Global Leading Market Research Publisher QYResearch announces the release of its latest report “Lactobacillus Acidophilus – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032″. Based on current situation and impact historical analysis (2021-2025) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Lactobacillus Acidophilus market, including market size, share, demand, industry development status, and forecasts for the next few years.

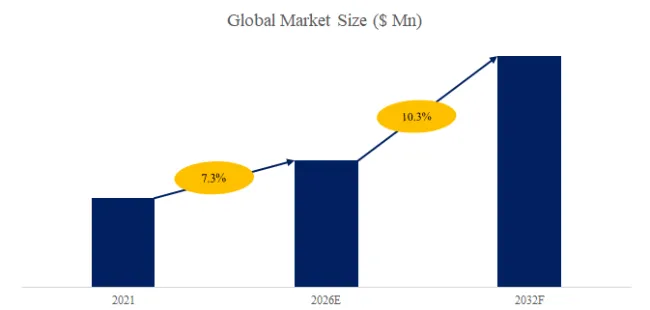

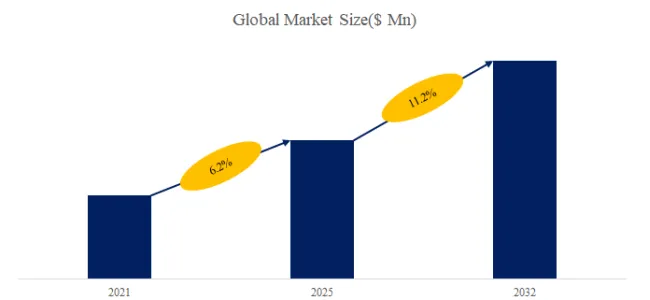

The global market for Lactobacillus Acidophilus was estimated to be worth US$ million in 2025 and is projected to reach US$ million, growing at a CAGR of % from 2026 to 2032. Lactobacillus acidophilus is one of the species of the genus Lactobacillus, which is a bacteria that exists naturally in the body, primarily in the intestines and the vagina. Morphologically, Lb. acidophilus bacteria are Gram-positive, non-spore-forming rods with rounded ends that occur singly, in pairs, and in short chains. The Lb. acidophilus group is fastidious organisms adapted to growth on complex organic substrates and contains mainly obligately homofermentative lactobacilli, but a few are facultative heterofermenters. The bacteriocins produced by the Lb. acidophilus group include lactocin B, lactacin F, acidocin A, and acidocin B. Lactobacillus acidophilus also has been used as a probiotic, or “friendly bacteria.” The health benefits associated with these strains include reduction of gastrointestinal symptoms in lactose-intolerant individuals, relief from symptoms of constipation, treatment of infantile diarrhea, prevention of travelers’ diarrhea, and activity against Helicobacter pylori.

Addressing Core Gut Health, Digestive Wellness, and Probiotic Supplementation Pain Points

Health-conscious consumers, dietary supplement manufacturers, functional food developers, and pharmaceutical companies face persistent challenges: digestive disorders (lactose intolerance, constipation, diarrhea) affect 30-40% of global population; gut microbiome imbalances are linked to immunity, mental health, and chronic disease; and consumers seek natural, clinically validated probiotics for digestive health. Lactobacillus acidophilus—a Gram-positive, non-spore-forming, homofermentative bacterium naturally present in human intestines and vagina—has emerged as one of the most studied and widely used probiotic strains. Health benefits include reduction of gastrointestinal symptoms in lactose-intolerant individuals (lactase activity), relief from constipation, treatment of infantile diarrhea, prevention of travelers’ diarrhea, and activity against Helicobacter pylori. Additionally, L. acidophilus produces bacteriocins (lactocin B, lactacin F, acidocin A, acidocin B) that inhibit pathogenic bacteria. However, product selection is complicated by two distinct formulations: single component (pure L. acidophilus strain) versus compound (multi-strain probiotic blends with other Lactobacillus, Bifidobacterium, or prebiotics). Over the past six months, new postbiotic research (non-viable bacterial metabolites), gut-brain axis studies, and functional food innovation have reshaped the competitive landscape.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)

https://www.qyresearch.com/reports/6015840/lactobacillus-acidophilus

Key Industry Keywords (Embedded Throughout)

- Lactobacillus acidophilus market

- Probiotic friendly bacteria

- Gut digestive health

- Single component compound

- Bacteriocin production

Market Landscape & Recent Data (Last 6 Months, Q4 2025–Q1 2026)

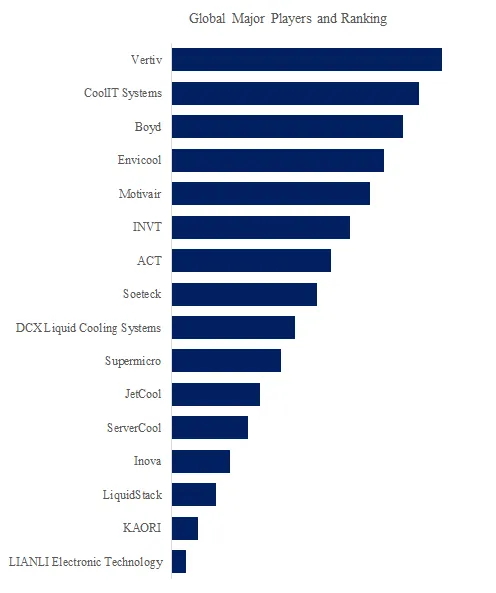

The global L. acidophilus market is fragmented, with a mix of global probiotic ingredient suppliers and regional/national manufacturers. Key players include DuPont (Danisco, US), Chr. Hansen (Denmark), Lallemand (Canada), DSM (Netherlands), Bio-K+ (Canada), ADM (US), China-Biotics (China), Jiangsu Wecare Biotechnology (China), Yiran Biology (China), Shandong Zhongke Jiayi Bioengineering (China), Shandong Xiangrikui (China), Probioway (China), Scitop (China), Lab4 probiotics (UK), and Probiotical (Italy).

Three recent developments are reshaping demand patterns:

- Postbiotic and paraprobiotic research: Postbiotics (non-viable bacterial metabolites, heat-killed cells) offer stability (longer shelf life, no cold chain) and safety (no live bacteria concerns). L. acidophilus postbiotics show similar anti-inflammatory and antimicrobial activity. Postbiotic segment grew 15-20% in 2025 (initial commercial launches).

- Gut-brain axis clinical evidence: L. acidophilus strains linked to reduced anxiety and depression symptoms (clinical trials, 2024-2025). Mental wellness probiotics (psychobiotics) gaining traction. Psychobiotic segment grew 10-12% in 2025.

- Functional food innovation: Fermented plant-based (oat, soy, coconut, almond) yogurts and kefirs using L. acidophilus (dairy-free probiotic). Plant-based probiotic segment grew 18% in 2025.

Technical Deep-Dive: Single Component vs. Compound Probiotics

- Single component (pure L. acidophilus strain) formulations contain only one strain (e.g., L. acidophilus La-14, NCFM, La-5). Advantages: strain-specific clinical evidence (dose-response studies), purity (no cross-strain competition), and easier for allergen labeling. A 2025 meta-analysis from the International Probiotics Association found that single-strain L. acidophilus (10^9-10^10 CFU/day) significantly reduced lactose intolerance symptoms (bloating, diarrhea) vs. placebo. Disadvantages: may be less effective for complex gut dysbiosis (requires multiple strains). Single component accounts for approximately 30-35% of L. acidophilus market volume, dominating clinical studies, pharmaceutical applications, and evidence-based supplements.

- Compound (multi-strain probiotic blends) combine L. acidophilus with other strains: L. rhamnosus, L. casei, L. plantarum, Bifidobacterium (B. lactis, B. longum, B. bifidum), and/or prebiotics (FOS, GOS, inulin). Advantages: synergistic effects (broader gut microbiome modulation), more effective for complex digestive issues (IBS, constipation, antibiotic-associated diarrhea), and consumer preference (comprehensive gut health). Disadvantages: strain interference possible, harder to attribute benefits to specific strain, and higher production cost (multiple fermentation, blending). Compound accounts for approximately 60-65% of volume, dominating dietary supplements, functional foods (yogurt, kefir), and consumer probiotics.

User case example: In November 2025, a European dietary supplement brand launched a compound probiotic (L. acidophilus + L. rhamnosus + B. lactis + FOS prebiotic) for daily gut health. The 12-month market study (completed Q1 2026) showed:

- Sales volume: 2 million units/year (capsules, powder sticks).

- Consumer survey (n=5,000): 85% reported improved digestion (less bloating, regular bowel movements).

- Price: $25/month supply (compound) vs. $15 for single-strain L. acidophilus (67% premium).

- Repeat purchase rate: 45% (vs. industry average 30-35% for probiotics).

- Decision: Compound probiotics with L. acidophilus as anchor strain; single-strain for targeted indications (lactose intolerance, H. pylori).

Industry Segmentation: Discrete vs. Continuous Manufacturing

- L. acidophilus manufacturing (fermentation (anaerobic, 37°C, MRS broth), cell harvesting (centrifugation), freeze-drying or spray-drying, blending (for compound), packaging) follows batch fermentation (discrete manufacturing). Production volumes: metric tons to hundreds of metric tons annually.

- CFU enumeration and stability testing (viable cell count at batch release and throughout shelf life) is QC/analytical.

Exclusive observation: Based on analysis of early 2026 product launches, a new “L. acidophilus spore-forming probiotic” is emerging (Bacillus coagulans, not true L. acidophilus but marketed similarly). Spore-forming probiotics survive stomach acid (higher viability, no enteric coating), ambient shelf life (no refrigeration), and higher heat tolerance (suitable for baked goods, hot beverages). True L. acidophilus is non-spore-forming (sensitive to heat, acid, requires refrigeration for some products). Spore-forming probiotics command 30-50% price premiums and are gaining share in functional foods (probiotic granola, chocolate, coffee).

Application Segmentation: Food & Beverage, Drugs, Dietary Supplements, Others

- Food & Beverage (fermented dairy (yogurt, kefir, buttermilk), non-dairy (plant-based yogurt, kefir), fermented vegetables (sauerkraut, kimchi), juice, chocolate) accounts for approximately 45-50% of L. acidophilus market volume (largest segment). Fastest-growing segment (8-10% CAGR), driven by functional food innovation (plant-based, probiotic snacks).

- Dietary Supplements (capsules, tablets, powder sticks, gummies, liquids) accounts for 35-40% of volume. Compound probiotics dominate; single-strain for targeted indications.

- Drugs (pharmaceutical-grade probiotics for specific indications: antibiotic-associated diarrhea, C. difficile infection, H. pylori eradication) accounts for 10-15% of volume (higher ASP, regulatory approval required).

- Others (animal feed, aquaculture, agriculture) accounts for 5-10% of volume.

Strategic Outlook & Recommendations

The global Lactobacillus acidophilus market is projected to reach US$ million by 2032, growing at a CAGR of %.

- Dietary supplement and functional food manufacturers: L. acidophilus should be anchor strain in compound probiotics (broad digestive health). Single-strain for targeted indications (lactose intolerance, H. pylori). Postbiotics (heat-killed, non-viable) for shelf-stable products (no refrigeration). Spore-forming probiotics for high-heat applications (baked goods, hot beverages).

- Consumers: L. acidophilus (10^9-10^10 CFU/day) effective for lactose intolerance, constipation, diarrhea (travelers’, infantile). Compound probiotics (multi-strain + prebiotics) for comprehensive gut health. Refrigerated vs. ambient shelf life depends on formulation (freeze-dried stable at room temperature).

- Regulators: EFSA (EU) and FDA (US) have not approved specific health claims for L. acidophilus (except general gut health). Structure/function claims allowed. Pharmaceutical-grade probiotics require clinical trial evidence.

- Manufacturers (DuPont, Chr. Hansen, Lallemand, DSM, ADM): Invest in strain-specific clinical evidence (lactose intolerance, H. pylori), postbiotic development (stability, safety), and spore-forming probiotic technologies. Microencapsulation for acid/bile tolerance.

For digestive and gut health, Lactobacillus acidophilus is a clinically validated probiotic (“friendly bacteria”) with benefits for lactose intolerance, constipation, diarrhea, and H. pylori activity. Compound probiotics (multi-strain + prebiotics) dominate dietary supplements; single-strain serves targeted indications. Food & beverage and dietary supplements are primary growth drivers.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp