Coolant Distribution Units (CDU) Market Summary

Coolant Distribution Unit (CDU) is an essential component in liquid cooling systems that distribute coolant or water evenly throughout the system. The CDU regulates and controls the flow of coolant, maintaining the desired temperature and flow rate. It works in conjunction with pumps, radiators, heat exchangers, and control units to ensure the cooling system runs smoothly and efficiently. The CDU also helps keep the system clean by removing impurities from the coolant, preventing clogging and damage to other components in the system. Overall, the CDU plays a critical role in maintaining the proper functioning of liquid cooling systems.

Above data is based on report from QYResearch: Global Coolant Distribution Units (CDU) Market Report 2026-2032 (published in 2026). If you need the latest data, plaese contact QYResearch.

Fast Market Growth: In the current landscape dominated by AI-driven applications and dense chip architectures, liquid cooling has emerged as a pivotal technology. CDU, as a key part in liquid cooling system, will benefit from the prevalence of AI and high-performance computing (HPC). The CDU market is expected to experience fast growth in the coming years.

Intensified Competition: As showing great market potential, many investors and companies have laid their attentions on the CDU market. With more and more companies will enter in the CDU industry, the whole market competition will be intensified in the coming years.

Continued Technology Innovation: CDU include liquid-to-liquid and liquid-to-air types. Though limited in cooling capability compared with liquid-to-liquid CDUs, liquid-to-air CDUs don’t require water pipes, can be installed more easily, and take less space and lower initial cost than liquid-to-liquid CDUs. While although liquid-to-liquid CDUs hold the best cooling performance of all types. They require, among others, pipes to be installed to operate with a facility’s water. More research and technology innovation will be put on liquid-to-liquid CDUs by CDU manufacturers to provide high performance CDU to data centers.

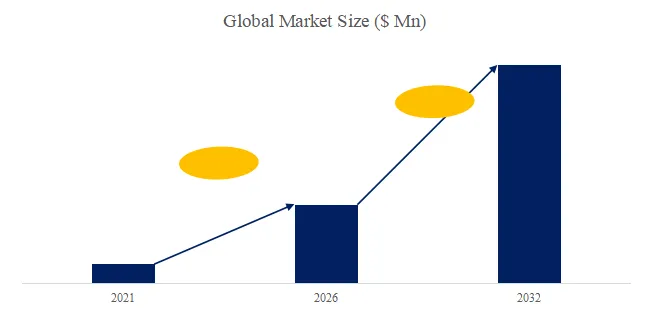

According to the new market research report “Global Coolant Distribution Units (CDU) Market Report 2026-2032″, published by QYResearch, the global Coolant Distribution Units (CDU) market size is projected to grow from USD 1,337 million in 2025 to USD 4,427 million by 2032, at a CAGR of 18.5% during the forecast period.

Figure00002. Global Coolant Distribution Units (CDU) Market Size (US$ Million), 2021-2032

Above data is based on report from QYResearch: Global Coolant Distribution Units (CDU) Market Report 2026-2032 (published in 2026). If you need the latest data, plaese contact QYResearch.

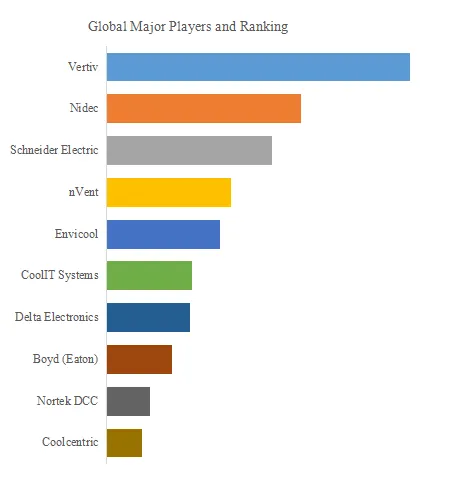

Figure00003. Global Coolant Distribution Units (CDU) Top 10 Players Ranking and Market Share (Ranking is based on the revenue of 2025, continually updated)

Above data is based on report from QYResearch: Global Coolant Distribution Units (CDU) Market Report 2026-2032 (published in 2026). If you need the latest data, plaese contact QYResearch.

This report profiles key players of Coolant Distribution Units (CDU) such as Vertiv, Nidec, Schneider Electric, nVent, Envicool.

In 2025, the global top three Coolant Distribution Units (CDU) players account for 48% of market share in terms of revenue. Above figure shows the key players ranked by revenue in Coolant Distribution Units (CDU).

Market Drivers:

One of the primary drivers behind the uptick in liquid cooling adoption is the escalating power density of modern IT equipment. With the proliferation of high-performance servers, GPUs, and AI accelerators, data centers are generating more heat than ever before. Traditional air-cooling systems struggle to effectively dissipate the heat generated by these dense workloads, leading to hotspots and reduced operational efficiency. Liquid cooling, on the other hand, offers a more efficient means of heat transfer and dissipation. By circulating coolant directly in contact with hot components, such as processors and graphics cards, liquid cooling systems can effectively remove heat at a faster rate than air-based solutions. This capability enables data centers to accommodate higher power densities while maintaining optimal operating temperatures, thereby improving overall performance and energy efficiency.

Restraint:

Air cooling uses air conditioning, fans, and vents to circulate ambient air, expelling the hot air produced by computing equipment. It’s the most traditional method and forms the basis for many data center cooling strategies. Compared with traditional air-cooling technology, the installation with additional power and water, higher cost as well as other questions bring great challenges to promote liquid cooling technology market share, which will impact the demand of CDU accordingly.

Opportunity:

As data center footprints continue to shrink due to urbanization and real estate constraints, optimizing space utilization has become a pressing priority for data center managers. Liquid cooling solutions offer a compact and space-efficient alternative to traditional air-cooling systems, enabling data centers to maximize their rack densities and floor space without compromising thermal performance. Moreover, the scalability of liquid cooling systems makes them well-suited for accommodating future growth and expansion. By modularizing cooling infrastructure and deploying liquid cooling units in a distributed manner, data centers can easily scale their cooling capacity in response to changing workload demands. This flexibility not only enhances operational agility but also streamlines the deployment of new IT equipment without the need for extensive retrofitting or reconfiguration.

About The Authors

| Maocai Zhang – Lead Author |

| Email: zhangmaocai@qyresearch.com |

About QYResearch

QYResearch founded in California, USA in 2007. It is a leading global market research and consulting company. With over 19 years’ experience and professional research team in various cities over the world QY Research focuses on management consulting, database and seminar services, IPO consulting (data is widely cited in prospectuses, annual reports and presentations), industry chain research and customized research to help our clients in providing non-linear revenue model and make them successful. We are globally recognized for our expansive portfolio of services, good corporate citizenship, and our strong commitment to sustainability. Up to now, we have cooperated with more than 70,000 clients across five continents. Let’s work closely with you and build a bold and better future.

QYResearch is a world-renowned large-scale consulting company. The industry covers various high-tech industry chain market segments, spanning the semiconductor industry chain (semiconductor equipment and parts, semiconductor materials, ICs, Foundry, packaging and testing, discrete devices, sensors, optoelectronic devices), photovoltaic industry chain (equipment, cells, modules, auxiliary material brackets, inverters, power station terminals), new energy automobile industry chain (batteries and materials, auto parts, batteries, motors, electronic control, automotive semiconductors, etc.), communication industry chain (communication system equipment, terminal equipment, electronic components, RF front-end, optical modules, 4G/5G/6G, broadband, IoT, digital economy, AI), advanced materials industry Chain (metal materials, polymer materials, ceramic materials, nano materials, etc.), machinery manufacturing industry chain (CNC machine tools, construction machinery, electrical machinery, 3C automation, industrial robots, lasers, industrial control, drones), food, beverages and pharmaceuticals, medical equipment, agriculture, etc.

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 18 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp