policy drivers (2025–2026):

- Kigali Amendment Implementation: The final compliance tranche for Article 5 (developing) countries begins in 2028, but early adopters (China, India, Brazil) have accelerated CO2 technology deployment to secure market share in export markets.

- EU Energy Efficiency Directive (EED) recast, effective July 2025, mandates that new commercial refrigeration systems above 50 kW cooling capacity achieve a minimum seasonal energy efficiency ratio (SEER) that effectively requires transcritical CO2 or other natural refrigerant solutions.

- U.S. EPA SNAP Rule 26 (December 2025) formally lists CO2 as an acceptable substitute in all refrigeration and air conditioning end-uses, removing previous use restrictions in certain retail food applications.

Exclusive Market Observations & Strategic Recommendations

Unlike conventional refrigeration market analyses, this report identifies three distinctive trends:

1. The convergence of cooling and heating is creating integrated system demand. Transcritical CO2 systems excel at simultaneous heating and cooling (heat recovery). A November 2025 installation at a Danish supermarket chain demonstrated 65% total energy savings when the CO2 system provided refrigeration, space heating, and hot water—compared to separate systems. This integrated approach is gaining traction in cold climates (Nordics, Canada, Northern China).

2. Light commercial applications are the next frontier. While supermarket refrigeration has driven early adoption, convenience stores, restaurants, and small grocery outlets represent an underserved segment. Danfoss and CAREL have launched scaled-down, pre-charged, plug-and-play transcritical units for sub-20 kW applications, reducing installation cost by an estimated 40% compared to custom-built systems.

3. The EV thermal management opportunity is transformative. Electric vehicles require both cabin air conditioning and battery thermal management. Transcritical CO2 systems can serve both functions with a single refrigerant circuit, eliminating separate cooling loops. Major automotive suppliers (Hanon, Valeo, MAHLE) are investing heavily in this application, with a projected 8–10 million CO2-equipped EVs on the road by 2030.

For facility managers, automotive engineers, and investors: The transcritical CO2 cycle refrigeration system market is entering a phase of accelerated mainstream adoption. Suppliers with integrated component portfolios (compressors, valves, controllers) and proven high-ambient performance are best positioned. End-users should prioritize systems with ejector or parallel compression architectures to maximize year-round efficiency and secure regulatory compliance through 2035 and beyond.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp

2890.webp)