Global Leading Market Research Publisher QYResearch announces the release of its latest report “Cholesterol Drug – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032″. Based on current situation and impact historical analysis (2021-2025) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Cholesterol Drug market, including market size, share, demand, industry development status, and forecasts for the next few years.

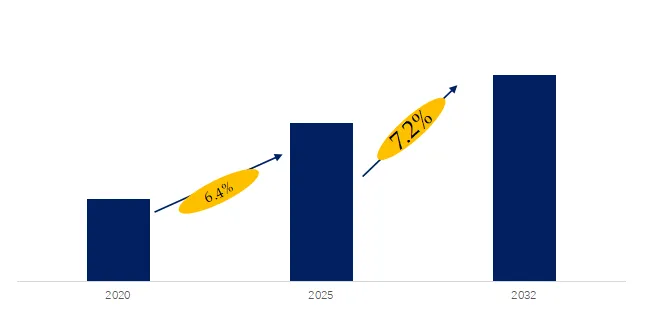

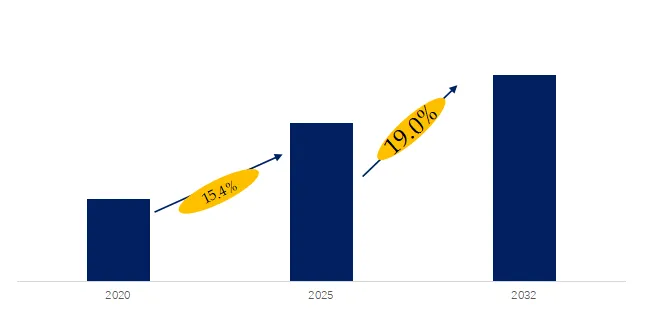

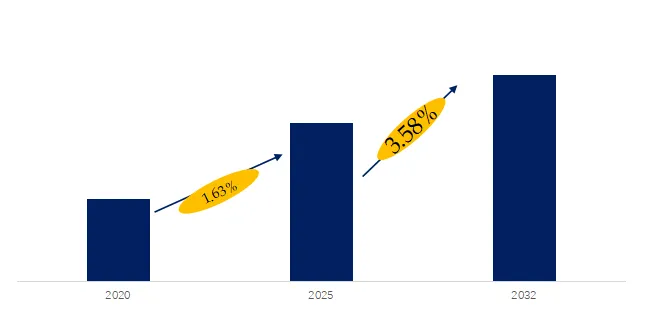

The global market for Cholesterol Drug was estimated to be worth US$ million in 2025 and is projected to reach US$ million, growing at a CAGR of % from 2026 to 2032. Cholesterol Drugs are a class of prescription medicines and biologics designed to reduce the risk of atherosclerotic cardiovascular events. They operate through multiple mechanisms — including inhibition of synthesis, inhibition of absorption, enhancement of receptor-mediated metabolism, and modulation of the hepatic PCSK9 axis — to establish a framework for long-term therapeutic management. Their clinical value lies not only in the degree of LDL-C reduction but also in the redistribution of risk across different patient stratifications, particularly among those with statin intolerance or a history of cardiovascular events. In recent years, regulatory labeling and commercial rights have been continuously restructured — such as regional asset transfers of legacy statins and the label expansion of PCSK9 inhibitors and fixed-dose combinations — collectively driving a shift from single-mechanism pharmacology to stratified combination therapy and sustained treatment adherence.

Opportunities and Drivers: How Do Demand-Side and Technology-Side Forces Resonate to Unlock the Growth Curve of “Long-Term Therapy + Combination Treatment”? In secondary cardiovascular prevention and high-risk frontline intervention, the combination of intensive lipid lowering and early co-therapy has become a clinical consensus, accelerating the adoption of fixed-dose statin–ezetimibe combinations and PCSK9 pathway drugs. The U.S. FDA and European EMA continue to refine labeling and indications for both combination products and PCSK9 monoclonal antibodies, providing greater regulatory certainty for accessibility and compliance. At the enterprise level, redistribution of rights and supply capacity—such as AstraZeneca transferring CRESTOR rights in most European countries to Grünenthal, and the regional operational split of Sanofi/Regeneron’s Praluent—has improved market efficiency for established assets. The key challenge lies in global supply resilience and affordability: from Praluent’s temporary supply suspension in China to the U.S. initiatives for direct-to-patient pricing and new distribution models for PCSK9 inhibitors, companies must strike a balance among capacity, channels, and pricing structures.

Industry Chain / Supply Chain: From API to Clinical End Use—Who Bears the Pressure and Who Fills the Gap? At the upstream level, integration of API and formulation production remains vital to maintaining stable long-term supply of generic statins. Teva’s TAPI division continues to provide robust API supply capacity, forming the backbone for multi-market formulation expansion. In the midstream segment, formulation and combination platforms operate on a global, regionally segmented basis: Viatris manages legacy brands such as Lipitor along with a wide portfolio of generic statins; Sun Pharma has positioned Rosuvastatin and patient-adapted sprinkle formulations (Ezallor Sprinkle) in the U.S. and other markets; while in China, state-owned pharmaceutical platforms—such as Shanghai Modern Pharmaceutical under China National Pharmaceutical Group—support localized production of agents like Pravastatin. Downstream, PCSK9 monoclonal antibodies (e.g., Amgen’s Repatha) and statin–ezetimibe combinations (e.g., ROSZET) are progressively filling therapeutic gaps for high-risk or goal-unmet patient populations.

Market Segmentation Trends: Which Clinical Scenarios Are Emerging as the “Acceleration Lanes”? Statin-intolerant or suboptimally controlled patients represent the main entry point for both innovation and combination therapies. The expanding indications of PCSK9 monoclonal antibodies in patients with prior cardiovascular events or extremely high risk further reinforce their role in secondary prevention. Meanwhile, fixed-dose combinations (statin + ezetimibe) are accelerating their adoption in long-term management from “intensification to maintenance” due to simplified therapy and better adherence. Patient-friendly formulations—such as sprinkle capsules for those with swallowing difficulties or elderly populations—enhance treatment accessibility, while compliance-based direct-to-patient distribution models reduce access barriers for high-value biologics, supporting long-term follow-up and prescription continuity.

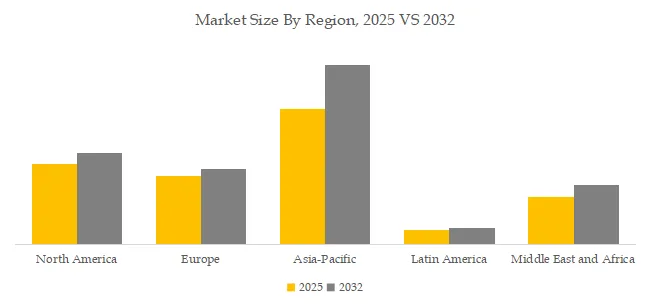

Regional Trends: How Will the “Multi-Center Evolution” of Regulation, Access, and Commercial Rights Progress? In North America, label expansion and innovative commercial models proceed in parallel—e.g., Repatha’s new indication for high-risk adults and significant price reductions via direct sales—prompting subtle shifts in prescription structures as affordability and access improve. In Europe, the asset restructuring of legacy statins (such as AstraZeneca’s transfer of CRESTOR rights to Grünenthal in most European markets) has led to renewed distribution and packaging arrangements. Across China and the broader Asia-Pacific, national reimbursement programs and volume-based procurement policies emphasize “clinical value plus affordability,” while temporary supply constraints of imported biologics have driven closer coordination between domestic and imported channels. Overall, regional diversity in regulatory timing, commercial ownership, and production capacity deployment is shaping a differentiated and layered competitive landscape. Latest Developments October 6, 2025 (U.S.) – Amgen announced a >60% price reduction for Repatha through its AmgenNow direct-sales channel, in collaboration with retail partners, aiming to enhance PCSK9 inhibitor accessibility and patient adherence; August 25, 2025 (U.S.) – The FDA expanded Repatha’s indication to include adults with uncontrolled LDL-C and elevated risk of major cardiovascular events, reinforcing its positioning in high-risk populations; August 12, 2025 (China) – Sanofi disclosed a temporary suspension of Praluent (alirocumab) supply to the Chinese market due to global shortages; the company announced expansion investments and coordination with healthcare institutions to ensure treatment continuity through alternative options.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)

https://www.qyresearch.com/reports/6017889/cholesterol-drug

Key Industry Keywords (Embedded Throughout)

- Cholesterol drug market

- Statins PCSK9 inhibitors

- LDL-C reduction therapy

- Statin intolerance treatment

- Fixed-dose combination

Market Landscape & Recent Data (Last 6 Months, Q4 2025–Q1 2026)

The global cholesterol drug market is concentrated among major pharmaceutical companies with cardiovascular franchises. Key players include AstraZeneca (CRESTOR/rosuvastatin), Amgen (Repatha/evolocumab), Sanofi (Praluent/alirocumab), Sun Pharma (Ezallor Sprinkle/rosuvastatin), Viatris (Lipitor/atorvastatin, generic statins), TEVA (generic statins, API via TAPI division), China National Pharmaceutical Group (pravastatin, localized production), and PKU Healthcare (China).

Three recent developments are reshaping treatment paradigms:

- Amgen Repatha price reduction >60% via AmgenNow (Oct 6, 2025) : Direct-sales channel collaboration with retail partners to enhance PCSK9 inhibitor accessibility and patient adherence.

- FDA expanded Repatha indication (Aug 25, 2025) : Adults with uncontrolled LDL-C and elevated risk of major cardiovascular events, reinforcing high-risk population positioning.

- Sanofi Praluent temporary supply suspension in China (Aug 12, 2025) : Global shortages; expansion investments and coordination with healthcare institutions for alternative treatment continuity.

Strategic Outlook & Recommendations

- Statins (atorvastatin, rosuvastatin, simvastatin, pravastatin, lovastatin, fluvastatin, pitavastatin) : First-line LDL-C reduction therapy. Generic statins (Viatris, Teva) dominate. High-intensity statins for secondary prevention (LDL-C <70 mg/dL, <55 mg/dL for very high risk). Statin intolerance (muscle pain, elevated liver enzymes) → ezetimibe or PCSK9 inhibitors.

- PCSK9 inhibitors (evolocumab/Repatha, alirocumab/Praluent) : Monoclonal antibodies for statin-intolerant or suboptimally controlled patients (familial hypercholesterolemia, established CVD). FDA expanded indication (high-risk adults, uncontrolled LDL-C). Amgen Repatha price reduction >60% (AmgenNow direct-sales).

- Fixed-dose combinations (statin + ezetimibe, ROSZET, CRESTOR + ezetimibe) : Simplified therapy, improved adherence. Long-term management from intensification to maintenance.

- Selective Cholesterol Absorption Inhibitors (ezetimibe) : Add-on to statin or monotherapy for statin-intolerant.

- Resins (bile acid sequestrants: cholestyramine, colestipol, colesevelam) : Second-line.

- Key players: AstraZeneca, Amgen, Sanofi, Sun Pharma, Viatris, Teva, China National Pharmaceutical Group, PKU Healthcare.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp