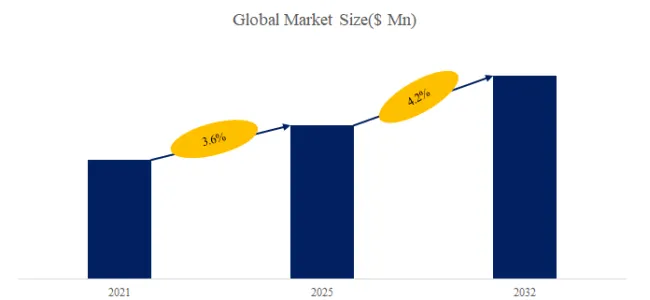

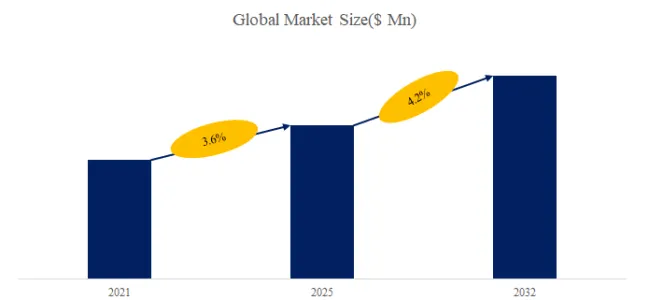

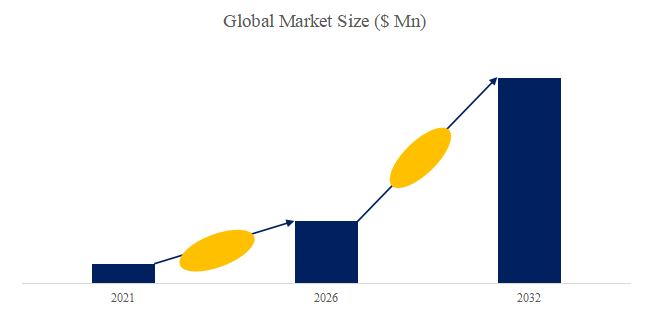

The global market for Infrared Thermal Imaging Analyzers was estimated to be worth US$ 517 million in 2025 and is projected to reach US$ 724 million, growing at a CAGR of 5.0% from 2026 to 2032.

Global Market Research Publisher QYResearch announces the release of its lastest report “Infrared Thermal Imaging Analyzers – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. Based on historical analysis (2021-2025) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Infrared Thermal Imaging Analyzers market, including market size, share, demand, industry development status, and forecasts for the next few years. Provides advanced statistics and information on global market conditions and studies the strategic patterns adopted by renowned players across the globe.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/5761349/infrared-thermal-imaging-analyzers

Some of the Key Questions Answered in this Report:

What is the Infrared Thermal Imaging Analyzers market size at the regional and country-level

What are the key drivers, restraints, opportunities, and challenges of the Infrared Thermal Imaging Analyzers market, and how they are expected to impact the market

What is the global (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa) sales value, production value, consumption value, import and export of Infrared Thermal Imaging Analyzers

Who are the global key manufacturers of the Infrared Thermal Imaging Analyzers Industry, How is their operating situation (capacity, production, sales, price, cost, gross, and revenue)

What are the Infrared Thermal Imaging Analyzers market opportunities and threats faced by the vendors in the global Infrared Thermal Imaging Analyzers Industry

Which application/end-user or product type may seek incremental growth prospects,What is the market share of each type and application

What focused approach and constraints are holding the Infrared Thermal Imaging Analyzers market

What are the different sales, marketing, and distribution channels in the global industry

What are the upstream raw materials andof Infrared Thermal Imaging Analyzers along with the manufacturing process of Infrared Thermal Imaging Analyzers

What are the key market trends impacting the growth of the Infrared Thermal Imaging Analyzers market

Economic impact on the Infrared Thermal Imaging Analyzers industry and development trend of the Infrared Thermal Imaging Analyzers industry

What are the Infrared Thermal Imaging Analyzers market opportunities, market risk, and market overview of the Infrared Thermal Imaging Analyzers market

Overall, this report strives to provide you with the insights and information you need to make informed business decisions and stay ahead of the competition.

All findings, data and information provided in the report have been verified and re-verified with the help of reliable sources. The analysts who wrote the report conducted in-depth research using unique and industry-best research and analysis methods.

The report provides a detailed analysis of the market size, growth potential, and key trends for each segment. Through detailed analysis, industry players can identify profit opportunities, develop strategies for specific customer segments, and allocate resources effectively.

The Infrared Thermal Imaging Analyzers market is segmented as below:

By Company

FLIR Systems, Inc.

Fluke Corporation

Testo SE & Co. KGaA

Seek Thermal, Inc.

Hikvision

Infratec (A Part of Jenoptik)

Optris GmbH

Axis Communications

Teledyne FLIR (Formerly Teledyne DALSA)

Sierra-Olympic Technologies, Inc.

Leonardo DRS

Infrared Cameras Inc.

SATIR Europe (Ireland) Ltd.

ULIS (A subsidiary of Sofradir Group)

NEC Avio Infrared Technologies Co., Ltd.

Guide Infrared

Segment by Type

Handheld Thermal Cameras

Fixed/Mounted Thermal Cameras

Segment by Application

Building Diagnostics

Electrical Maintenance

Energy Audits

Firefighting and Rescue

Automotive

Medica

Others

This information will help stakeholders make informed decisions and develop effective strategies for growth. The report’s analysis of the restraints in the market is crucial for strategic planning as it helps stakeholders understand the challenges that could hinder growth. This information will enable stakeholders to devise effective strategies to overcome these challenges and capitalize on the opportunities presented by the growing market. Furthermore, the report incorporates the opinions of market experts to provide valuable insights into the market’s dynamics. This information will help stakeholders gain a better understanding of the market and make informed decisions.

Each chapter of the report provides detailed information for readers to further understand the Infrared Thermal Imaging Analyzers market:

Chapter One: Introduces the study scope of this report, executive summary of market segments by Type, market size segments for North America, Europe, Asia Pacific, Latin America, Middle East & Africa.

Chapter Two: Detailed analysis of Infrared Thermal Imaging Analyzers manufacturers competitive landscape, price, sales, revenue, market share and ranking, latest development plan, merger, and acquisition information, etc.

Chapter Three: Sales, revenue of Infrared Thermal Imaging Analyzers in regional level. It provides a quantitative analysis of the market size and development potential of each region and introduces the future development prospects, and market space in the world.

Chapter Four: Introduces market segments by Application, market size segment for North America, Europe, Asia Pacific, Latin America, Middle East & Africa.

Chapter Five, Six, Seven, Eight and Nine: North America, Europe, Asia Pacific, Latin America, Middle East & Africa, sales and revenue by country.

Chapter Ten: Provides profiles of key players, introducing the basic situation of the main companies in the market in detail, including product sales, revenue, price, gross margin, product introduction, recent development, etc.

Chapter Eleven: Analysis of industrial chain, key raw materials, manufacturing cost, and market dynamics. Introduces the market dynamics, latest developments of the market, the driving factors and restrictive factors of the market, the challenges and risks faced by manufacturers in the industry, and the analysis of relevant policies in the industry.

Chapter Twelve: Analysis of sales channel, distributors and customers.

Chapter Thirteen: Research Findings and Conclusion.

Table of Contents

1 Infrared Thermal Imaging Analyzers Market Overview

1.2 Infrared Thermal Imaging Analyzers Market by Type

1.3 Global Infrared Thermal Imaging Analyzers Market Size by Type

1.4 Key Regions Market Size by Type

1.4.1 North America Infrared Thermal Imaging Analyzers Sales Breakdown by Type (2021-2026)

1.4.2 Europe Infrared Thermal Imaging Analyzers Sales Breakdown by Type (2021-2026)

1.4.3 Asia-Pacific Infrared Thermal Imaging Analyzers Sales Breakdown by Type (2021-2026)

1.4.4 Latin America Infrared Thermal Imaging Analyzers Sales Breakdown by Type (2021-2026)

1.4.5 Middle East and Africa Infrared Thermal Imaging Analyzers Sales Breakdown by Type (2021-2026)

2 Infrared Thermal Imaging Analyzers Market Competition by Company

2.1 Global Top Players by Infrared Thermal Imaging Analyzers Sales (2021-2026)

2.2 Global Top Players by Infrared Thermal Imaging Analyzers Revenue (2021-2026)

2.3 Global Top Players by Infrared Thermal Imaging Analyzers Price (2021-2026)

2.4 Global Top Manufacturers Infrared Thermal Imaging Analyzers Manufacturing Base Distribution, Sales Area, Product Type

2.5 Infrared Thermal Imaging Analyzers Market Competitive Situation and Trends

2.5.1 Infrared Thermal Imaging Analyzers Market Concentration Rate (2021-2026)

2.5.2 Global 5 and 10 Largest Manufacturers by Infrared Thermal Imaging Analyzers Sales and Revenue in 2025

2.6 Global Top Manufacturers by Company Type (Tier 1, Tier 2, and Tier 3) & (based on the Revenue in Infrared Thermal Imaging Analyzers as of 2025)

2.7 Date of Key Manufacturers Enter into Infrared Thermal Imaging Analyzers Market

2.8 Key Manufacturers Infrared Thermal Imaging Analyzers Product Offered

2.9 Mergers & Acquisitions, Expansion

3 Infrared Thermal Imaging Analyzers Status and Outlook by Region

3.1 Global Infrared Thermal Imaging Analyzers Market Size and CAGR by Region: 2021 VS 2025 VS 2032

3.2 Global Infrared Thermal Imaging Analyzers Historic Market Size by Region

3.3 Global Infrared Thermal Imaging Analyzers Forecasted Market Size by Region

…

Our Service:

1.Express Delivery Report Service

2.More than 19 years of vast experience

3.Establish offices in 6 countries

4.Operation for 24 * 7 & 365 days

5.Owns large database

6.In-depth and comprehensive analysis

7.Professional and timely after-sales service

To contact us and get this report: https://www.qyresearch.com/reports/5761349/infrared-thermal-imaging-analyzers

About Us:

QYResearch’s core competitiveness lies in our unique full industry chain research perspective. We go beyond isolated segments to map the complete industrial ecosystem for our clients. Over 19 years of accumulation have allowed us to build a database covering thousands of industrial chains. This panoramic analytical capability enables clients to precisely locate their position in the value chain, identify opportunities and risks upstream and downstream, and formulate more synergistic and competitive development strategies.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc (QYResearch).

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp