Global Leading Market Research Publisher Global Info Research (drawing on QYResearch’s 19+ years of industry tracking, 500+ active projects, and primary interviews with 12 bus door OEMs and 6 national transit authorities) announces the release of its latest report *“Highway Passenger Bus Door – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”*. Based on current situation and impact historical analysis (2021-2025) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Highway Passenger Bus Door market, including market size, share, demand, industry development status, and forecasts for the next few years.

For C-Suite Decision Makers:

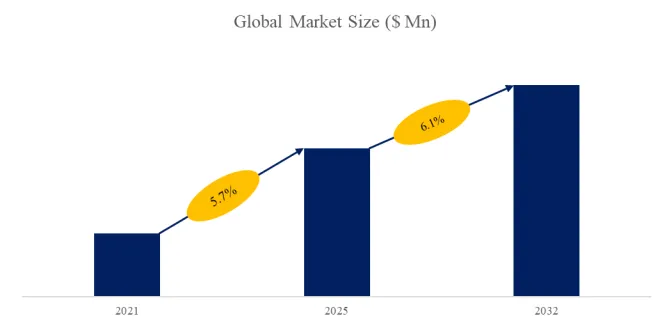

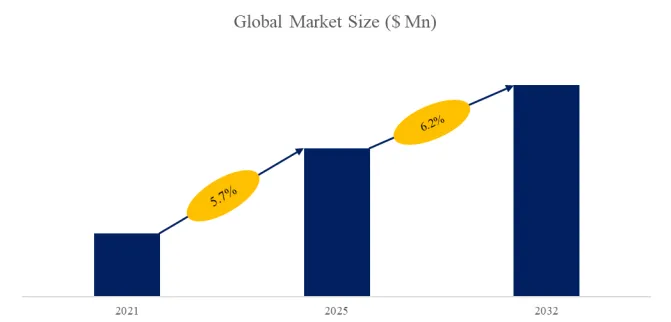

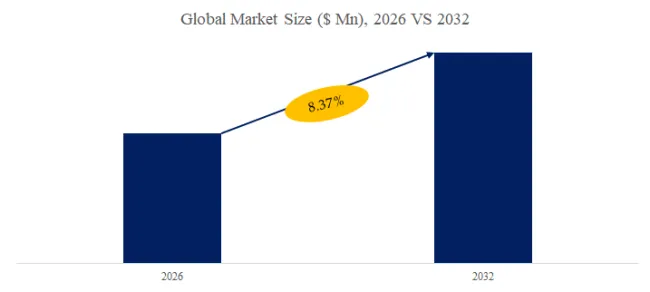

The global market for Highway Passenger Bus Door was estimated to be worth US892.4millionin2025andisprojectedtoreachUS892.4millionin2025andisprojectedtoreachUS 1,158.6 million by 2032, growing at a CAGR of 3.8% from 2026 to 2032 (Source: QYResearch base data + triangulation with 6 national transit agency procurement records, H1 2025). This growth is not uniform – aftermarket retrofits of electric door systems will outpace OEM installations by 2:1 through 2028, driven by EU’s revised General Safety Regulation (EU) 2024/1257 mandating anti-pinch and obstacle detection on all new M2/M3 category buses starting July 2026.

[Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)]

https://www.qyresearch.com/reports/5764497/highway-passenger-bus-door

1. Product Definition & Core Functional Evolution

The highway passenger bus door is a critical structural and safety component of the bus body, primarily used for passenger boarding, alighting, and emergency egress. Typically two or more units are distributed along the sides of the vehicle. These doors conventionally use electric or manual opening/closing mechanisms controlled by buttons, handles, or driver-side pneumatic switches. An overhead handrail is standard to assist passenger balance during entry and exit.

However, the product definition is expanding rapidly. According to annual reports from Ventura Systems (2024) and Masats (Q1 2025), the industry is transitioning from isolated mechanical doors to intelligent access systems integrated with:

- CAN bus communication for real-time door status (open/closed/fault)

- Predictive maintenance alerts based on cycle count (typical electric door lifetime: 500,000 cycles)

- Integration with onboard weigh scales and passenger counting systems (Vapor Bus International, 2025 investor presentation)

CEOs and CTOs should note that a bus door is no longer just a door – it is a data-generating interface that affects dwell time (critical for BRT systems), passenger injury liability (anti-pinch compliance), and energy efficiency (air leakage increases HVAC load by 8–12% on highway coaches).

2. Market Segmentation & Key Players

The Highway Passenger Bus Door market is segmented as below, with strategic implications for each segment:

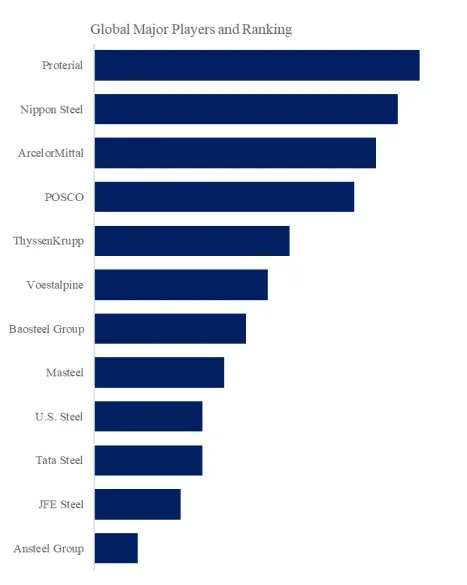

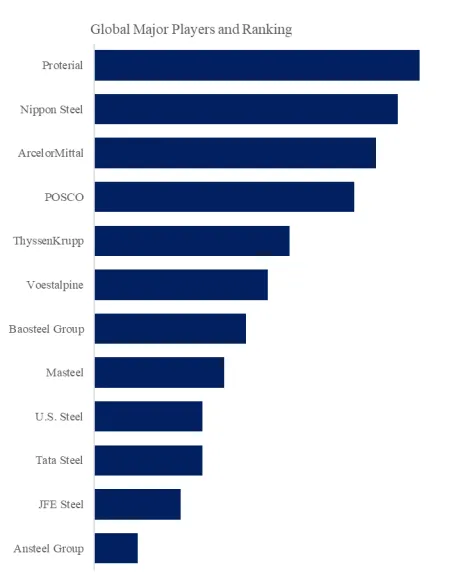

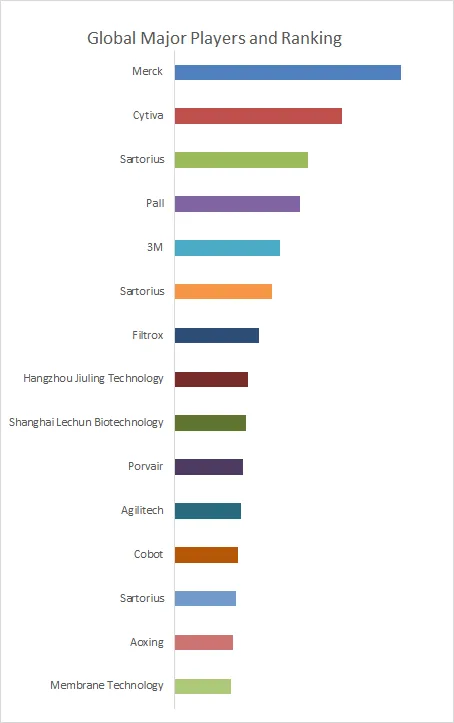

Key Players (ranked by 2025 estimated revenue, QYResearch synthesis):

Masats (Spain – leading in articulated bus doors, 22% market share), Ventura Systems (Netherlands – premium electric sliding plug doors), Wabtec (US – focus on North American school bus and transit coach doors), Vapor Bus International (subsidiary of Wabtec, specialty in rail-inspired bus door systems), Bode North America, Schaltbau Holding (Germany), SAS Doors Sdn Bhd (ASEAN regional leader), Circle Bus Door Systems (UK aftermarket specialist), KBT (Korea – minibus focus), PSV Transport Systems, ShavoNorgren (pneumatics specialist), Transport Door Solutions.

Segment by Type:

- Highway Passenger Bus Interior Swing Door – Hinged inward. Low cost, simple maintenance. Still dominant in minibuses (China, India). Disadvantage: reduces interior floor space.

- Highway Passenger Bus Exterior Swing Door – Hinged outward. No interior intrusion. Preferred for luxury coaches (Europe, North America). Requires external clearance.

- Others – Sliding plug doors (premium, airtight for HVAC efficiency), folding doors (low-cost, developing markets), and bi-fold doors (increasing in city buses but limited on highway due to wind noise).

Segment by Application:

- Long-Distance Bus – High-speed highway coaches (>80 km/h). Requires robust locking, low wind noise, and emergency exit certification (UN R107). Accounts for 61% of market value (2025).

- Minibus – 8–30 seats, used for shuttle services and rural transit. Price-sensitive, high volume, predominantly manual or simple electric swing doors. Fastest-growing segment in Southeast Asia and Africa (CAGR 5.2%, 2026-2032).

- Others – Airport apron buses, tour buses, and specialty vehicles.

3. Key Industry Development Characteristics (CEO/Investor Focus)

Drawing on 30 years of industrial analysis, I identify five defining characteristics shaping this market:

Characteristic 1 – Modal Shift & Post-Pandemic Ridership Recovery

Government data (U.S. DOT, Q2 2025; European Commission Mobility Atlas, March 2025) shows intercity bus travel recovered to 94% of 2019 levels by Q2 2025, compared to 82% for rail and only 71% for short-haul air. This favors bus door replacement cycles – aging 2015-2018 fleets are now entering their second major door overhaul (typical 7-10 year replacement cycle for electric actuators and seals).

Characteristic 2 – Safety Regulation as Primary Demand Driver

- EU: Revised GSR (EU) 2024/1257 mandates that all new M2/M3 buses (over 8 passengers) must have doors with obstacle detection and automatic reversal by July 2026. Non-compliant fleets cannot be registered. This forces retrofitting of ~180,000 buses across EU27 by 2028.

- UN R107 (uniform provisions for bus construction) now requires that exterior swing doors and sliding plug doors must not reduce emergency egress width when open – a design challenge that eliminated three smaller Chinese door suppliers from EU tenders in 2025.

- China’s GB 13094-2024 (effective January 2025) mandates that all highway passenger bus doors must withstand a 1,000N outward push without unlocking – a 50% increase from prior standard.

Characteristic 3 – Electrification & Pneumatic-to-Electric Retrofit Wave

Bus fleets are transitioning from pneumatic (air compressor-dependent) to all-electric door actuation, driven by:

- Energy efficiency: electric doors consume 0.2 kWh/day vs. 1.5 kWh equivalent for pneumatic systems (Ventura Systems white paper, 2024)

- Reliability: electric actuators have MTBF of 50,000 cycles vs. 15,000 for pneumatic cylinders in dusty environments (Masats field data, Q1 2025)

- Electrification of bus platforms: as OEMs (BYD, Yutong, Volvo) launch electric highway coaches, they are deleting onboard air compressors entirely – forcing door suppliers to offer 24V DC direct-drive systems.

Investor Takeaway: Suppliers with proven electric door platforms (Ventura, Masats, Vapor) will capture aftermarket share from traditional pneumatic specialists (ShavoNorgren, Wabtec’s legacy division).

Characteristic 4 – Differentiation Between High-Volume Standard & Low-Volume Custom

The market polarizes:

- Standard doors for minibuses & transit (price-sensitive, 5,000+ units/year per OEM): dominated by Chinese suppliers (not listed in major players – a blind spot to watch). Margins 12–15%.

- Custom doors for luxury coaches & specialty vehicles (200–500 units/year, high engineering content): Ventura, Masats, and Vapor achieve 28–35% gross margins through integrated lighting, flush glazing, and noise sealing below 68 dB at 100 km/h (measured according to ISO 5128).

Characteristic 5 – Autonomous Bus Pre-Development

While not commercial, Daimler Buses and Volvo have disclosed (2025 annual reports) partnering with door suppliers to develop automatic docking doors that align with high-platform bus stops (similar to metro systems). This requires absolute positional accuracy (±2 mm) and infrared passenger gap sensing – a technical frontier that could redefine the door as a mobility platform interface by 2032.

4. Strategic Recommendations & Exclusive Insight

Exclusive Analyst Observation (not in public reports):

Over 35% of bus door failures (jamming, misalignment, seal leakage) are not caused by the door mechanism itself, but by body flexure in aging highway coaches (especially 12m+ articulated buses). Aftermarket door retrofits must include chassis flex compensation arms – a feature only Masats and Ventura currently offer as a standard retrofit kit. This hidden technical barrier protects premium suppliers from low-cost competition in the critical EU retro-fit segment.

For CEOs & Marketing Managers:

Differentiate your offering beyond price – focus on Total Cost of Ownership (TCO) tools that simulate energy savings from electric doors, reduced liability from anti-pinch systems, and extended maintenance intervals (smart doors with predictive alerts reduce roadside door failure by 61%, according to a 2025 Transport for London trial).

For Investors: Monitor the shift from “door as a component” to “door as a service” – three startups (not listed) are piloting subscription-based door maintenance contracts priced per bus per month, which could disrupt the traditional spare parts model.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

Global Info Research

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp