Datacenter Electric DC-DC Converter Market Summary

Data center DC-DC converters refer to power electronic conversion devices used in data center power architectures to perform power conversion, voltage regulation, and power management between different DC voltage levels, and are typically delivered as finished DC-DC converter products that can be independently procured and deployed. These products mainly include board-mounted DC-DC modules and rack-level DC-DC converter units, and are used in applications such as server and accelerated computing power supply, rack and cabinet-level power distribution and conversion, energy storage and backup power interface conversion, and networking and communications equipment power supply. In 2025, global production of data center DC-DC converters reached 4.98 million units, with an average ex-factory price of USD 36 per unit.

Market Overview

Data center DC-DC converters are a key power electronics component in data center power architectures, primarily used for power conversion, voltage regulation, and power management between different DC voltage levels. Typical applications include server and accelerated computing power supply, rack- and cabinet-level power distribution and conversion, energy storage and backup power interface conversion, and networking and communications equipment power supply. With the rapid growth of AI training and inference workloads, continued increases in server power density, and the accelerating adoption of 48V intermediate bus architectures in data centers, demand is shifting from traditional general-purpose DC-DC module markets toward data center-specific converters featuring higher power density, higher efficiency, and higher reliability, creating strong structural growth characteristics. In terms of regional structure, North America, China, and other active data center buildout markets in Asia-Pacific are the main demand regions. North America remains the leading market, driven by hyperscale cloud capital expenditure, while China is growing rapidly, supported by computing infrastructure expansion and local server supply-chain development.

From a product structure perspective, the industry is characterized by board-mounted DC-DC modules as the main shipment volume contributor and rack-/cabinet-level DC-DC converter units as the main value contributor, forming a market structure in which high-volume modular products coexist with low-volume, high-ASP system-level products. Board-mounted DC-DC modules are widely deployed in server motherboards, power boards, and AI accelerator boards and serve as the core driver of shipment volume. Rack- and cabinet-level DC-DC converter units are used more often in high-power rack distribution and power architecture upgrades; they feature higher unit prices and longer validation cycles, and their revenue contribution is higher than their shipment share. By technology and topology, products can be further categorized into isolated and non-isolated types, which differ in their trade-offs among efficiency, size, EMC, and safety design, and they serve different roles across voltage architectures and application layers. As power density rises and thermal design constraints tighten, high-efficiency topologies, digital control, high-frequency magnetic components, and advanced packaging are becoming the core directions of product iteration.

From an application structure perspective, servers and AI accelerated computing equipment remain the largest source of demand, while networking switches, storage systems, and parts of rack-level power chains provide important supplementary demand. Industry demand comes not only from new server shipments and new data center rack deployments, but also from power architecture retrofits in existing data centers aimed at improving power efficiency, reducing losses, and supporting higher-power loads. As AI server penetration increases, the number of mid- to high-power DC-DC modules required per server is rising, driving up value per device. In terms of cost structure, product costs mainly consist of power semiconductor devices, magnetic components, control and driver chips, PCBs, and structural thermal management components, among which power devices and magnetic components have the greatest impact on efficiency, thermal performance, and cost. At the same time, high-power-density products require stricter testing, burn-in, and reliability verification, making manufacturing and quality-related costs a meaningful portion of total cost.

From the manufacturing side, data center DC-DC converters are power products with both high design barriers and high manufacturing barriers. Leading suppliers typically possess platform-based product development capabilities, automated assembly, full-process testing, and reliability verification capabilities. Single-line capacity varies significantly by product mix: for board-mounted DC-DC module production lines, single-line capacity is typically in the range of hundreds of thousands to several million units per year, and highly automated standardized lines for mature models can reach even higher levels; for rack-/cabinet-level DC-DC converter units, due to higher power ratings and greater assembly and testing complexity, single-line capacity is typically in the range of several thousand to tens of thousands of units per year. Industry gross margin is generally at a medium-to-high level, typically around 20%–40%. Standardized mid-power modules tend to be closer to the mid-range, while high-power-density, high-reliability data center-specific modules and system-level converter units with stronger customer certification barriers tend to have higher gross margins. Products with higher commoditization and more intense price competition tend to have lower gross margins. As AI-related demand grows and product mix shifts upward, the industry’s average gross margin has some support, although it can still be affected by upstream component price fluctuations and pricing pressure caused by high customer concentration.

In terms of industry chain structure and competitive landscape, upstream suppliers include power semiconductors, control chips, magnetic materials, and structural thermal management components; the midstream consists of DC-DC module and converter unit manufacturers; and downstream customers include server OEMs/ODMs, networking equipment manufacturers, system integrators, and data center operators. In the global market, international power module suppliers still maintain advantages in high-end data center application scenarios through accumulated technology, customer certifications, and delivery experience, while some Chinese manufacturers are accelerating penetration in mid- to high-power board-mounted modules and local supporting supply, improving competitiveness through response speed, cost control, and customization capabilities. Overall, industry concentration is higher than that of general industrial power subsegments, but a long tail of suppliers still exists, especially in general-purpose modules and regional customer markets where competition remains relatively fragmented.

Future industry trends will mainly center on higher power density, architecture upgrades, and more segmented application scenarios. On one hand, AI and high-performance computing will continue to increase server and rack power density, driving demand for mid- to high-power DC-DC modules. On the other hand, the rollout of 48V intermediate bus and higher-voltage DC distribution architectures will accelerate the penetration of bus converters, isolated high-power DC-DC converters, and rack-level converter units. At the same time, rising requirements from data center operators for energy efficiency, reliability, and maintenance convenience will push products toward higher efficiency, better monitoring capability, and easier maintenance. Overall, the data center DC-DC converter industry has both strong technology-driven and demand-driven characteristics and is expected to maintain solid growth and product mix optimization potential during the computing infrastructure upgrade cycle.

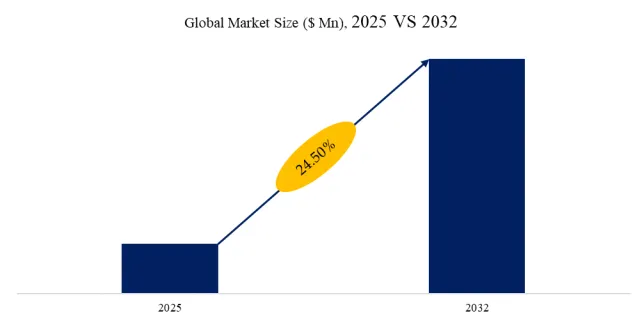

Figure00002. Global Datacenter Electric DC-DC Converter Market Size (US$ Million), 2025 vs 2032

Above data is based on report from QYResearch: Global Datacenter Electric DC-DC Converter Market Report 2026-2032 (published in 2026). If you need the latest data, plaese contact QYResearch.

According to the new market research report “Global Datacenter Electric DC-DC Converter Market Report 2026-2032”, published by QYResearch, the global Datacenter Electric DC-DC Converter market size is projected to reach USD 8.51 billion by 2032, at a CAGR of 24.5% during the forecast period.

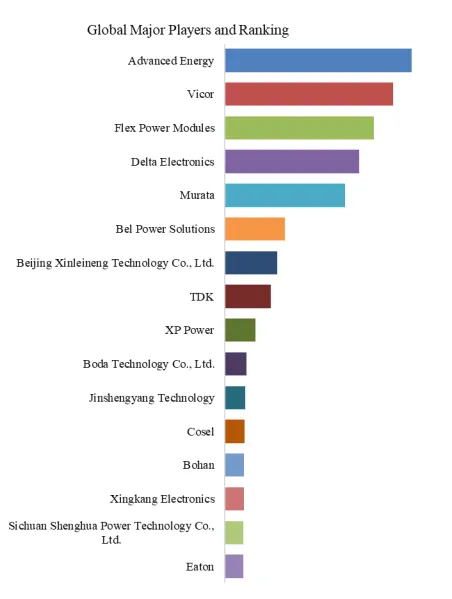

Figure00003. Global Datacenter Electric DC-DC Converter Top 16 Players Ranking and Market Share (Ranking is based on the revenue of 2025, continually updated)

Above data is based on report from QYResearch: Global Datacenter Electric DC-DC Converter Market Report 2026-2032 (published in 2026). If you need the latest data, plaese contact QYResearch.

According to QYResearch Top Players Research Center, the global key manufacturers of Datacenter Electric DC-DC Converter include Advanced Energy, Vicor, Flex Power Modules, Delta Electronics, Murata, Bel Power Solutions, Beijing Xinleineng Technology Co., Ltd., TDK, Boda Technology Co., Ltd., Jinshengyang Technology, etc. In 2025, the global top 10 players had a share approximately 71.0% in terms of revenue.

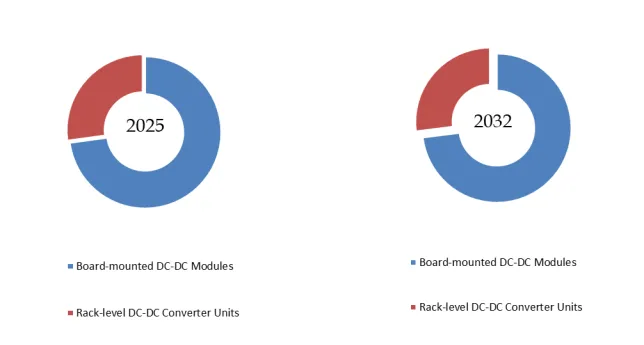

Figure00004. Datacenter Electric DC-DC Converter, Global Market Size, Split by Product Segment

Based on or includes research from QYResearch: Global Datacenter Electric DC-DC Converter Market Report 2026-2032.

In terms of product type, currently Board-mounted DC-DC Modules is the largest segment, hold a share of 72.83%.

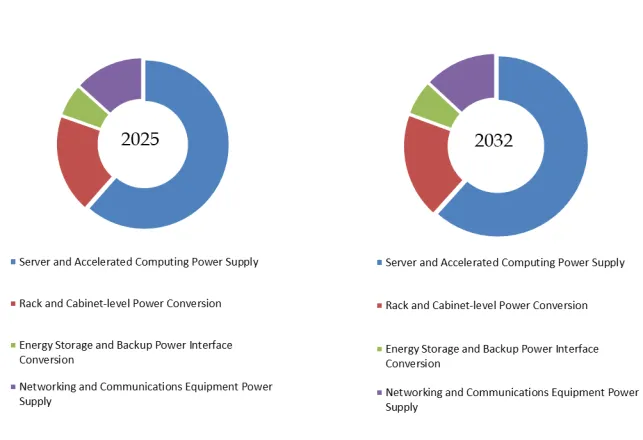

Figure00005. Datacenter Electric DC-DC Converter, Global Market Size, Split by Applications Segment

Based on or includes research from QYResearch: Global Datacenter Electric DC-DC Converter Market Report 2026-2032.

In terms of product application, currently Server and Accelerated Computing Power Supply is the largest segment, hold a share of 61.47%.

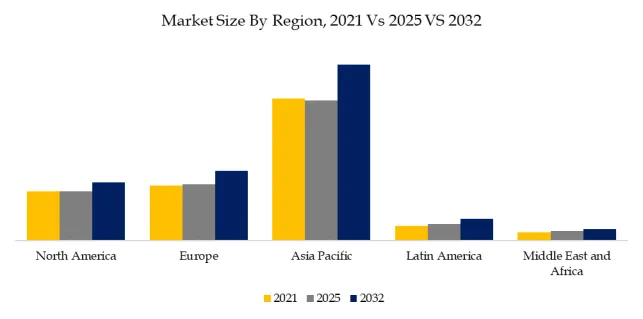

Figure00006. Datacenter Electric DC-DC Converter, Global Market Size, Split by Region

Based on or includes research from QYResearch: Global Datacenter Electric DC-DC Converter Market Report 2026-2032.

About the Authors

| Wei Qin – Electronics Industry Analyst

qinwei@qyresearch.com

Focusing on the electronics and communications field for a long time, she has observed, followed up and researched on various links in the industry chain, such as semiconductors, consumer electronics, home appliances, fiber optic communications, Internet of Things (IoT) and smart home for a long time. He has rich experience in industry research and has completed many successful cases. |

About QYResearch

QYResearch founded in California, USA in 2007.It is a leading global market research and consulting company. With over 17 years’ experience and professional research team in various cities over the world QY Research focuses on management consulting, database and seminar services, IPO consulting (data is widely cited in prospectuses, annual reports and presentations), industry chain research and customized research to help our clients in providing non-linear revenue model and make them successful. We are globally recognized for our expansive portfolio of services, good corporate citizenship, and our strong commitment to sustainability. Up to now, we have cooperated with more than 60,000 clients across five continents. Let’s work closely with you and build a bold and better future.

QYResearch is a world-renowned large-scale consulting company. The industry covers various high-tech industry chain market segments, spanning the semiconductor industry chain (semiconductor equipment and parts, semiconductor materials, ICs, Foundry, packaging and testing, discrete devices, sensors, optoelectronic devices), photovoltaic industry chain (equipment, cells, modules, auxiliary material brackets, inverters, power station terminals), new energy automobile industry chain (batteries and materials, auto parts, batteries, motors, electronic control, automotive semiconductors, etc.), communication industry chain (communication system equipment, terminal equipment, electronic components, RF front-end, optical modules, 4G/5G/6G, broadband, IoT, digital economy, AI), advanced materials industry Chain (metal materials, polymer materials, ceramic materials, nano materials, etc.), machinery manufacturing industry chain (CNC machine tools, construction machinery, electrical machinery, 3C automation, industrial robots, lasers, industrial control, drones), food, beverages and pharmaceuticals, medical equipment, agriculture, etc.

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 18 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp