QY Research Inc. (Global Market Report Research Publisher) announces the release of 2025 latest report “Rental Transparent LED Display- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. Based on current situation and impact historical analysis (2020-2024) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Rental Transparent LED Display market, including market size, share, demand, industry development status, and forecasts for the next few years.

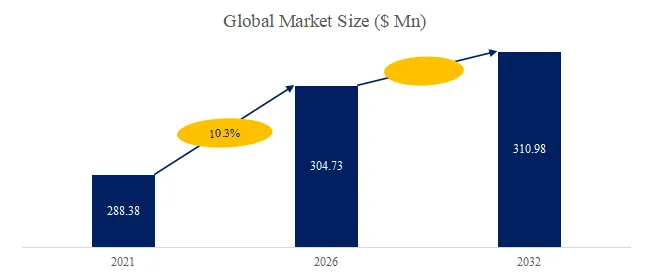

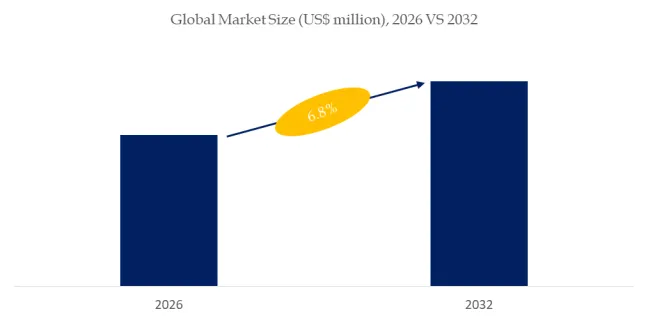

The global market for Rental Transparent LED Display was estimated to be worth US$ 178 million in 2025 and is projected to reach US$ 797 million, growing at a CAGR of 24.2% from 2026 to 2032.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/6069946/rental-transparent-led-display

Rental Transparent LED Display

The rental transparent LED display is an innovative display device that combines high transparency with flexible rental services. Its core feature is the use of hollow design or micro-LED technology, which enables dynamic content display while maintaining a 50%-90% transparency rate. It does not affect the lighting and visual transparency of the building, and can enhance the sense of technology and commercial value of the space through multimedia content. When using the rental model, users do not need to bear the cost of equipment procurement and maintenance. They can flexibly choose the screen size, resolution and special-shaped splicing solutions according to their needs, and enjoy the rapid installation, debugging and content adaptation services of a professional team. Technically, the product usually has high brightness, wide viewing angle, low power consumption and modular structure, supports seamless splicing and remote control, and can still maintain stable operation in complex environments. Some high-end models are also equipped with energy-saving cooling systems and waterproof functions, taking into account environmental protection and outdoor adaptability. With customized creative content, it can create an immersive visual experience that combines virtuality and reality for various scenes.

According to the latest QYResearch report, the global Rental Transparent LED Display market is expected to reach US$ 217.17 million in 2025, with a compound annual growth rate (CAGR) of 24.2%.

Manufacturing companies include Daktronics, Eager LED, Unilumin, Leyard, Dicolor LED, Gloshine Technology, Showtechled, Chenxiang Photoelectric, Meiyad Optoelectronics, Radiant Technology, Premteco, LCF LED, Guoxin Optoelectronics, Yuchip Electronic, SUNMAX Photoelectric Display.

|

Company Name

|

Description |

|

Daktronics

|

Daktronics is a world leader in the design, engineering, and manufacturing of digital LED display technology and audio systems. The company also installs and services reliable, long-lasting digital solutions—including scoreboards, video boards, message displays, and billboards—along with intuitive software used to control these systems.

|

|

Eager LED

|

Since its establishment in 2009, EagerLED has been engaged in indoor and outdoor LED displays, and has become one of the leaders in the field of LED displays. EagerLED attaches great importance to the research and development of LED products. After more than 10 years of development, EagerLED products sell well in more than 90 countries and regions around the world.

|

|

Unilumin

|

As a leading global provider of LED display and lighting products and optical solutions, Unilumin is a recipient of the National Science and Technology Progress Award (First Prize) and the Ministry of Industry and Information Technology’s Manufacturing Single Champion Award. It leads in LED display sales and shipment area, market share in rental displays, and market share in XR virtual photography. As a globally operating high-tech company, Unilumin has R&D centers in China, Japan, and the United States, a sales and service network covering more than 160 countries and regions worldwide, and the world’s largest intelligent manufacturing base for LED displays.

|

|

Leyard

|

Founded in 1995, Leyard Group has been maintaining high growth after being listed on the Shenzhen Stock Exchange. Display remains No.1 in global market share for five consecutive years. Leyard enjoys high brand awareness and reputation at home and abroad thanks to its involvement and professional service in many major events, including the Olympic Games, the World Expo, the NBA games, the German Bundestag (Federal Parliament), etc.Focusing on activities in the intelligent display, urban light environment, new cultural tourism business forms, and VR technology. |

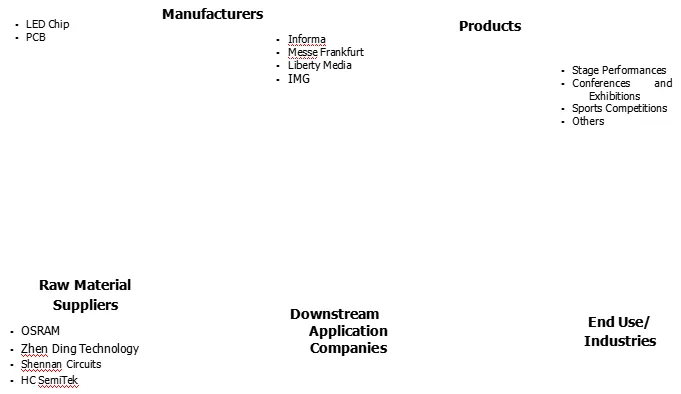

Figure00002. Rental Transparent LED Display Value Chain

Source: Secondary Sources, Expert Interviews and QYResearch, 2025

The upstream supply chain for rental transparent LED displays primarily includes suppliers of core raw materials and key components, such as LED chips, PCBs, driver ICs, module components, power supplies, and control systems. Representative domestic companies include San’an Optoelectronics, Lianchuang Electronics, and HC Semitek, while international companies include Samsung, Cree, Nichia, and Osram. Downstream applications encompass performance stages, commercial displays, expositions, advertising media, sporting events, and public events. Domestic clients include CCTV studios, major shopping malls, and exhibition centers, while international customers include Coachella, Times Square advertising screens, and international exhibition centers. This collaborative effort has driven the rapid adoption and widespread adoption of transparent LED displays for rental and temporary displays in diverse scenarios.

Market Drivers:

Demand for rental transparent LED displays is driven by the concert/exhibition economy, stagecraft upgrades, and experience-based branding. Live events (concerts, exhibitions, launches, sports, large commercial shows) increasingly require fast deployment, repeatable utilization, and high-impact visuals; transparent LEDs add depth and “see-through” aesthetics, enabling dynamic content without fully blocking lighting, set design, or sightlines. Rental use cases prioritize lightweight panels, quick-lock mechanics, front/rear serviceability, and high reliability—pushing continuous improvements in mechanical design, thermal management, and shock/vibration tolerance. Meanwhile, more mature content pipelines and real-time control (media servers, sync systems, XR/AR stages) raise the usability and ROI of transparent screens in complex productions.

Restraint:

Key restraints include the inherent trade-off between transparency and display performance, and the reliability/maintenance burden under rental duty cycles. Transparent LEDs often require compromises in pixel density, brightness/contrast, viewing angle, and black uniformity to preserve see-through characteristics; strong ambient light and long viewing distances place tougher demands on brightness and image quality. High turnover in rental operations increases damage risk, latch wear, and connector/power/receiver-card failures, raising requirements for mechanical robustness, EMC stability, and rapid repair. In addition, transparent screens are more sensitive to rigging safety, power/signal redundancy, and on-site calibration/color consistency; without standardized O&M, total cost of ownership rises and re-rental rates suffer.

Opportunity:

Opportunities lie in premium stage/immersive experiences, platformized products, and service-led delivery. As live productions pursue deeper immersion and spatial storytelling, transparent LEDs integrate well with lighting, kinetic stages, interactive installations, and XR/AR to create differentiated visual assets. Rental companies increasingly prefer modular, standardized platforms (common cabinets, swappable spares, unified control stacks) that maximize cross-project reuse—favoring manufacturers with scalable production and coherent product families. Moreover, integrated delivery models—hardware plus content support and full O&M (rigging engineering, calibration, backup units, rapid response)—are becoming decisive, enabling players with strong engineering execution and service footprints to capture higher value in premium projects.

Barriers to Entry:

Entry barriers are driven by engineering-grade mechanical/electro-optical integration, long-term reliability validation, and rental-channel delivery capability. Rental transparent LEDs must meet pixel/brightness/refresh/grayscale targets while balancing lightweight design with strength, ensuring latches, frames, and protection remain consistent across repeated assembly, transport, and impacts. Suppliers need rigorous incoming/production quality control, shock/vibration testing, EMC and safety compliance, and field-friendly replaceable modules/power/receiver systems to minimize downtime. Commercially, top rental houses and major production integrators prioritize proven references, execution quality, and aftersales responsiveness; new entrants must build credibility through project track records, spare-part systems, and service networks to enter core supply chains and achieve repeat purchases.

The report provides a detailed analysis of the market size, growth potential, and key trends for each segment. Through detailed analysis, industry players can identify profit opportunities, develop strategies for specific customer segments, and allocate resources effectively.

The Rental Transparent LED Display market is segmented as below:

By Company

Daktronics

Eager LED

Unilumin

Leyard

Dicolor LED

Gloshine Technology

Showtechled

Chenxiang Photoelectric

Meiyad Optoelectronics

Radiant Technology

Premteco

LCF LED

Guoxin Optoelectronics

Yuchip Electronic

SUNMAX Photoelectric Display

Segment by Type

Indoor Display

Outdoor Display

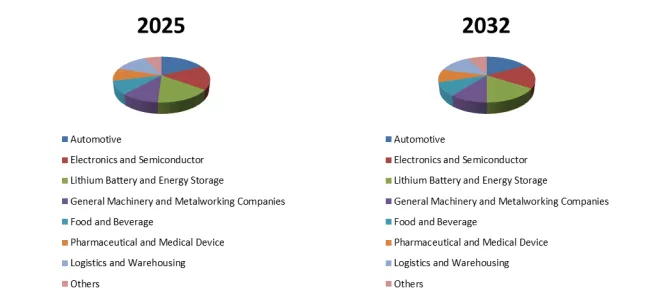

Segment by Application

Stage Performances

Conferences and Exhibitions

Sports Competitions

Others

Each chapter of the report provides detailed information for readers to further understand the Rental Transparent LED Display market:

Chapter 1: Introduces the report scope of the Rental Transparent LED Display report, global total market size (valve, volume and price). This chapter also provides the market dynamics, latest developments of the market, the driving factors and restrictive factors of the market, the challenges and risks faced by manufacturers in the industry, and the analysis of relevant policies in the industry. (2021-2032)

Chapter 2: Detailed analysis of Rental Transparent LED Display manufacturers competitive landscape, price, sales and revenue market share, latest development plan, merger, and acquisition information, etc. (2021-2026)

Chapter 3: Provides the analysis of various Rental Transparent LED Display market segments by Type, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different market segments. (2021-2032)

Chapter 4: Provides the analysis of various market segments by Application, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different downstream markets.(2021-2032)

Chapter 5: Sales, revenue of Rental Transparent LED Display in regional level. It provides a quantitative analysis of the market size and development potential of each region and introduces the market development, future development prospects, market space, and market size of each country in the world..(2021-2032)

Chapter 6: Sales, revenue of Rental Transparent LED Display in country level. It provides sigmate data by Type, and by Application for each country/region.(2021-2032)

Chapter 7: Provides profiles of key players, introducing the basic situation of the main companies in the market in detail, including product sales, revenue, price, gross margin, product introduction, recent development, etc. (2021-2026)

Chapter 8: Analysis of industrial chain, including the upstream and downstream of the industry.

Chapter 9: Conclusion.

Benefits of purchasing QYResearch report:

Competitive Analysis: QYResearch provides in-depth Rental Transparent LED Display competitive analysis, including information on key company profiles, new entrants, acquisitions, mergers, large market shear, opportunities, and challenges. These analyses provide clients with a comprehensive understanding of market conditions and competitive dynamics, enabling them to develop effective market strategies and maintain their competitive edge.

Industry Analysis: QYResearch provides Rental Transparent LED Display comprehensive industry data and trend analysis, including raw material analysis, market application analysis, product type analysis, market demand analysis, market supply analysis, downstream market analysis, and supply chain analysis.

and trend analysis. These analyses help clients understand the direction of industry development and make informed business decisions.

Market Size: QYResearch provides Rental Transparent LED Display market size analysis, including capacity, production, sales, production value, price, cost, and profit analysis. This data helps clients understand market size and development potential, and is an important reference for business development.

Other relevant reports of QYResearch:

Global Rental Transparent LED Display Market Outlook, In‑Depth Analysis & Forecast to 2032

Global Rental Transparent LED Display Market Research Report 2026

Global Rental Transparent LED Display Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 19 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp

2890.webp)