Robotic Collision Sensor Market Summary

Robot collision sensor is an important safety component of robot, which is used to detect whether accidental contact or collision occurs between robot and surrounding environment or object in real time, to trigger emergency stop or adjust motion trajectory to protect the safety of people, robot itself and peripheral equipment.

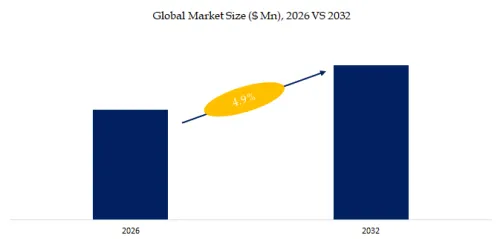

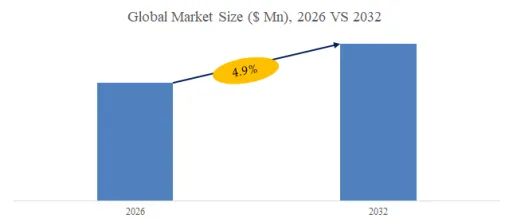

According to the new market research report “Global Robotic Collision Sensor Market Report 2026-2032″, published by QYResearch, the global Robotic Collision Sensor market size is projected to grow from USD 61.44 million in 2025 to USD 140 million by 2032, at a CAGR of 12.5% during the forecast period.

Above data is based on report from QYResearch: Global Robotic Collision Sensor Market Report 2026-2032(published in 2026). If you need the latest data, plaese contact QYResearch.

Table. Global Robotic Collision Sensor Main Manufacturers

| Headquarter | Company | Business Introduction |

| USA | ATI Industrial Automation | ATI Industrial Automation is a manufacturer of robotic automation equipment, specializing in engineering, research and development, and production of robot end effectors and robot accessories. The company’s main products include robot tool changers, multi-axis force/torque sensors, robot collision sensors, compliance devices, material removal tools, and couplers, which are widely used in industrial robots, collaborative robots, medical robots, and automated assembly, grinding, and inspection applications.

ATI’s core competitiveness lies in its high-precision force sensing and robot end effector technologies, and its products have been widely adopted in global manufacturing automation systems. |

| USA | RAD | RAD is a manufacturer of robotic automation attachments and is considered one of the early inventors of robot collision sensor technology. The company primarily designs and manufactures robot end effector attachments, including robot collision sensors, compliance devices, deburring tools, robot grippers, and tool changers. Its core product, the Ultimatic™ collision sensor series, mechanically detects robot contact with obstacles and sends a stop signal to the control system to protect the robot and tooling. |

| USA | AGI | AGI Automation is an industrial automation component manufacturer specializing in the design and production of pneumatic automation components and robot end effectors. The company’s products include pneumatic grippers, linear and rotary actuators, robot tool changers, feeding mechanisms, overload protection and collision sensors, and other automated assembly equipment components, widely used in manufacturing processes such as assembly, handling, packaging, loading/unloading, and parts transfer.

AGI focuses on pneumatic gripping and automated assembly mechanisms as its core technologies and is a professional manufacturer of industrial robot accessories and assembly automation components. |

| Sweden | Robot System | Robot System Products AB (RSP) is a manufacturer of robot accessories and automation components, specializing in the research and development and production of robot end effector interfaces and safety devices. The company’s main products include robot collision sensors, tool changers, electrical and fluid connection modules, and robot mounting and protection components, which are widely used in automotive manufacturing, welding, assembly, and industrial automation production lines. RSP’s core business focuses on modular robot interfaces and collision protection technology. |

| German | SCHUNK | SCHUNK is an industrial automation and gripping technology manufacturer and one of the world’s leading suppliers of gripping systems and robot end effectors. The company’s main products include mechanical and electric grippers, machine tool chucks, tool clamping systems, robot automation modules, and collaborative robot grasping solutions, widely used in machine tooling, automotive manufacturing, electronics assembly, and industrial robot automation. SCHUNK’s core competitiveness lies in its high-precision gripping and modular automation technologies. |

| Italy | EFFECTO GROUP | EFFECTO GROUP is an industrial automation equipment manufacturer specializing in the research and development and production of robot end effectors and workpiece clamping solutions. Through its brands, the company offers pneumatic and electric grippers, tool changers, robot collision sensors, compliance devices, deburring tools, self-centering vises, and clamping systems, which are widely used in the automotive, aerospace, machine tool, medical, food, and general manufacturing automation industries.

EFFECTO GROUP positions itself as a supplier of industrial robot end effectors and automated clamping technologies, serving global automated production lines and robot system integration applications. |

| Denmark | OnRobot | OnRobot is a manufacturer of robot end effectors, formed by the consolidation of several robot accessory companies. The company focuses on providing plug-and-play automation solutions for collaborative and industrial robots.

OnRobot’s main products include electric and adaptive grippers, vacuum grippers, force/torque sensors, vision systems, grinding and screw fastening tools, etc., supporting major robot platforms such as UR, ABB, FANUC, and KUKA. These products are widely used in automation scenarios such as assembly, handling, packaging, machine tool loading and unloading, and quality inspection. The company positions itself as a general-purpose end effector supplier within the collaborative robot ecosystem. |

| Switzerland | Bota Systems | Bota Systems AG is a robotic sensor technology company specializing in the research and development and production of multi-axis force/torque sensors and robot force control solutions. The company’s main products include six-dimensional force/torque sensors, robot end-effector force control modules, and software interfaces, used for force feedback control in applications such as precision assembly, grinding, polishing, and human-robot collaboration. Bota Systems’ sensors are characterized by compact design, high sampling rates, and ease of integration, supporting robot platforms such as UR, Franka, and KUKA, serving the fields of industrial automation and robotics research. |

| German | SICK AG | SICK AG is an industrial sensor and automation solutions manufacturer and one of the world’s leading suppliers of industrial sensing and machine vision technologies. The company’s main products include photoelectric sensors, laser scanners, machine vision systems, industrial safety sensors, encoders, and gas analyzers, which are widely used in industrial automation, logistics and warehousing, automotive manufacturing, process control, and robot safety systems. SICK possesses strong technological expertise and global market influence in industrial safety and intelligent sensing technologies. |

| German | Pepperl+Fuchs | Pepperl+Fuchs is a manufacturer of industrial sensing and explosion-proof automation equipment, and one of the world’s leading suppliers of industrial sensors and intrinsically safe explosion-proof technologies. The company’s business is primarily divided into two segments: industrial sensors (such as proximity sensors, photoelectric sensors, encoders, and RFID systems) and process automation and explosion-proof equipment. Its products are widely used in factory automation, logistics, petrochemicals, power generation, and hazardous environments. Pepperl+Fuchs’ core competitiveness lies in industrial sensing and intrinsic safety technologies. |

| China | Duco Robot | Duco Robot is a manufacturer of collaborative and desktop robots, specializing in the research and development and production of lightweight industrial robots, collaborative robots, and educational robots. The company’s main products include desktop robotic arms, collaborative robots, SCARA robots, and automated workstation solutions, widely used in electronic assembly, 3C manufacturing, scientific research and education, medical, and light industrial automation. Duco Robot’s core market positioning is based on miniaturized, easy-to-program, and cost-effective robot products. |

Above data is based on report from QYResearch: Global Robotic Collision Sensor Market Report 2026-2032 (published in 2026). If you need the latest data, plaese contact QYResearch.

Robot Collision Sensor Supply Chain Analysis:

Upstream: Primarily includes suppliers of core components such as force/torque sensing chips, MEMS accelerometers, strain gauges, piezoelectric elements, elastomer structural components, signal processing ICs, and connectors.

Midstream: Manufacturers of collision sensors and safety monitoring modules (such as six-dimensional force sensor manufacturers, robot safety system manufacturers, and end effector sensor manufacturers), responsible for structural design, calibration, algorithms, and safety certification.

Downstream: Industrial robot manufacturers, collaborative robot manufacturers, and automation system integrators, ultimately applying these technologies in automotive manufacturing, electronic assembly, logistics automation, service robots, and human-robot collaboration scenarios.

Overall, the technological barriers in this industry chain are concentrated in high-precision force sensing, real-time signal processing algorithms, safety function certification, and robot control system integration capabilities, belonging to the core functional sensor sub-sector of robots.

Key Drivers:

The core driving force behind the growth of the robot collision sensor market stems firstly from the global wave of industrial automation upgrades. The deepening of smart manufacturing and Industry 4.0 has led to the continuous expansion of robot applications in industries such as automotive, electronics, and food processing, directly driving the rigid demand for safety sensing components. Simultaneously, the rise of human-robot collaboration has become a key driving force. In the new production model where humans and robots share workspaces, higher demands are placed on real-time and accurate collision avoidance protection, prompting sensor technology to develop towards higher sensitivity and faster response speeds. Technological progress and innovation are the internal engines. Continuous breakthroughs in technologies such as LiDAR, multi-sensor fusion, and AI algorithm optimization have significantly improved the accuracy, reliability, and intelligence level of sensors, while continuously reducing their costs, gradually lowering the application threshold. Strong policy support provides a favorable development environment for the market. Governments around the world have introduced plans and financial support policies to encourage the development of robots and core components in order to promote the intelligent transformation and upgrading of industries. The rapid expansion of downstream application scenarios has brought new growth poles, extending from traditional industrial fields to emerging fields such as service robots, special robots, healthcare, and even humanoid robots. These complex scenarios place diversified and demanding requirements on collision perception. Finally, the rapid increase in the localization rate of sensors is also an undeniable driving force. Domestic enterprises have made significant progress in technological research and development, with some products reaching international advanced levels. Driven by both market demand and national strategy, the process of domestic substitution has accelerated, injecting new vitality into the market.

Main Obstacles:

The primary obstacle facing robot collision sensors lies in their technological maturity and complexity. Achieving high precision and high reliability still requires overcoming many challenges, especially in complex and dynamic real-world industrial scenarios filled with electromagnetic interference. The issues of false alarm rate, response delay, and long-term stability of sensors have not yet been perfectly resolved. Cost pressure is another prevalent constraint. The research and development and production costs of high-performance sensors are high, and their price still constitutes a significant investment threshold for many small and medium-sized manufacturing enterprises, especially in applications pursuing ultimate cost-effectiveness, where customers are extremely price-sensitive. The highly fragmented and non-standardized nature of downstream application scenarios also presents significant obstacles. Different industries, different tasks, and even different robot models have differentiated requirements for sensor size, performance, interfaces, and installation methods, making it difficult to achieve standardized mass production and resulting in high research and development and market expansion costs. Insufficient market awareness and education also hinder the speed of adoption. Many end-users, especially those in traditional industries, have limited understanding of the necessity, technical principles, and value of collision sensors, often viewing them as “optional accessories” that increase costs rather than “core components” that ensure safety and efficiency, resulting in a lengthy decision-making process. Furthermore, industry standards and certification systems are still evolving, lacking fully unified and widely accepted testing standards. This introduces uncertainty and additional costs into product performance comparisons, quality assessments, and market access. The shortage of professional talent, particularly interdisciplinary R&D personnel with expertise in mechanics, electronics, and software algorithms, also restricts rapid technological iteration and innovative breakthroughs. Finally, the stability of the supply chain, especially the supply of high-end chips and special materials, may become a potential risk in the complex international trade environment, affecting product delivery and cost control.

Industry Development Opportunities:

The robot collision sensor industry is experiencing unprecedented development opportunities. Firstly, the industrialization of humanoid robots has brought exponential growth in demand. To simulate human perception, individual humanoid robots need to be equipped with complex sensor arrays, including force, touch, and vision sensors, directly opening up a new market worth hundreds of billions. Secondly, continuous technological breakthroughs have injected strong momentum into the industry. Large-scale artificial intelligence models have significantly improved the intelligence level of multimodal perception. Multi-sensor fusion, edge computing, and self-learning algorithms are constantly optimizing sensor accuracy and response speed. Meanwhile, new materials such as flexible carbon nanotube substrates have significantly reduced manufacturing costs. The rapid expansion of application scenarios has provided vast opportunities. Sensor applications are rapidly extending from traditional industrial manufacturing to public services such as healthcare, smart agriculture, low-altitude economy, and home care, with increasingly diversified demands. Strong policy and capital support provide a solid backing. Governments worldwide have introduced industry incentive policies, and China has established a multi-billion-dollar industry fund. Meanwhile, the capital market is paying close attention, with a large influx of funds supporting technology research and development and capacity expansion. Finally, the accelerated process of domestic substitution has created a historic window of opportunity for domestic enterprises. Domestic companies have achieved substantial breakthroughs in core areas such as high-precision force sensors and electronic skin, highlighting the cost-effectiveness advantage of their products and continuously increasing their market share, thus reshaping the global competitive landscape.

About The Authors

Meng Yu Lead Author

Email: yumeng@qyresearch.com

QYResearch Nanning Research Center analyst, main research areas include semiconductors, chemical materials, electronics and other fields, some of the sub-research topics include Motor for semiconductor equipment, air bearing stage, low CTE ceramic material, high purity oleic acid, camera soc, intelligent energy management system, etc., also engaged in market segment report development, and participate in the writing of customized projects.

About QYResearch

QYResearch founded in California, USA in 2007.It is a leading global market research and consulting company. With over 17 years’ experience and professional research team in various cities over the world QY Research focuses on management consulting, database and seminar services, IPO consulting (data is widely cited in prospectuses, annual reports and presentations), industry chain research and customized research to help our clients in providing non-linear revenue model and make them successful. We are globally recognized for our expansive portfolio of services, good corporate citizenship, and our strong commitment to sustainability. Up to now, we have cooperated with more than 60,000 clients across five continents. Let’s work closely with you and build a bold and better future.

QYResearch is a world-renowned large-scale consulting company. The industry covers various high-tech industry chain market segments, spanning the semiconductor industry chain (semiconductor equipment and parts, semiconductor materials, ICs, Foundry, packaging and testing, discrete devices, sensors, optoelectronic devices), photovoltaic industry chain (equipment, cells, modules, auxiliary material brackets, inverters, power station terminals), new energy automobile industry chain (batteries and materials, auto parts, batteries, motors, electronic control, automotive semiconductors, etc.), communication industry chain (communication system equipment, terminal equipment, electronic components, RF front-end, optical modules, 4G/5G/6G, broadband, IoT, digital economy, AI), advanced materials industry Chain (metal materials, polymer materials, ceramic materials, nano materials, etc.), machinery manufacturing industry chain (CNC machine tools, construction machinery, electrical machinery, 3C automation, industrial robots, lasers, industrial control, drones), food, beverages and pharmaceuticals, medical equipment, agriculture, etc.

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 18 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp