3D Printing Market Summary

3D printing is a process of creating three-dimensional objects using digital files. “3D printing” encompasses various processes that, under computer control, join or solidify materials to create three-dimensional objects, typically by adding materials layer by layer (e.g., fusing liquid molecules or powder particles together). This report focuses primarily on industrial-grade 3D printing equipment for industrial applications.

Source, EOS

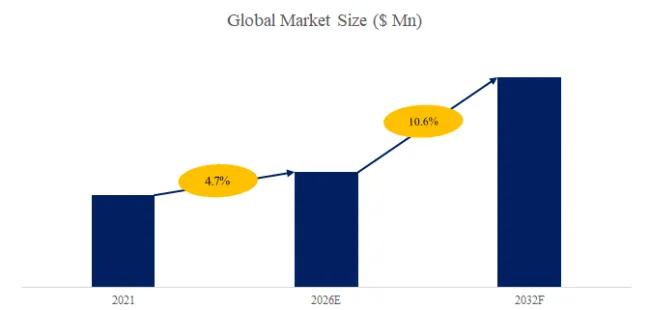

According to the new market research report “Global 3D Printing Market Report 2026-2032”, published by QYResearch, the global 3D Printing market size is projected to reach USD 3.41 billion by 2032, at a CAGR of 10.6% during the forecast period.

Figure00002. Global 3D Printing Market Size (US$ Million), 2021-2032

Above data is based on report from QYResearch: Global 3D Printing Market Report 2026-2032 (published in 2026). If you need the latest data, plaese contact QYResearch.

Supply Chain Collaboration: Building a Complete Ecosystem from Material Innovation to Application Scenario The 3D printing supply chain has formed a complete closed loop encompassing upstream materials and equipment, midstream printing services, and downstream application scenarios. Upstream, the focus is on core material and equipment R&D. The materials sector covers a diverse range of options, including metal powders, photosensitive resins, and bio-based materials. For example, titanium alloy powder achieves high-strength printing of aerospace components through micron-level particle size control. The equipment sector covers multi-level products from desktop to industrial to ultra-precision, with technological breakthroughs such as multi-laser heads and large-size molding chambers driving simultaneous improvements in printing efficiency and accuracy. Midstream is led by professional printing service providers, integrating the entire process of design, printing, and post-processing through digital platforms to provide “one-click ordering” cloud-based manufacturing services. For instance, a smart factory developed by one company can process thousands of orders simultaneously, covering all categories of needs from jewelry customization to automotive parts. Downstream application scenarios continue to expand, extending beyond traditional mold manufacturing to high-value-added fields such as medicine, construction, and energy. For example, bio-3D printing can construct human tissue models for drug testing, and concrete 3D printing technology enables rapid prototyping of building structures, forming an ecosystem of “materials-equipment-services-applications.” Policy Empowerment: National Strategy Guides High-Quality Development of the Industry Policy dividends inject strong momentum into the 3D printing industry. At the national level, additive manufacturing is listed as a key development area of ”Made in China 2025,” explicitly requiring breakthroughs in key technologies such as high-end printing equipment and core materials to promote the independent control of the industrial chain. For example, the Ministry of Industry and Information Technology, together with several other ministries, released the “Action Plan for the Development of Additive Manufacturing Industry (2023-2025),” proposing the goal of “achieving an independent rate of over 80% for key technologies by 2025,” and establishing a special fund to support enterprise R&D and innovation. The Ministry of Science and Technology, through the “14th Five-Year Plan” National Key R&D Program, focuses on tackling key technological challenges in high-end application scenarios such as aero-engine blades and medical implants. At the local level, Shanghai, Guangdong, Shandong, and other regions have introduced supporting policies, built 3D printing industrial parks, and provided support such as tax breaks and site subsidies to attract upstream and downstream enterprises to cluster and develop, forming a collaborative promotion pattern of “national guidance + local implementation.”

Trends and Opportunities: Technological Convergence and Upgraded Demand Drive Industry Transformation

The industry exhibits three major development trends: First, technological convergence: the deep integration of AI, robotics, and IoT technologies is driving 3D printing towards intelligent and automated upgrades. For example, AI algorithms can automatically optimize printing paths, reducing material waste; robotic arms integrated with print heads enable unmanned continuous production of large components. Second, high-end applications: extending from prototype manufacturing to end-product production, with explosive demand for customized, lightweight, and complex structural components in fields such as medical, aerospace, and automotive. For example, a car company uses 3D printing to produce engine brackets, reducing weight by 40% and outperforming traditional castings; a hospital uses 3D printing to customize orthopedic implants, achieving a perfect match with patients’ bones. Third, green sustainability: environmentally friendly solutions such as biodegradable materials and recyclable printing technologies are emerging. For example, a company developed PLA-recycled composite materials, which can reduce carbon emissions during the printing process by 30%, aligning with the global trend towards carbon neutrality. In terms of opportunities, the consumer market has huge potential, with continued growth in demand from education, cultural and creative industries, and personalized customization; the industrial market benefits from the transformation and upgrading of the manufacturing industry, especially the demand for flexible production from SMEs, opening up new blue ocean opportunities for 3D printing service providers. Challenges and Breakthroughs: From Technological Breakthroughs to Ecosystem Reconstruction The industry faces multiple challenges: Technologically, high-end equipment and materials still rely on imports; for example, the localization rate of key components in high-precision metal printing equipment is less than 50%. Cost-wise, industrial-grade printing materials are expensive, and post-processing is complex, resulting in end-product costs 2-3 times higher than traditional manufacturing. In terms of standards, the industry lacks a unified quality evaluation system, leading to significant performance differences in the same type of parts printed by different manufacturers, hindering large-scale application. The solution lies in differentiated competition and ecosystem collaboration: leading companies should focus on the high-end market, consolidating their barriers through technological iteration; SMEs should cultivate niche markets, such as developing specialized equipment and materials for dentistry and jewelry; and simultaneously strengthen industry-academia-research cooperation, promoting standard setting and testing platform construction. For example, an alliance, in conjunction with universities and enterprises, released the “Performance Testing Specification for Metal 3D Printed Parts,” providing quality references for the industry.

Entry Barriers: A Triple Test of Technology, Capital, and Ecosystem The 3D printing market faces high barriers to entry: Technological barriers require mastering core patents such as multiphysics simulation and precision control algorithms; for example, controlling the uniformity of the light spot in photopolymer printing requires long-term R&D investment. Capital barriers exist, with massive investments required for high-end equipment development and material production line construction; for instance, an industrial-grade metal printer can cost over ten million yuan, making it unaffordable for small and medium-sized enterprises. Ecosystem barriers require collaboration with CAD software and post-processing manufacturers to form a closed-loop ecosystem of “design-printing-post-processing.” Against this backdrop, new entrants must break through the barriers by differentiating themselves, such as focusing on the consumer desktop market or developing open-source software to lower the user barrier, in order to secure a place in the fiercely competitive market.

About The Authors

| Chengping Zhang | A experienced Technology & Market Analyst. Deep experience in chemical industry, focus on electronic materials, engineering materials and mineral resources, etc. Fully engaged in the development of technology and market reports as well as custom projects. | |

|

Senior Analyst |

||

| Email: zhangchengping@qyresearch.com |

Website: www.qyresearch.com Hot Line:4006068865

QYResearch focus on Market Survey and Research

US: +1-888-365-4458(US) +1-202-499-1434(Int’L)

EU: +44-808-111-0143(UK) +44-203-734-8135(EU)

Asia: +86-10-8294-5717(CN) +852-30628839(HK)

About QYResearch

QYResearch founded in California, USA in 2007.It is a leading global market research and consulting company. With over 17 years’ experience and professional research team in various cities over the world QY Research focuses on management consulting, database and seminar services, IPO consulting (data is widely cited in prospectuses, annual reports and presentations), industry chain research and customized research to help our clients in providing non-linear revenue model and make them successful. We are globally recognized for our expansive portfolio of services, good corporate citizenship, and our strong commitment to sustainability. Up to now, we have cooperated with more than 60,000 clients across five continents. Let’s work closely with you and build a bold and better future.

QYResearch is a world-renowned large-scale consulting company. The industry covers various high-tech industry chain market segments, spanning the semiconductor industry chain (semiconductor equipment and parts, semiconductor materials, ICs, Foundry, packaging and testing, discrete devices, sensors, optoelectronic devices), photovoltaic industry chain (equipment, cells, modules, auxiliary material brackets, inverters, power station terminals), new energy automobile industry chain (batteries and materials, auto parts, batteries, motors, electronic control, automotive semiconductors, etc.), communication industry chain (communication system equipment, terminal equipment, electronic components, RF front-end, optical modules, 4G/5G/6G, broadband, IoT, digital economy, AI), advanced materials industry Chain (metal materials, polymer materials, ceramic materials, nano materials, etc.), machinery manufacturing industry chain (CNC machine tools, construction machinery, electrical machinery, 3C automation, industrial robots, lasers, industrial control, drones), food, beverages and pharmaceuticals, medical equipment, agriculture, etc.

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 18 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp