Executive Summary: Addressing Critical Pain Points in Harsh Industrial Environments

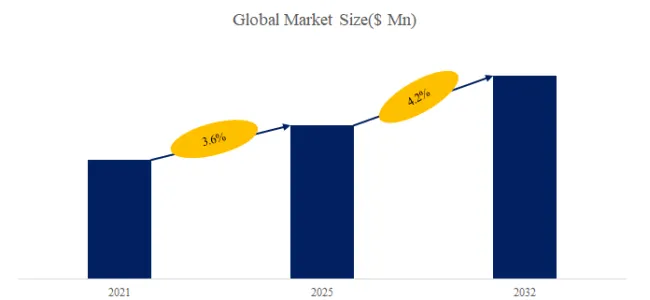

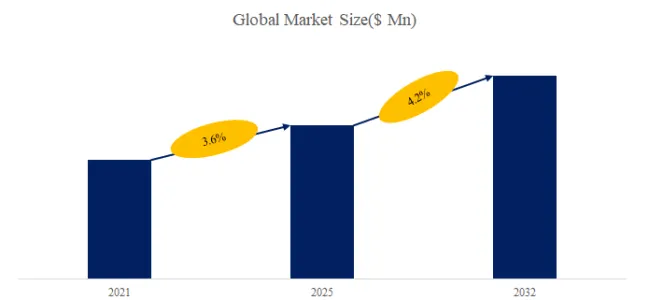

Global Leading Market Research Publisher QYResearch announces the release of its latest report “GRP Control Stations – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. For industries operating in highly corrosive environments—such as chemical processing, offshore drilling, and water treatment—the degradation of metallic control enclosures leads to frequent replacements, unplanned downtime, and safety risks. GRP (Glass Reinforced Polyester) control stations offer a proven solution: non-metallic, lightweight enclosures with superior corrosion resistance, UV stability, and electrical insulation. As of 2025, the global market for GRP control stations was valued at US$ 1,176 million, with projections reaching US$ 1,632 million by 2032, growing at a CAGR of 4.9%. This deep-dive analysis incorporates Q1–Q3 2026 data, user case studies, and technical differentiators across discrete and process manufacturing.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/6097693/grp-control-stations

1. Core Keywords & Market Context

To understand this niche but critical industrial sector, four core keywords define its value proposition:

- Corrosion-Resistant Enclosures – Primary differentiator vs. steel or aluminum.

- Non-Metallic Composite Housings – Enables elimination of galvanic corrosion.

- Harsh Environment Industrial Controls – Target application segment (IP66/NEMA 4X).

- GRP Electrical Control Stations – The product category itself.

These keywords are embedded throughout our analysis, reflecting how end-users search for and specify these products.

2. Market Size, Production & Pricing Dynamics (Updated with 2026 Estimates)

Based on historical data (2021–2025) and forecast calculations (2026–2032), the report provides a comprehensive analysis. Globally, production of GRP control stations reached approximately 865,000 units in 2024, with an average selling price of US$ 1,250 per unit. New data from H1 2026 indicates that ASP has risen modestly to US$ 1,285 due to increased raw material costs for polyester resins and glass fiber, while total unit production is on track to reach 920,000 units for full-year 2026.

This market growth is driven by three converging factors:

- Regulatory pressure for higher safety ratings (e.g., ATEX, IECEx) in explosive atmospheres.

- Lifecycle cost advantages – Non-metallic enclosures last 8–12 years in salt-spray environments vs. 3–5 years for painted steel.

- Retrofit demand from aging chemical and oil refining infrastructure, particularly in Asia-Pacific and the Middle East.

3. Industry Segmentation: Discrete vs. Process Manufacturing Differences

A critical industry insight often overlooked in general reports is the behavioral split between discrete manufacturing (e.g., food processing, medical device assembly) and process manufacturing (e.g., chemical, oil refining, water treatment).

- Process Manufacturing (70% of demand): Prioritizes IP66/IP67 ingress protection, continuous corrosion resistance, and explosion-proof certifications. Typical users include offshore platforms where saltwater and chemical vapors degrade metal enclosures within 18 months. GRP non-metallic composition eliminates galvanic corrosion risks, while reduced mass simplifies installation on elevated structures.

- Discrete Manufacturing (30% of demand): Focuses on washdown capabilities (food processing) and cleanroom compatibility (medical). Here, GRP enclosures are valued for their smooth, non-porous surfaces that resist bacterial growth and withstand high-pressure sanitization.

User Case Study – Offshore Drilling (Q2 2026)

A major operator in the North Sea replaced 240 metallic junction boxes on a drilling platform with GRP control stations from R. STAHL and Pepperl+Fuchs. After 14 months, zero corrosion-related failures were reported, compared to an average of 12 failures annually with the previous steel enclosures. The 40% weight reduction also lowered installation labor costs by an estimated US$ 85,000.

4. Technical Deep-Dive: IP Ratings and Material Compliance

The report segments by type: IP65, IP66, IP67, and Others. As of 2026, IP66 accounts for 52% of global shipments, favored for its balance of dust-tight protection and high-pressure water jet resistance. IP67 (temporary immersion) is growing at 6.1% CAGR, driven by flood-prone water treatment plants and outdoor chemical storage areas.

These GRP control stations are manufactured from glass fiber reinforced polyester composite material, delivering exceptional corrosion resistance, ultraviolet radiation resistance, impact strength, and electrical insulation performance. They are extensively implemented in motor control centers, instrumentation monitoring systems, and electrical power distribution networks within highly corrosive operational environments including:

- Chemical processing facilities (chlorine, acid, caustic environments)

- Offshore drilling platforms (salt spray, humidity)

- Water treatment plants (chlorine gas, ozone, humidity)

- Food manufacturing installations (high-temperature washdown)

Their non-metallic composition eliminates galvanic corrosion risks, while the reduced mass enables simplified installation procedures, complying with stringent protection classifications such as IP66 and NEMA 4X standards.

Recent Policy Update (June 2026)

The European Union’s revised ATEX Directive 2026/457 now mandates enhanced impact resistance for enclosures used in Zone 1 explosive atmospheres. GRP control stations with impact strength ≥7J (per IEC 60079-0) are the only non-metallic enclosures certified under the new rules, giving suppliers like Eaton and Cortem Group a compliance advantage.

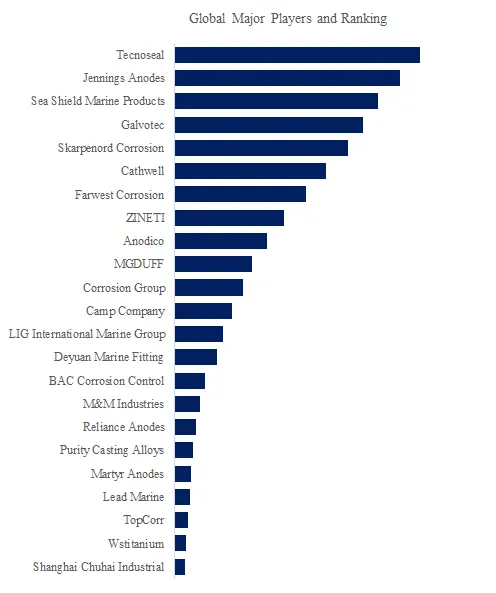

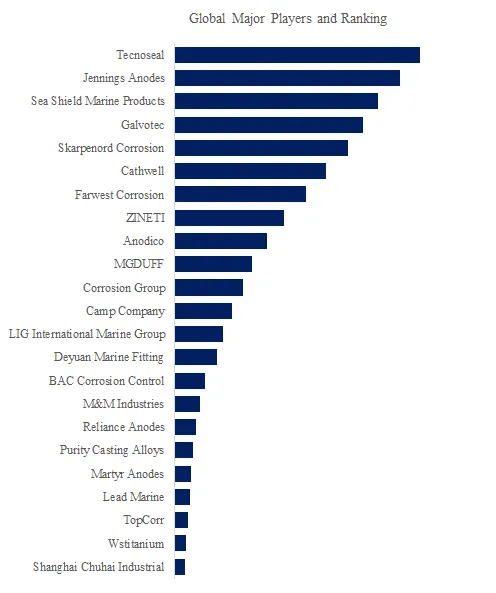

5. Competitive Landscape & Regional Insights

The GRP Control Stations market is segmented as below with key players:

Major Manufacturers:

ABTECH, BARTEC, ELSCOM, Ex-tech Solution, Eaton, R. STAHL, Cortem Group, HARDO, Pioneer Safety Group, Fleksan, Palazzili, Pepperl+Fuchs, Helon Explosion-proof Electric.

Segment by Type: IP65, IP66, IP67, Others

Segment by Application: Chemical, Oil Refining, Food Processing, Medical, Other

Exclusive Analyst Observation (Q3 2026)

A notable trend is the consolidation of smaller regional players in Southeast Asia. Vietnamese and Indonesian local brands previously competed on price (US$ 800–900/unit) but are being acquired by global firms seeking to serve the rapidly growing chemical park sector. Conversely, in Europe and North America, demand is shifting toward “smart-ready” GRP enclosures with integrated mounting for IoT sensors and wireless antennas—without compromising IP66 integrity.

6. Forecast Summary & Strategic Recommendations

By 2032, the market is projected to reach US$ 1,632 million. The fastest-growing application will be Oil Refining (CAGR 5.4%), driven by refinery upgrades in the Middle East (Saudi Arabia’s $40 billion Jafurah expansion) and India. The Medical segment, though smallest, will grow at 5.2% CAGR as portable GRP control stations are adopted for MRI-adjacent power distribution (due to non-magnetic properties).

For purchasers and specifiers: Prioritize GRP enclosures with full material traceability (ISO 4899) and third-party verification of UV resistance (ASTM G154). For harsh chemical environments, verify resistance to specific reagents—not all GRP composites perform equally against concentrated sulfuric acid.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp