QY Research Inc. (Global Market Report Research Publisher) announces the release of 2025 latest report “Railway Pantograph Slider- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. Based on current situation and impact historical analysis (2020-2024) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Railway Pantograph Slider market, including market size, share, demand, industry development status, and forecasts for the next few years.

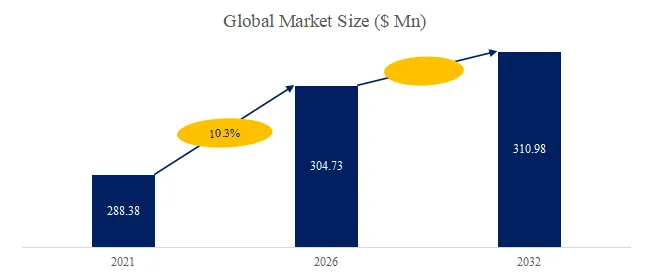

The global market for Railway Pantograph Slider was estimated to be worth US$ 301 million in 2025 and is projected to reach US$ 311 million, growing at a CAGR of 0.3% from 2026 to 2032.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/5504447/railway-pantograph-slider

Railway Pantograph Sliders

Railway pantograph sliders are key current-collecting components used in high-speed rail EMUs, electric locomotives, subways, and light rail systems. The slider directly contacts the overhead contact wire, and its performance is critical to power supply stability and train operational safety. Pantographs are generally classified into single-arm and double-arm types, with the slider being a typical wear part that requires periodic replacement.

According to the new market research report ” Global Railway Pantograph Slider Market Growth 2026-2032″, published by QYResearch, the global Railway Pantograph Slider market size is projected to grow from USD 304.73 million in 2026 to USD 310.98 million by 2032, at a CAGR of 0.3% during the forecast period.

Figure00002. Global Railway Pantograph Slider Market Insights, Forecast to 2032

Above data is based on report from QYResearch: Global Railway Pantograph Slider Market Growth 2026-2032

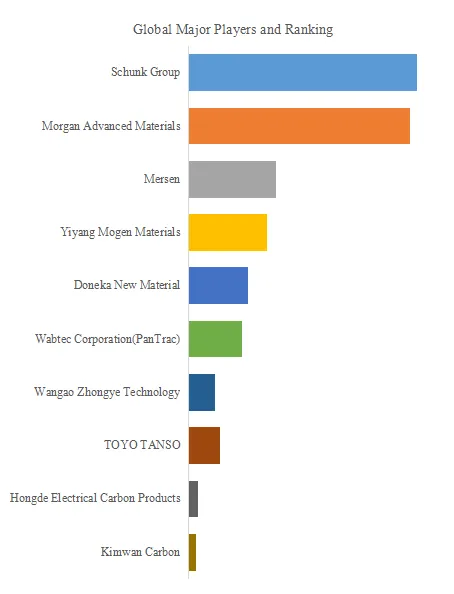

Figure00003. Global Railway Pantograph Slider Top 10 Players Ranking and Market Share (Ranking is based on the revenue of 2025, continually updated)

Above data is based on report from QYResearch: Global Railway Pantograph Slider Market Growth 2026-2032

This report profiles key players of Railway Pantograph Slider such as Schunk Group, Morgan Advanced Materials, Mersen, Yiyang Mogen Materials, Doneka New Material, Wabtec Corporation (PanTrac), Wangao Zhongye Technology, TOYO TANSO, Hongde Electrical Carbon Products, Kimwan Carbon.

In 2025, the global top five Railway Pantograph Slider players account for 67% of market share in terms of revenue. Above figure shows the key players ranked by revenue in Railway Pantograph Slider.

|

Company Name |

Description |

|

Schunk Group |

Schunk Group is an industrial technology group built around materials and engineering capabilities, with key activities spanning carbon/graphite solutions, technical ceramics, environmental simulation & climate technologies, sintered metals, and ultrasonic welding. It supplies critical components and systems to end markets such as energy, electrical engineering, high-temperature processes, transportation, and industrial equipment. Its Schunk Carbon Technology division is positioned as a global leader in the development, manufacturing, and application of carbon and graphite solutions, supported by a broad international manufacturing and sales footprint and application engineering services. |

|

Morgan Advanced Materials |

Morgan Advanced Materials is a global advanced materials and engineering solutions company organized around three core platforms: Thermal Products, Performance Carbon, and Technical Ceramics. It supplies materials, components, and systems to demanding applications across energy-intensive industry, transport, electronics, and high-temperature manufacturing. Its Thermal Ceramics business is described as engineering advanced ceramic insulation products and systems for high-temperature environments, helping customers reduce energy use and emissions while improving safety and process performance. |

|

Doneka New Material |

Doneka New Material is a China-based company focused on electro-carbon materials and carbon-based functional components. According to its official profile, it has long specialized in carbon material R&D and manufacturing, with major business lines including carbon brushes for automotive motors, home appliances and power tools, carbon contact strips/sliders for rail transit, industrial carbon brushes, and specialty carbon materials. Its products serve applications across automotive, rail transit, appliances, power tools, and power generation, with an emphasis on in-house innovation, patent accumulation, and customer-oriented delivery capability. |

|

Wangao Zhongye Technology |

Wangao Zhongye is a China-based electro-carbon materials supplier serving rail current-collection systems. Public company/project information indicates its core business includes R&D, manufacturing, sales, and technical services for pantograph carbon contact strips (carbon sliders), and it also provides agency sales services for certain imported carbon sliders. Its products are primarily used across high-speed trains, electric locomotives, metro, and light-rail applications, with an engineering-oriented delivery model typically combining product supply with field technical support and service. |

Market Drivers:

Demand for railway pantograph sliders grows alongside expanding rail and metro fleets, higher service intensity, and more standardized maintenance regimes. High-speed rail and dense urban operations raise requirements for current-collection stability, low failure rates, and predictive maintenance, driving continual upgrades in material systems, wear life, electrical resistance consistency, and thermal stability. In parallel, energy efficiency and environmental objectives—reducing arcing, wear debris, and contact-related damage—push the segment toward more consistent, engineering-grade products, sustaining recurring consumables replacement demand.

Restraint:

Constraints are driven by multi-objective performance trade-offs and lengthy system-level qualification. Pantograph sliders must balance conductivity, wear resistance, arc erosion resistance, mechanical strength, noise/vibration behavior, and catenary-friendliness—while route-specific factors (speed class, current load, climate, catenary material) strongly affect formulation fit. As a critical component within the pantograph–catenary system, large-scale adoption typically requires line trials, life validation, and operational proof, making qualification cycles long and switching costs high. Raw-material volatility (carbon/graphite, metal impregnation inputs, resins), lot-to-lot consistency, and variability in maintenance practices add uncertainty to failure rates and lifecycle economics.

Opportunity:

Opportunities arise from material upgrades, digitalized maintenance, and localization/dual-sourcing trends. Under higher speeds, higher current densities, and harsher operating conditions, advanced composites—optimized metal-impregnated systems, modified resin/carbon composites, functional fillers, and improved structural design—can improve arc resistance, wear life, and thermal behavior, increasing value per trainset and predictability of replacement cycles. As maintenance shifts toward condition-based approaches, wear monitoring, current-collection quality assessment, and data-driven acceptance elevate demand for consistency and traceable quality systems—favoring suppliers with engineering validation, process control, and field service capability. In parallel, supply-security and localization initiatives in multiple markets create entry windows for players that can meet qualification requirements while offering capacity assurance and fast delivery.

The report provides a detailed analysis of the market size, growth potential, and key trends for each segment. Through detailed analysis, industry players can identify profit opportunities, develop strategies for specific customer segments, and allocate resources effectively.

The Railway Pantograph Slider market is segmented as below:

By Company

Schunk Group

Morgan Advanced Materials

Mersen

Yiyang Mogen Materials

Doneka New Material

Wabtec Corporation (PanTrac)

TOYO TANSO

Wangao Zhongye Technology

Hongde Electrical Carbon Products

Kimwan Carbon

Segment by Type

Pure Carbon Slider

Metallic Carbon Slider

Other

Segment by Application

Electric Locomotive

EMU

Subway/Light Rail

Each chapter of the report provides detailed information for readers to further understand the Railway Pantograph Slider market:

Chapter 1: Introduces the report scope of the Railway Pantograph Slider report, global total market size (valve, volume and price). This chapter also provides the market dynamics, latest developments of the market, the driving factors and restrictive factors of the market, the challenges and risks faced by manufacturers in the industry, and the analysis of relevant policies in the industry. (2021-2032)

Chapter 2: Detailed analysis of Railway Pantograph Slider manufacturers competitive landscape, price, sales and revenue market share, latest development plan, merger, and acquisition information, etc. (2021-2026)

Chapter 3: Provides the analysis of various Railway Pantograph Slider market segments by Type, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different market segments. (2021-2032)

Chapter 4: Provides the analysis of various market segments by Application, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different downstream markets.(2021-2032)

Chapter 5: Sales, revenue of Railway Pantograph Slider in regional level. It provides a quantitative analysis of the market size and development potential of each region and introduces the market development, future development prospects, market space, and market size of each country in the world..(2021-2032)

Chapter 6: Sales, revenue of Railway Pantograph Slider in country level. It provides sigmate data by Type, and by Application for each country/region.(2021-2032)

Chapter 7: Provides profiles of key players, introducing the basic situation of the main companies in the market in detail, including product sales, revenue, price, gross margin, product introduction, recent development, etc. (2021-2026)

Chapter 8: Analysis of industrial chain, including the upstream and downstream of the industry.

Chapter 9: Conclusion.

Benefits of purchasing QYResearch report:

Competitive Analysis: QYResearch provides in-depth Railway Pantograph Slider competitive analysis, including information on key company profiles, new entrants, acquisitions, mergers, large market shear, opportunities, and challenges. These analyses provide clients with a comprehensive understanding of market conditions and competitive dynamics, enabling them to develop effective market strategies and maintain their competitive edge.

Industry Analysis: QYResearch provides Railway Pantograph Slider comprehensive industry data and trend analysis, including raw material analysis, market application analysis, product type analysis, market demand analysis, market supply analysis, downstream market analysis, and supply chain analysis.

and trend analysis. These analyses help clients understand the direction of industry development and make informed business decisions.

Market Size: QYResearch provides Railway Pantograph Slider market size analysis, including capacity, production, sales, production value, price, cost, and profit analysis. This data helps clients understand market size and development potential, and is an important reference for business development.

Other relevant reports of QYResearch:

Global Railway Pantograph Slider Market Insights – Industry Share, Sales Projections, and Demand Outlook 2026-2032

Global Railway Pantograph Slider Market Outlook, In‑Depth Analysis & Forecast to 2032

Global Railway Pantograph Slider Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

Global Railway Pantograph Slider Market Research Report 2026

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 19 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp