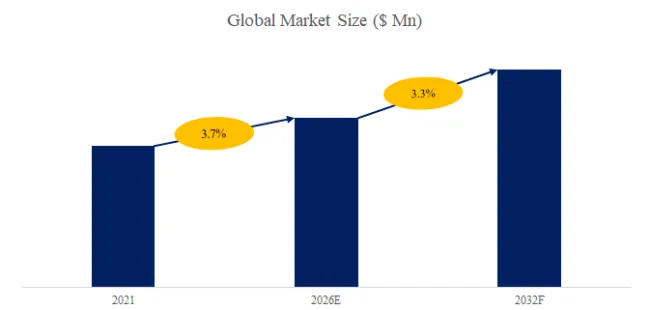

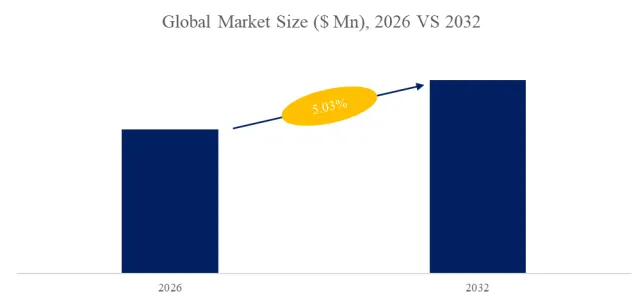

The global market for Automatic High Speed Checkweigher was estimated to be worth US$ 583 million in 2025 and is projected to reach US$ 782 million, growing at a CAGR of 4.4% from 2026 to 2032.

A 2026 latest Report by QYResearch offers on -“Automatic High Speed Checkweigher – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032” provides an extensive examination of Automatic High Speed Checkweigher market attributes, size assessments, and growth projections through segmentation, regional analyses, and country-specific insights, alongside a scrutiny of the competitive landscape, player market shares, and essential business strategies.

The research report encompasses a comprehensive analysis of the factors that affect the growth of the market. It includes an evaluation of trends, restraints, and drivers that influence the market positively or negatively. The report also outlines the potential impact of different segments and applications on the market in the future. The information presented is based on historical milestones and current trends, providing a detailed analysis of the production volume for each type from 2020 to 2032, as well as the production volume by region during the same period.

This inquiry delivers a thorough perspective with valuable insights, accentuating noteworthy outcomes in the industry. These insights empower corporate leaders to formulate improved business strategies and make more astute decisions, ultimately enhancing profitability. Furthermore, the study assists private or venture participants in gaining a deep understanding of businesses, enabling them to make well-informed choices.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/6092628/automatic-high-speed-checkweigher

The report provides a detailed analysis of the market size, growth potential, and key trends for each segment. Through detailed analysis, industry players can identify profit opportunities, develop strategies for specific customer segments, and allocate resources effectively.

The Automatic High Speed Checkweigher market is segmented as below:

By Company

Mettler Toledo

Ishida

Wipotec

High Dream

Anritsu

Marel

Yamato Scale

General Measure

All Fill Inc.

Dibal

A&D Company

LCS Controls

Spee-Dee

Flintec

Easyweigh

Fanchi-tech

Dream Vision

Shandong SeTAQ

Segment by Type

100-300 bag/min

300-500 bag/min

>500 bag/min

Segment by Application

Food and Beverages

Pharmaceuticals

Cosmetics

Others

The Automatic High Speed Checkweigher report is compiled with a thorough and dynamic research methodology.

The report offers a complete picture of the competitive scenario of Automatic High Speed Checkweigher market.

It comprises vast amount of information about the latest technology and product developments in the Automatic High Speed Checkweigher industry.

The extensive range of analyses associates with the impact of these improvements on the future of Automatic High Speed Checkweigher industry growth.

The Automatic High Speed Checkweigher report has combined the required essential historical data and analysis in the comprehensive research report.

The insights in the Automatic High Speed Checkweigher report can be easily understood and contains a graphical representation of the figures in the form of bar graphs, statistics, and pie charts, etc.

Each chapter of the report provides detailed information for readers to further understand the Automatic High Speed Checkweigher market:

Chapter 1- Executive summary of market segments by Type, market size segments for North America, Europe, Asia Pacific, Latin America, Middle East & Africa.

Chapter 2- Detailed analysis of Automatic High Speed Checkweigher manufacturers competitive landscape, price, sales, revenue, market share and ranking, latest development plan, merger, and acquisition information, etc.

Chapter 3- Sales, revenue of Automatic High Speed Checkweigher in regional level. It provides a quantitative analysis of the market size and development potential of each region and introduces the future development prospects, and market space in the world.

Chapter 4- Introduces market segments by Application, market size segment for North America, Europe, Asia Pacific, Latin America, Middle East & Africa.

Chapter 5,6,7,8,9 – North America, Europe, Asia Pacific, Latin America, Middle East & Africa, sales and revenue by country.

Chapter 10- Provides profiles of key players, introducing the basic situation of the main companies in the market in detail, including product sales, revenue, price, gross margin, product introduction, recent development, etc.

Chapter 11- Analysis of industrial chain, key raw materials, manufacturing cost, and market dynamics. Introduces the market dynamics, latest developments of the market, the driving factors and restrictive factors of the market, the challenges and risks faced by manufacturers in the industry, and the analysis of relevant policies in the industry.

Chapter 12 – Analysis of sales channel, distributors and customers.

Chapter 13- Research Findings and Conclusion.

Table of Contents

1 Automatic High Speed Checkweigher Market Overview

1.1 Automatic High Speed Checkweigher Product Overview

1.2 Automatic High Speed Checkweigher Market by Type

1.3 Global Automatic High Speed Checkweigher Market Size by Type

1.3.1 Global Automatic High Speed Checkweigher Market Size Overview by Type (2021-2032)

1.3.2 Global Automatic High Speed Checkweigher Historic Market Size Review by Type (2021-2026)

1.3.3 Global Automatic High Speed Checkweigher Forecasted Market Size by Type (2026-2032)

1.4 Key Regions Market Size by Type

1.4.1 North America Automatic High Speed Checkweigher Sales Breakdown by Type (2021-2026)

1.4.2 Europe Automatic High Speed Checkweigher Sales Breakdown by Type (2021-2026)

1.4.3 Asia-Pacific Automatic High Speed Checkweigher Sales Breakdown by Type (2021-2026)

1.4.4 Latin America Automatic High Speed Checkweigher Sales Breakdown by Type (2021-2026)

1.4.5 Middle East and Africa Automatic High Speed Checkweigher Sales Breakdown by Type (2021-2026)

2 Automatic High Speed Checkweigher Market Competition by Company

3 Automatic High Speed Checkweigher Status and Outlook by Region

3.1 Global Automatic High Speed Checkweigher Market Size and CAGR by Region: 2021 VS 2024 VS 2032

3.2 Global Automatic High Speed Checkweigher Historic Market Size by Region

3.2.1 Global Automatic High Speed Checkweigher Sales in Volume by Region (2021-2026)

3.2.2 Global Automatic High Speed Checkweigher Sales in Value by Region (2021-2026)

3.2.3 Global Automatic High Speed Checkweigher Sales (Volume & Value), Price and Gross Margin (2021-2026)

3.3 Global Automatic High Speed Checkweigher Forecasted Market Size by Region

3.3.1 Global Automatic High Speed Checkweigher Sales in Volume by Region (2026-2032)

3.3.2 Global Automatic High Speed Checkweigher Sales in Value by Region (2026-2032)

3.3.3 Global Automatic High Speed Checkweigher Sales (Volume & Value), Price and Gross Margin (2026-2032)

…

Our Service:

1.Express Delivery Report Service

2.More than 19 years of vast experience

3.Establish offices in 6 countries

4.Operation for 24 * 7 & 365 days

5.Owns large database

6.In-depth and comprehensive analysis

7.Professional and timely after-sales service

To contact us and get this report: https://www.qyresearch.com/reports/6092628/automatic-high-speed-checkweigher

About Us:

As an independent global market research firm, one of our greatest strengths is our commitment to an objective and impartial third-party stance. We are not affiliated with any specific company or interest group, and all our research and analysis are grounded in facts and data. This independence ensures our reports and advisory recommendations maintain high credibility and reference value, serving as the most trusted objective basis for clients making investment decisions, conducting competitive analysis, and formulating strategic adjustments in complex market environments.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp