QY Research Inc. (Global Market Report Research Publisher) announces the release of 2025 latest report “Desktop Synthesizer- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. Based on current situation and impact historical analysis (2020-2024) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Desktop Synthesizer market, including market size, share, demand, industry development status, and forecasts for the next few years.

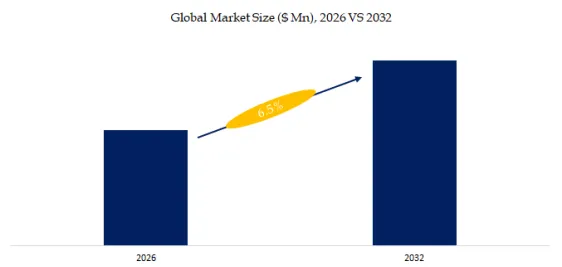

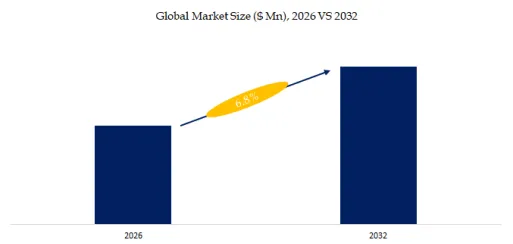

The global market for Desktop Synthesizer was estimated to be worth US$ 425 million in 2025 and is projected to reach US$ 679 million, growing at a CAGR of 6.8% from 2026 to 2032.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/5735030/desktop-synthesizer

Desktop Synthesizer Market Summary

A desktop synthesizer is a compact and self-contained electronic musical instrument designed for sound synthesis and music production. Unlike larger synthesizers that feature built-in keyboards, desktop synthesizers typically lack a keyboard and are intended to be controlled via external MIDI controllers, sequencers, or computer software. Desktop synthesizers often feature a wide range of sound synthesis capabilities, including analog, digital, or hybrid synthesis methods, allowing users to create a diverse array of sounds, from classic analog tones to modern digital textures. These synthesizers typically come in a compact desktop format, making them portable and space-saving, ideal for home studios, professional studios, live performances, and on-the-go music production setups. Desktop synthesizers may also include built-in sequencers, arpeggiators, effects processors, and modulation options, providing users with powerful tools for sound design, composition, and performance.

Currently, the desktop synthesizer market is in a phase of steady growth, driven by the expansion of home music production, the rise of independent creators, and the revival of analog sound preferences; it features a diverse product landscape spanning analog, digital, and hybrid models, catering to both professional and hobbyist users with varying budgets and functional needs.

According to the new market research report “Global Desktop Synthesizer Market Report 2026-2032″, published by QYResearch, the global market for Desktop Synthesizer was valued at US$ 425.00 million in the year 2025 and is projected to reach a revised size of US$ 679.4 million by 2032, growing at a CAGR of 6.8% during the forecast period 2026-2032.

Figure00002. Global Desktop Synthesizer Market Size (US$ Million), 2026 VS 2032

Above data is based on report from QYResearch: Global Desktop SynthesizerMarket Report 2026-2032(published in 2026). If you need the latest data, plaese contact QYResearch.

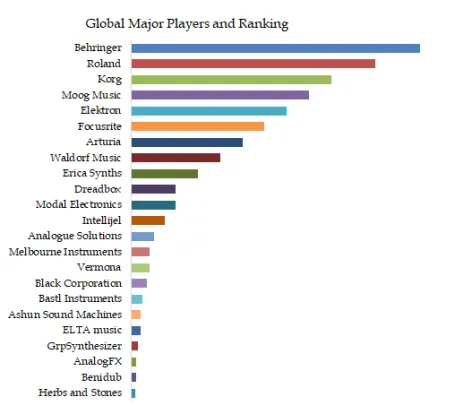

Figure00003. Global Desktop Synthesizer Top 23 Players Ranking and Market Share (Ranking is based on the revenue of 2025, continually updated)

Above data is based on report from QYResearch: Global Desktop SynthesizerMarket Report 2026-2032 (published in 2026). If you need the latest data, plaese contact QYResearch.

Figure00004. Desktop Synthesizer Industry Chain Analysis

Source: Secondary Sources, Press Releases, Expert Interviews and QYResearch, 2026、

Table 1. Desktop Synthesizer Industry Development Trends

|

Development Trends |

Description |

| 1 |

Hybrid architecture maturation |

Blending analog warmth with digital flexibility, such as combining analog oscillator circuits with digital wavetable synthesis and effects processing, becomes the dominant design philosophy, balancing tonal texture and functional versatility. |

| 2 |

AI creative assistance integration |

Deep incorporation of artificial intelligence into sound design, enabling AI-assisted patch generation, automatic harmonization, real-time performance analysis, and style migration, which transforms the synthesizer from a sound-generating tool into an intelligent creative partner. |

| 3 |

Software-hardware ecosystem linkage |

Strengthened integration with digital audio workstations (DAWs), virtual instrument libraries, and cloud-based sound banks, allowing for seamless data synchronization, remote parameter control, and the expansion of the device’s functionality through software updates. |

Source: Secondary Sources, Press Releases, Expert Interviews and QYResearch, 2026

Table 2. Desktop Synthesizer Industry Development Opportunities

|

Development Opportunities |

Description |

| 1 |

Booming home music creation |

The growing number of amateur producers, electronic music enthusiasts, and content creators creates sustained demand for entry-level and mid-range desktop synthesizers, lowering the creative threshold and expanding the user base. |

| 2 |

Expansion of professional scenarios |

Increasing application in film and television soundtrack production, live stage performance, sound design for advertising and media, and experimental art projects provides high-value market opportunities for high-end and professional-grade synthesizers. |

| 3 |

Hardware technology upgrading |

Improvements in core components like low-noise analog circuits, high-precision digital signal processing (DSP) chips, and low-power control modules reduce production costs and enhance the stability and performance of products, driving product iteration. |

Source: Secondary Sources, Press Releases, Expert Interviews and QYResearch, 2026

Table 3. Desktop Synthesizer Obstacles/Challenges to Industry Development

|

Obstacles/Challenges |

Description |

| 1 |

High technical barriers |

Profound expertise in analog circuit design, acoustic engineering, and digital signal processing is required to achieve excellent sound quality and stable performance, forming a high entry barrier for new entrants and increasing R&D costs for existing manufacturers. |

| 2 |

Severe market homogenization |

A large number of products with similar core functions and sound characteristics lead to fierce price competition, compressing profit margins and reducing the motivation for technological innovation among enterprises. |

| 3 |

Divergent user demands |

Balancing the pursuit of unique, professional sound quality by advanced users and the need for simplicity and ease of use by entry-level users is difficult, making it challenging for products to satisfy all user groups and achieve broad market penetration. |

Source: Secondary Sources, Press Releases, Expert Interviews and QYResearch, 2026

Future trends will center on deeper integration of AI for intelligent sound design and performance, tighter connectivity with DAWs and cloud ecosystems, and the evolution of hybrid architectures that blend analog warmth with digital flexibility, alongside more compact, user-friendly designs and expanded modular compatibility to unify fragmented hardware ecosystems.

The report provides a detailed analysis of the market size, growth potential, and key trends for each segment. Through detailed analysis, industry players can identify profit opportunities, develop strategies for specific customer segments, and allocate resources effectively.

The Desktop Synthesizer market is segmented as below:

By Company

Roland

Moog Music

Behringer

Korg

Elektron

Focusrite

Arturia

Erica Synths

Modal Electronics

Analogue Solutions

Vermona

AnalogFX

Black Corporation

Benidub

Bastl Instruments

Ashun Sound Machines

ELTA music

GrpSynthesizer

Intellijel

Herbs and Stones

Melbourne Instruments

Waldorf Music

Dreadbox

Segment by Type

Monophonic Synthesizer

Polyphonic Synthesizer

Segment by Application

Music Production Studio

Live Performance

Education and Learning

Home Studio

Others

Each chapter of the report provides detailed information for readers to further understand the Desktop Synthesizer market:

Chapter 1: Introduces the report scope of the Desktop Synthesizer report, global total market size (valve, volume and price). This chapter also provides the market dynamics, latest developments of the market, the driving factors and restrictive factors of the market, the challenges and risks faced by manufacturers in the industry, and the analysis of relevant policies in the industry. (2021-2032)

Chapter 2: Detailed analysis of Desktop Synthesizer manufacturers competitive landscape, price, sales and revenue market share, latest development plan, merger, and acquisition information, etc. (2021-2026)

Chapter 3: Provides the analysis of various Desktop Synthesizer market segments by Type, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different market segments. (2021-2032)

Chapter 4: Provides the analysis of various market segments by Application, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different downstream markets.(2021-2032)

Chapter 5: Sales, revenue of Desktop Synthesizer in regional level. It provides a quantitative analysis of the market size and development potential of each region and introduces the market development, future development prospects, market space, and market size of each country in the world..(2021-2032)

Chapter 6: Sales, revenue of Desktop Synthesizer in country level. It provides sigmate data by Type, and by Application for each country/region.(2021-2032)

Chapter 7: Provides profiles of key players, introducing the basic situation of the main companies in the market in detail, including product sales, revenue, price, gross margin, product introduction, recent development, etc. (2021-2026)

Chapter 8: Analysis of industrial chain, including the upstream and downstream of the industry.

Chapter 9: Conclusion.

Benefits of purchasing QYResearch report:

Competitive Analysis: QYResearch provides in-depth Desktop Synthesizer competitive analysis, including information on key company profiles, new entrants, acquisitions, mergers, large market shear, opportunities, and challenges. These analyses provide clients with a comprehensive understanding of market conditions and competitive dynamics, enabling them to develop effective market strategies and maintain their competitive edge.

Industry Analysis: QYResearch provides Desktop Synthesizer comprehensive industry data and trend analysis, including raw material analysis, market application analysis, product type analysis, market demand analysis, market supply analysis, downstream market analysis, and supply chain analysis.

and trend analysis. These analyses help clients understand the direction of industry development and make informed business decisions.

Market Size: QYResearch provides Desktop Synthesizer market size analysis, including capacity, production, sales, production value, price, cost, and profit analysis. This data helps clients understand market size and development potential, and is an important reference for business development.

Other relevant reports of QYResearch:

Global Desktop Synthesizer Market Outlook, In‑Depth Analysis & Forecast to 2032

Global Desktop Synthesizer Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

Global Desktop Synthesizer Market Research Report 2026

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 19 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

QY Research Inc. (Global Market Report Research Publisher) announces the release of 2025 latest report “Desktop Synthesizer- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. Based on current situation and impact historical analysis (2020-2024) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Desktop Synthesizer market, including market size, share, demand, industry development status, and forecasts for the next few years.

The global market for Desktop Synthesizer was estimated to be worth US$ 425 million in 2025 and is projected to reach US$ 679 million, growing at a CAGR of 6.8% from 2026 to 2032.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/5735030/desktop-synthesizer

Desktop Synthesizer Market Summary

A desktop synthesizer is a compact and self-contained electronic musical instrument designed for sound synthesis and music production. Unlike larger synthesizers that feature built-in keyboards, desktop synthesizers typically lack a keyboard and are intended to be controlled via external MIDI controllers, sequencers, or computer software. Desktop synthesizers often feature a wide range of sound synthesis capabilities, including analog, digital, or hybrid synthesis methods, allowing users to create a diverse array of sounds, from classic analog tones to modern digital textures. These synthesizers typically come in a compact desktop format, making them portable and space-saving, ideal for home studios, professional studios, live performances, and on-the-go music production setups. Desktop synthesizers may also include built-in sequencers, arpeggiators, effects processors, and modulation options, providing users with powerful tools for sound design, composition, and performance.

Currently, the desktop synthesizer market is in a phase of steady growth, driven by the expansion of home music production, the rise of independent creators, and the revival of analog sound preferences; it features a diverse product landscape spanning analog, digital, and hybrid models, catering to both professional and hobbyist users with varying budgets and functional needs.

According to the new market research report “Global Desktop Synthesizer Market Report 2026-2032″, published by QYResearch, the global market for Desktop Synthesizer was valued at US$ 425.00 million in the year 2025 and is projected to reach a revised size of US$ 679.4 million by 2032, growing at a CAGR of 6.8% during the forecast period 2026-2032.

Figure00002. Global Desktop Synthesizer Market Size (US$ Million), 2026 VS 2032

Above data is based on report from QYResearch: Global Desktop SynthesizerMarket Report 2026-2032(published in 2026). If you need the latest data, plaese contact QYResearch.

Figure00003. Global Desktop Synthesizer Top 23 Players Ranking and Market Share (Ranking is based on the revenue of 2025, continually updated)

Above data is based on report from QYResearch: Global Desktop SynthesizerMarket Report 2026-2032 (published in 2026). If you need the latest data, plaese contact QYResearch.

Figure00004. Desktop Synthesizer Industry Chain Analysis

Source: Secondary Sources, Press Releases, Expert Interviews and QYResearch, 2026、

Table 1. Desktop Synthesizer Industry Development Trends

|

Development Trends |

Description |

| 1 |

Hybrid architecture maturation |

Blending analog warmth with digital flexibility, such as combining analog oscillator circuits with digital wavetable synthesis and effects processing, becomes the dominant design philosophy, balancing tonal texture and functional versatility. |

| 2 |

AI creative assistance integration |

Deep incorporation of artificial intelligence into sound design, enabling AI-assisted patch generation, automatic harmonization, real-time performance analysis, and style migration, which transforms the synthesizer from a sound-generating tool into an intelligent creative partner. |

| 3 |

Software-hardware ecosystem linkage |

Strengthened integration with digital audio workstations (DAWs), virtual instrument libraries, and cloud-based sound banks, allowing for seamless data synchronization, remote parameter control, and the expansion of the device’s functionality through software updates. |

Source: Secondary Sources, Press Releases, Expert Interviews and QYResearch, 2026

Table 2. Desktop Synthesizer Industry Development Opportunities

|

Development Opportunities |

Description |

| 1 |

Booming home music creation |

The growing number of amateur producers, electronic music enthusiasts, and content creators creates sustained demand for entry-level and mid-range desktop synthesizers, lowering the creative threshold and expanding the user base. |

| 2 |

Expansion of professional scenarios |

Increasing application in film and television soundtrack production, live stage performance, sound design for advertising and media, and experimental art projects provides high-value market opportunities for high-end and professional-grade synthesizers. |

| 3 |

Hardware technology upgrading |

Improvements in core components like low-noise analog circuits, high-precision digital signal processing (DSP) chips, and low-power control modules reduce production costs and enhance the stability and performance of products, driving product iteration. |

Source: Secondary Sources, Press Releases, Expert Interviews and QYResearch, 2026

Table 3. Desktop Synthesizer Obstacles/Challenges to Industry Development

|

Obstacles/Challenges |

Description |

| 1 |

High technical barriers |

Profound expertise in analog circuit design, acoustic engineering, and digital signal processing is required to achieve excellent sound quality and stable performance, forming a high entry barrier for new entrants and increasing R&D costs for existing manufacturers. |

| 2 |

Severe market homogenization |

A large number of products with similar core functions and sound characteristics lead to fierce price competition, compressing profit margins and reducing the motivation for technological innovation among enterprises. |

| 3 |

Divergent user demands |

Balancing the pursuit of unique, professional sound quality by advanced users and the need for simplicity and ease of use by entry-level users is difficult, making it challenging for products to satisfy all user groups and achieve broad market penetration. |

Source: Secondary Sources, Press Releases, Expert Interviews and QYResearch, 2026

Future trends will center on deeper integration of AI for intelligent sound design and performance, tighter connectivity with DAWs and cloud ecosystems, and the evolution of hybrid architectures that blend analog warmth with digital flexibility, alongside more compact, user-friendly designs and expanded modular compatibility to unify fragmented hardware ecosystems.

The report provides a detailed analysis of the market size, growth potential, and key trends for each segment. Through detailed analysis, industry players can identify profit opportunities, develop strategies for specific customer segments, and allocate resources effectively.

The Desktop Synthesizer market is segmented as below:

By Company

Roland

Moog Music

Behringer

Korg

Elektron

Focusrite

Arturia

Erica Synths

Modal Electronics

Analogue Solutions

Vermona

AnalogFX

Black Corporation

Benidub

Bastl Instruments

Ashun Sound Machines

ELTA music

GrpSynthesizer

Intellijel

Herbs and Stones

Melbourne Instruments

Waldorf Music

Dreadbox

Segment by Type

Monophonic Synthesizer

Polyphonic Synthesizer

Segment by Application

Music Production Studio

Live Performance

Education and Learning

Home Studio

Others

Each chapter of the report provides detailed information for readers to further understand the Desktop Synthesizer market:

Chapter 1: Introduces the report scope of the Desktop Synthesizer report, global total market size (valve, volume and price). This chapter also provides the market dynamics, latest developments of the market, the driving factors and restrictive factors of the market, the challenges and risks faced by manufacturers in the industry, and the analysis of relevant policies in the industry. (2021-2032)

Chapter 2: Detailed analysis of Desktop Synthesizer manufacturers competitive landscape, price, sales and revenue market share, latest development plan, merger, and acquisition information, etc. (2021-2026)

Chapter 3: Provides the analysis of various Desktop Synthesizer market segments by Type, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different market segments. (2021-2032)

Chapter 4: Provides the analysis of various market segments by Application, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different downstream markets.(2021-2032)

Chapter 5: Sales, revenue of Desktop Synthesizer in regional level. It provides a quantitative analysis of the market size and development potential of each region and introduces the market development, future development prospects, market space, and market size of each country in the world..(2021-2032)

Chapter 6: Sales, revenue of Desktop Synthesizer in country level. It provides sigmate data by Type, and by Application for each country/region.(2021-2032)

Chapter 7: Provides profiles of key players, introducing the basic situation of the main companies in the market in detail, including product sales, revenue, price, gross margin, product introduction, recent development, etc. (2021-2026)

Chapter 8: Analysis of industrial chain, including the upstream and downstream of the industry.

Chapter 9: Conclusion.

Benefits of purchasing QYResearch report:

Competitive Analysis: QYResearch provides in-depth Desktop Synthesizer competitive analysis, including information on key company profiles, new entrants, acquisitions, mergers, large market shear, opportunities, and challenges. These analyses provide clients with a comprehensive understanding of market conditions and competitive dynamics, enabling them to develop effective market strategies and maintain their competitive edge.

Industry Analysis: QYResearch provides Desktop Synthesizer comprehensive industry data and trend analysis, including raw material analysis, market application analysis, product type analysis, market demand analysis, market supply analysis, downstream market analysis, and supply chain analysis.

and trend analysis. These analyses help clients understand the direction of industry development and make informed business decisions.

Market Size: QYResearch provides Desktop Synthesizer market size analysis, including capacity, production, sales, production value, price, cost, and profit analysis. This data helps clients understand market size and development potential, and is an important reference for business development.

Other relevant reports of QYResearch:

Global Desktop Synthesizer Market Outlook, In‑Depth Analysis & Forecast to 2032

Global Desktop Synthesizer Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

Global Desktop Synthesizer Market Research Report 2026

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 19 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp