QY Research Inc. (Global Market Report Research Publisher) announces the release of 2025 latest report “Fire Pump- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. Based on current situation and impact historical analysis (2020-2024) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Fire Pump market, including market size, share, demand, industry development status, and forecasts for the next few years.

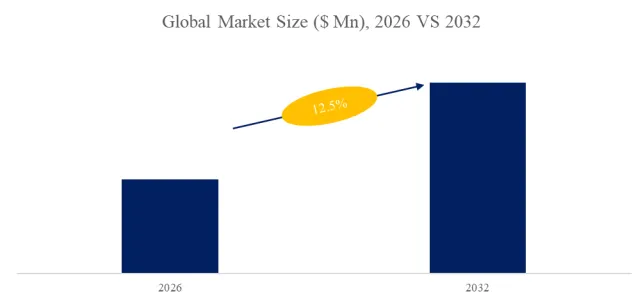

The global market for Fire Pump was estimated to be worth US$ 1549 million in 2025 and is projected to reach US$ 2004 million, growing at a CAGR of 3.8% from 2026 to 2032.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/5492734/fire-pump

Fire Pump Market Summary

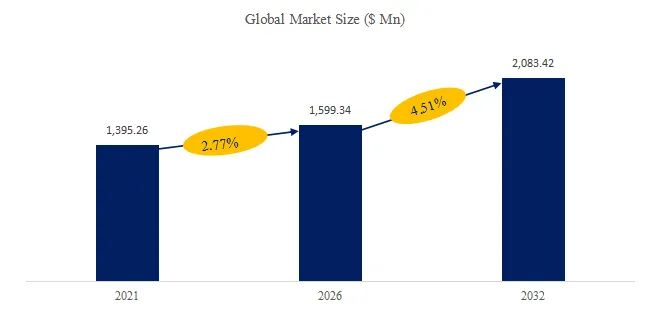

According to the new market research report “Global Fire Pump Market Report 2026-2032″, published by QYResearch, the global Fire Pump market size is projected to grow from USD 1,542 million in 2025 to USD 2,083 million by 2032, at a CAGR of 4.51% during the forecast period.

A fire pump is a part of a fire sprinkler system’s water supply and can be powered by electric, diesel or steam. The pump intake is either connected to the public underground water supply piping, or a static water source (e.g., tank, reservoir, lake). The pump provides water flow at a higher pressure to the sprinkler system risers and hose standpipes.

Market Drivers:

The growth of the fire pump market is primarily driven by regulations, construction activity, existing building renovations, and the need to protect high-value assets. Fundamentally, increasingly stringent fire safety regulations in various countries have made sprinkler and fire hydrant systems mandatory features in more and more buildings, directly driving the rigid demand for fire pumps as core water supply equipment. Simultaneously, the continuous increase in new projects such as commercial complexes, industrial plants, data centers, and warehousing and logistics facilities creates a stable source of incremental demand, as these scenarios have high requirements for the coverage and reliability of fire protection systems. On the existing building side, older buildings often require expansion or replacement of their original fire protection systems during compliance upgrades, repurposing changes, and safety renovations, providing a long-term and stable demand for upgrades. Furthermore, as the value of industrial facilities and critical infrastructure assets increases, companies are placing greater emphasis on fire risk control and business continuity, demanding higher levels of reliability, redundancy, and automation in fire water supply systems, further promoting the application of high-performance fire pumps and complete systems. In summary, this market exhibits a clear triple-driven characteristic: “regulatory necessity + construction cycle + safety upgrades,” with demand showing strong resilience and exhibiting a certain but not entirely synchronized relationship with the macroeconomic cycle.

Figure00001. Global Fire Pump Market Size (US$ Million), 2021-2032

Above data is based on report from QYResearch: Global Fire Pump Market Report 2026-2032 (published in 2025). If you need the latest data, plaese contact QYResearch.

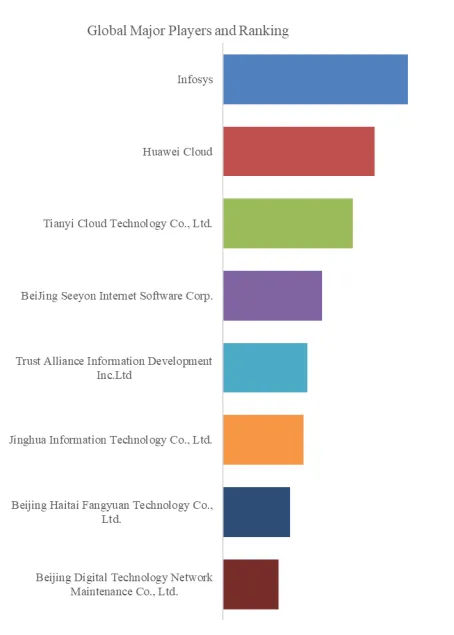

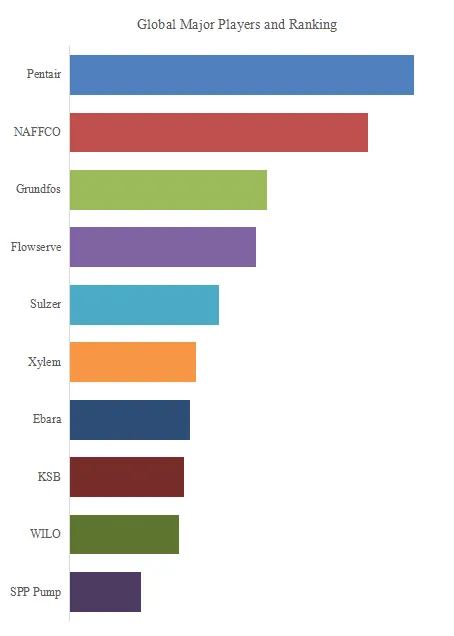

Figure00002. Global Fire Pump Top 10 Players Ranking and Market Share (Ranking is based on the revenue of 2025, continually updated)

Above data is based on report from QYResearch: Global Fire Pump Market Report 2026-2032 (published in 2025). If you need the latest data, plaese contact QYResearch.

According to QYResearch Top Players Research Center, the global key manufacturers of Fire Pump include Pentair, NAFFCO and Grundfos, etc. In 2025, the global top three players had a share approximately 25.9% in terms of revenue.

The report provides a detailed analysis of the market size, growth potential, and key trends for each segment. Through detailed analysis, industry players can identify profit opportunities, develop strategies for specific customer segments, and allocate resources effectively.

The Fire Pump market is segmented as below:

By Company

Pentair

NAFFCO

Grundfos

Flowserve

Sulzer

Xylem

Ebara

KSB

WILO

SPP Pump

Patterson Pump Company

Shanghai Kaiquan

Teral

Ruhrpumpen

SFFECO

PACIFIC PUMP

Shaanxi Aerospace Power

EAST PUMP

MAS Pumps

ZHONGQUAN Pump

Segment by Type

E-motor Drive

Diesel Drive

Segment by Application

Residential Application

Commercial Application

Industry Application

Each chapter of the report provides detailed information for readers to further understand the Fire Pump market:

Chapter 1: Introduces the report scope of the Fire Pump report, global total market size (valve, volume and price). This chapter also provides the market dynamics, latest developments of the market, the driving factors and restrictive factors of the market, the challenges and risks faced by manufacturers in the industry, and the analysis of relevant policies in the industry. (2021-2032)

Chapter 2: Detailed analysis of Fire Pump manufacturers competitive landscape, price, sales and revenue market share, latest development plan, merger, and acquisition information, etc. (2021-2026)

Chapter 3: Provides the analysis of various Fire Pump market segments by Type, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different market segments. (2021-2032)

Chapter 4: Provides the analysis of various market segments by Application, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different downstream markets.(2021-2032)

Chapter 5: Sales, revenue of Fire Pump in regional level. It provides a quantitative analysis of the market size and development potential of each region and introduces the market development, future development prospects, market space, and market size of each country in the world..(2021-2032)

Chapter 6: Sales, revenue of Fire Pump in country level. It provides sigmate data by Type, and by Application for each country/region.(2021-2032)

Chapter 7: Provides profiles of key players, introducing the basic situation of the main companies in the market in detail, including product sales, revenue, price, gross margin, product introduction, recent development, etc. (2021-2026)

Chapter 8: Analysis of industrial chain, including the upstream and downstream of the industry.

Chapter 9: Conclusion.

Benefits of purchasing QYResearch report:

Competitive Analysis: QYResearch provides in-depth Fire Pump competitive analysis, including information on key company profiles, new entrants, acquisitions, mergers, large market shear, opportunities, and challenges. These analyses provide clients with a comprehensive understanding of market conditions and competitive dynamics, enabling them to develop effective market strategies and maintain their competitive edge.

Industry Analysis: QYResearch provides Fire Pump comprehensive industry data and trend analysis, including raw material analysis, market application analysis, product type analysis, market demand analysis, market supply analysis, downstream market analysis, and supply chain analysis.

and trend analysis. These analyses help clients understand the direction of industry development and make informed business decisions.

Market Size: QYResearch provides Fire Pump market size analysis, including capacity, production, sales, production value, price, cost, and profit analysis. This data helps clients understand market size and development potential, and is an important reference for business development.

Other relevant reports of QYResearch:

Global Fire Pump Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

Global Fire Pump Market Research Report 2026

Fire Pump Set- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032

Global Fire Pump Set Market Research Report 2026

Global Pool Fire Pump Market Outlook, In‑Depth Analysis & Forecast to 2032

Global Pool Fire Pump Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

Global Pool Fire Pump Market Research Report 2026

Pool Fire Pump- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032

Global Fire Pump Truck Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

Global Fire Pump Truck Market Outlook, In‑Depth Analysis & Forecast to 2032

Fire Pump Truck- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032

Global Fire Pump Truck Market Research Report 2026

Global Diesel Fire Pump Market Research Report 2026

Global Marine Fire Pump Market Research Report 2026

Fire Pump Cannon- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032

Fire Pump Motors- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032

Global Fire Pump Cannon Market Research Report 2026

Global Fire Pump Motors Market Research Report 2026

Global Fire Pump Trailer Market Research Report 2026

Fire Pump Service – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 19 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp