QY Research Inc. (Global Market Report Research Publisher) announces the release of 2025 latest report “Air Fryer Spray- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. Based on current situation and impact historical analysis (2020-2024) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Air Fryer Spray market, including market size, share, demand, industry development status, and forecasts for the next few years.

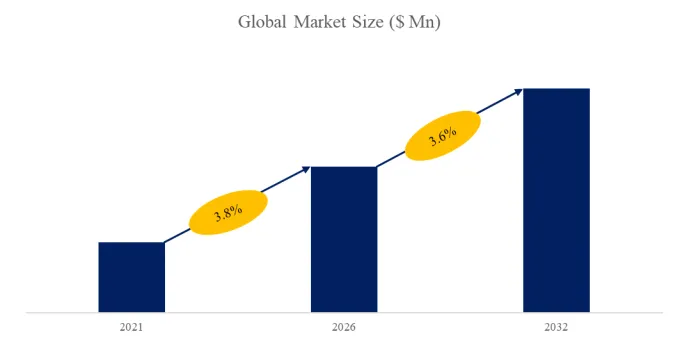

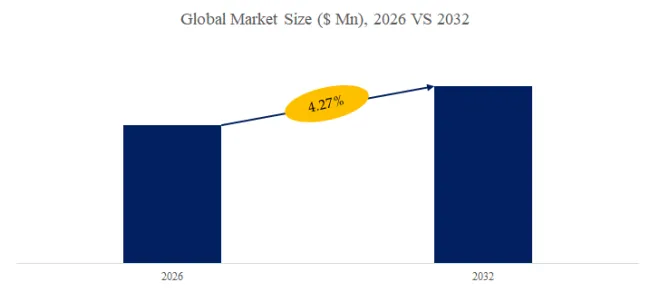

The global market for Air Fryer Spray was estimated to be worth US$ 143 million in 2025 and is projected to reach US$ 192 million, growing at a CAGR of 4.3% from 2026 to 2032.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/5543052/air-fryer-spray

Air Fryer Spray Market Summary

To address common problems in air fryer cooking, such as food drying out, sticking to the pan, and uneven oil distribution, specialized air fryer cooking sprays have emerged. As a core consumable for air fryers, these sprays utilize micro-atomizing nozzles to ensure even oil distribution, offering oil control, non-stick properties, and freshness preservation. They have developed into a category of kitchen consumables encompassing various types, including edible oil-based and functional compound sprays, widely used in home cooking, restaurant chains, and food processing.

According to the new market research report “Global Air Fryer Spray Market Report 2021-2032”, published by QYResearch, the global Air Fryer Spray market size is projected to reach USD 0.2 billion by 2032, at a CAGR of 4.3% during the forecast period.

Figure00001. Global Air Fryer Spray Market Size (US$ Million), 2026-2032

Above data is based on report from QYResearch: Global Air Fryer Spray Market Report 2021-2032 (published in 2025). If you need the latest data, plaese contact QYResearch.

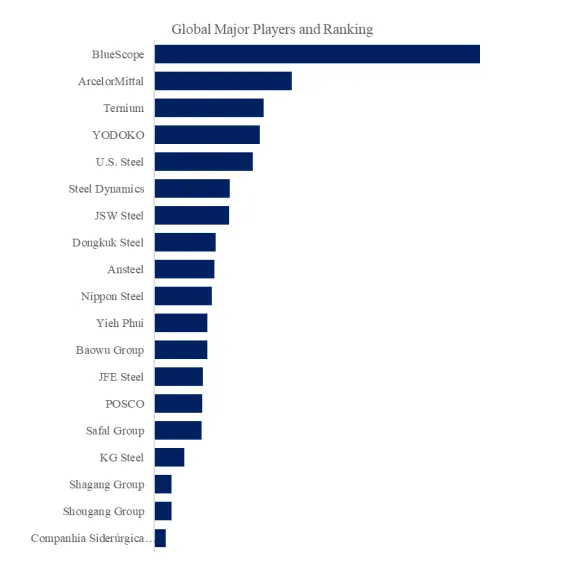

Figure00002. Global Air Fryer Spray Top 16 Players Ranking and Market Share (Ranking is based on the revenue of 2025, continually updated)

Above data is based on report from QYResearch: Global Air Fryer Spray Market Report 2021-2032 (published in 2025). If you need the latest data, plaese contact QYResearch.

Table 1. Air Fryer Spray Industry Chain Analysis

| Item | Description | |

| Upstream | Edible Vegetable Oils | Conductive Polypropylene is an antistatic polymer composite material based on a polypropylene (PP) matrix resin, modified through blending with conductive fillers, conductive carbon black, or polymeric conductive agents. While retaining the inherent advantages of polypropylene—such as light weight, impact resistance, corrosion resistance, and ease of molding—it endows the material with a stable surface resistivity, enabling it to dissipate static electricity and prevent static charge accumulation. It serves as the primary structural material for manufacturing ESD transport boxes, providing a secure physical and electrostatic protection environment for static-sensitive electronic components. |

| Food-Grade Emulsifiers | Food-grade emulsifiers are food additives that comply with national safety standards, enabling oils to mix uniformly and disperse stably with other auxiliary ingredients, thereby preventing separation, sedimentation, or coagulation. Their function is to enhance spray uniformity, extend product shelf-life, and improve atomization efficiency, ensuring that the resulting oil film is fine and thin—facilitating healthy, low-oil cooking—while remaining safe and harmless for human consumption. | |

| Downstream | Household Consumption | Air fryer spray is a popular accessory for healthy modern home cooking, specifically designed for use with air fryers, ovens, and frying pans. By delivering a thin, uniform mist of oil, it enables oil-free or low-oil cooking; it offers excellent non-stick properties, is convenient to use, and simplifies cleanup, thereby meeting the dietary health needs of households. It is widely used in daily culinary applications involving meat, fries, baked goods, and barbecued dishes. |

| Food Service Industry | In foodservice settings—such as fast-food outlets, Western-style restaurants, healthy-eating cafes, and tea shops—air fryer spray helps boost service efficiency, reduce oil consumption, and enhance the visual presentation of dishes. It is ideal for the batch preparation of roasted, fried, and baked items, helping to minimize cooking fumes and cleaning costs while aligning with the industry’s growing trends toward healthier, standardized, and highly efficient operations. | |

| Food Processing | In the industrial production of pre-prepared meals, frozen foods, and baked goods, air fryer spray serves as an efficient tool for non-stick coating and oil control. It allows for precise control over oil usage, enhances the consistency of product appearance and texture, and is compatible with automated production lines, thereby assisting food manufacturers in achieving their production goals regarding cost reduction, quality improvement, and regulatory compliance. |

Source: Secondary Sources, Press Releases, Expert Interviews and QYResearch, 2025

Table 2. Air Fryer Spray Industry Policy Analysis

| Policy | Description | |

| 1 | “National Food Safety Standard: Coatings and Coated Articles in Contact with Food” | This standard explicitly stipulates requirements regarding migration limits, heavy metal content, and the use of additives for coatings and coated articles intended for food contact. The coating materials used in air fryer sprays (e.g., coatings on metal or plastic components) must undergo migration testing for heavy metals—such as lead, cadmium, and arsenic—in accordance with the GB 31604 series of standards. Furthermore, they must pass corrosion resistance and abrasion resistance tests (e.g., 24-hour salt spray tests and 700-cycle abrasion tests) to ensure that no harmful substances are released during high-temperature cooking. |

| 2 | U.S. FDA | The US FDA mandates that all materials coming into direct or indirect contact with food must obtain food-contact safety certification. Consequently, the packaging materials for air fryer sprays (e.g., aluminum cans, plastic bottles) and the spray ingredients themselves (e.g., edible oil bases, emulsifiers) must comply with the definitions and migration limits for food additives outlined in 21 CFR Parts 174–178. |

| 3 | EU CE Certification | To be sold in the European Union market, air fryer spray products must obtain CE certification, which encompasses compliance with the Low Voltage Directive, the Electromagnetic Compatibility Directive, and the RoHS Directive. |

Source: Secondary Sources, Press Releases, Expert Interviews and QYResearch, 2025

Table 3. Air Fryer Spray Industry Development Trends

| Development Trends | Description | |

| 1 | Accelerated Health-Focused Upgrades: Organic and Low-Fat Options Become Mainstream | As consumer health awareness continues to rise, air fryer sprays are evolving toward low-fat, organic, and trans-fat-free formulations. Data from 2024 indicates that the market share of certified organic products is growing by 12% annually, while low-fat variants command a price premium of 30% to 50%. Precise oil-control technology—such as metered-dose spraying that dispenses approximately 1 gram per pump—has emerged as a core selling point, effectively meeting consumers’ strong demand for “healthy cooking with less oil.” |

| 2 | Integration of Multifunctional Features and Technological Innovation | Product functionality is evolving beyond simple oil control to incorporate integrated features—such as “seasoning-plus-non-stick” combinations, intelligent temperature control, and steam-assisted cooking—with a growth rate exceeding 50%. Advancements in electric atomization technology and the integration of AI-driven smart recipes enhance cooking precision, helping to prevent food from either burning or remaining undercooked. |

| 3 | Eco-Friendly Lightweighting and Packaging Innovation | The utilization rate of recyclable aluminum cans has risen to 68%, accompanied by an increased adoption of eco-friendly packaging materials (such as biodegradable plastics). These initiatives help reduce plastic pollution and align with the green, low-carbon trends mandated by “Dual Carbon” goals. The lightweight design reduces product weight and enhances portability, while simultaneously lowering production and transportation costs. |

Source: Secondary Sources, Press Releases, Expert Interviews and QYResearch, 2025

The report provides a detailed analysis of the market size, growth potential, and key trends for each segment. Through detailed analysis, industry players can identify profit opportunities, develop strategies for specific customer segments, and allocate resources effectively.

The Air Fryer Spray market is segmented as below:

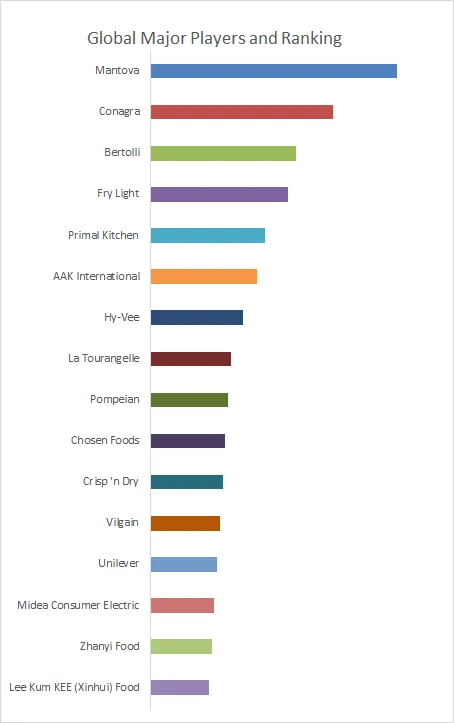

By Company

Mantova

Conagra

Bertolli

Fry Light

Primal Kitchen

AAK International

Hy-Vee

La Tourangelle

Pompeian

Chosen Foods

Crisp ‘n Dry

Vilgain

Unilever

Midea Home Appliances

Zhanyi Foods

Lee Kum Kee

Segment by Type

Vegetable Oil-Based

Animal Oil-Based

Segment by Application

Household Consumption

Catering Industry

Food Processing

Other

Each chapter of the report provides detailed information for readers to further understand the Air Fryer Spray market:

Chapter 1: Introduces the report scope of the Air Fryer Spray report, global total market size (valve, volume and price). This chapter also provides the market dynamics, latest developments of the market, the driving factors and restrictive factors of the market, the challenges and risks faced by manufacturers in the industry, and the analysis of relevant policies in the industry. (2021-2032)

Chapter 2: Detailed analysis of Air Fryer Spray manufacturers competitive landscape, price, sales and revenue market share, latest development plan, merger, and acquisition information, etc. (2021-2026)

Chapter 3: Provides the analysis of various Air Fryer Spray market segments by Type, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different market segments. (2021-2032)

Chapter 4: Provides the analysis of various market segments by Application, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different downstream markets.(2021-2032)

Chapter 5: Sales, revenue of Air Fryer Spray in regional level. It provides a quantitative analysis of the market size and development potential of each region and introduces the market development, future development prospects, market space, and market size of each country in the world..(2021-2032)

Chapter 6: Sales, revenue of Air Fryer Spray in country level. It provides sigmate data by Type, and by Application for each country/region.(2021-2032)

Chapter 7: Provides profiles of key players, introducing the basic situation of the main companies in the market in detail, including product sales, revenue, price, gross margin, product introduction, recent development, etc. (2021-2026)

Chapter 8: Analysis of industrial chain, including the upstream and downstream of the industry.

Chapter 9: Conclusion.

Benefits of purchasing QYResearch report:

Competitive Analysis: QYResearch provides in-depth Air Fryer Spray competitive analysis, including information on key company profiles, new entrants, acquisitions, mergers, large market shear, opportunities, and challenges. These analyses provide clients with a comprehensive understanding of market conditions and competitive dynamics, enabling them to develop effective market strategies and maintain their competitive edge.

Industry Analysis: QYResearch provides Air Fryer Spray comprehensive industry data and trend analysis, including raw material analysis, market application analysis, product type analysis, market demand analysis, market supply analysis, downstream market analysis, and supply chain analysis.

and trend analysis. These analyses help clients understand the direction of industry development and make informed business decisions.

Market Size: QYResearch provides Air Fryer Spray market size analysis, including capacity, production, sales, production value, price, cost, and profit analysis. This data helps clients understand market size and development potential, and is an important reference for business development.

Other relevant reports of QYResearch:

Global Air Fryer Spray Market Outlook, In‑Depth Analysis & Forecast to 2032

Global Air Fryer Spray Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

Global Air Fryer Spray Market Research Report 2026

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 19 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp