Global Leading Market Research Publisher Global Info Research announces the release of its latest report *“Slotted Optical Sensors – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”.* Based on current situation and impact historical analysis (2021-2025) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Slotted Optical Sensors market, including market size, share, demand, industry development status, and forecasts for the next few years.

For engineers designing office automation, industrial controls, and consumer devices, non‑contact detection of object presence or position is critical. Slotted optical sensors (also called transmissive photointerrupters) are compact, non‑contact sensors that detect the interruption of light across a narrow slot. They consist of an infrared LED emitter and a phototransistor detector facing each other across a slot. When an object passes through the slot, the light beam is blocked, triggering an output change. These sensors are widely used for precise object, position, and motion detection in printers/scanners (paper detection, carriage home position), home appliances (door closure, drum rotation), industrial automation (limit switches, counting), and consumer electronics (encoder wheels, flip phones). The market is driven by increasing automation, demand for reliable position sensing, and proliferation of smart devices. Average sensor price: $0.50-2.00.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/6093253/slotted-optical-sensors

Market Valuation & Growth Trajectory (2026-2032)

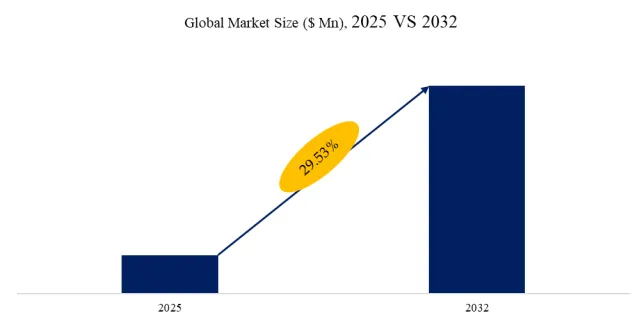

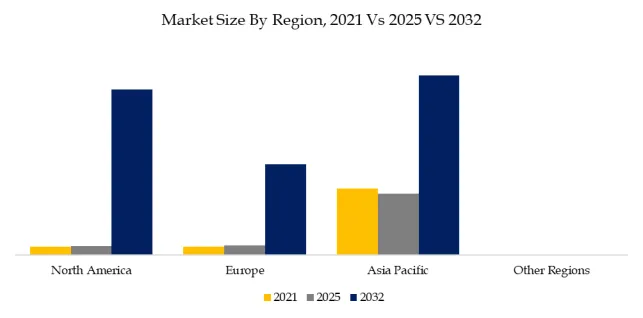

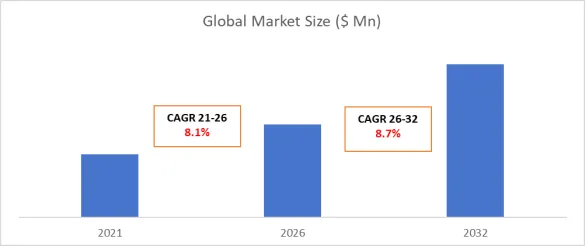

The global market for Slotted Optical Sensors was estimated to be worth approximately US1.33billionin2025∗∗andisprojectedtoreach∗∗US1.33billionin2025∗∗andisprojectedtoreach∗∗US 1.96 billion by 2032, growing at a CAGR of 5.7% from 2026 to 2032 (Source: Global Info Research, 2026 revision). This steady growth reflects increased office automation equipment sales, industrial robot adoption, and home appliance smart features. Key regions: Asia‑Pacific (60% of sales, manufacturing), North America (20%), Europe (15%), Rest of World (5%). Price range: 0.30−1.00(standard),0.30−1.00(standard),1-3 (high‑precision). Slotted sensors are characterized by slot width (gap). Types: 5mm and below (standard, high resolution), 5mm and above (larger objects, less precise). Gap width: 1-10 mm common. Smaller gap = higher positional accuracy. Output: digital (TTL, open collector), analog (current). Sensing distance equals gap width (through‑beam). Operating voltage: 3-24 V DC. Response time: microseconds. Temperature range: -20 to +85°C. Housing: PC (polycarbonate), PBT. Mounting: PCB (through‑hole, surface‑mount), connector. Slotted sensors are immune to ambient light (shielded). Unlike reflective sensors, object color/reflectivity does not affect detection (beam block vs reflect). Used as limit switches (no contact). Encoder disk (rotation) with multiple slots. Printer: 5-10 sensors (paper feed, platen, carriage). Industrial automation: part present, jam detection. Consumer electronics: flip phone hinge, camera shutter, tape deck end.

Exclusive Observer Insights (Q1-Q2 2026): Key market trends include: (1) miniature slotted sensors (SMD) for portable electronics; (2) high‑speed sensing (fast response); (3) logic level output (3.3V, 5V) for microcontrollers; (4) water‑resistant (IP67) for outdoor; (5) custom gap width, mounting. Slotted sensors advantages over mechanical switches: non‑contact (no wear), high speed (no bounce), long life (10+ years). Disadvantages: dust sensitive (reduce sensitivity). Solutions: enclosed housing, self‑cleaning. Sensor with integrated amplifier (threshold adjust). Phototransistor (analog output) vs photodiode (faster). Applications: encoders (rotary, linear), edge detection, hole detection, liquid level (float). Healthcare: lab equipment. Packaging: candy count. Automotive: sunroof position, seat belt detection.

Key Market Segments: By Type, Application, and Gap

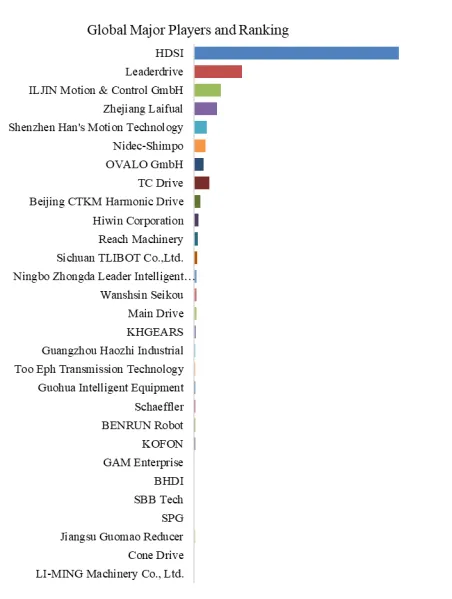

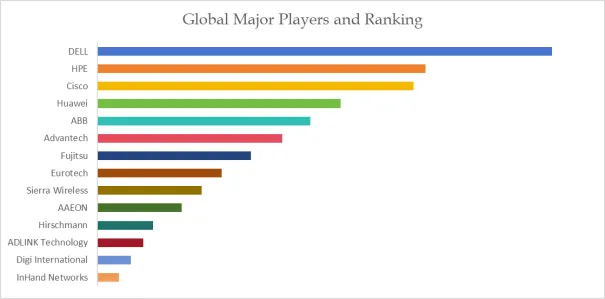

Major players include Omron, Sharp, Rohm Semiconductor, Vishay, Panasonic, TT Electronics, Honeywell, Toshiba, OSRAM, On Semiconductor, Kodenshi Corporation, Nippon Aleph, OncQue Corporation, Kingbright Electronic, Stanley Electric, Shinkoh, Okaya Electric Industries, Edison Opto Corporation, Lite‑On, and Everlight Electronics.

Segment by Type (Gap Width)

- 5 mm and Below – Largest volume (approx. 75% of units). High precision, standard for printers, encoders, small object detection.

- 5 mm and Above – Second (approx. 25% of units). Larger objects, less precise (industrial).

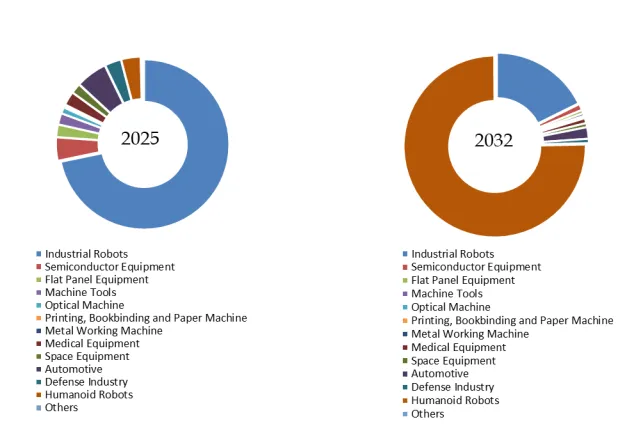

Segment by Application

- Printers and Scanners – Largest (approx. 35% of market). Paper detection, home position, jam detection.

- Industrial Automation – Second (approx. 25% of market). Limit switch, object counting, position.

- Home Appliances – Third (approx. 20% of market). Door closure, drum rotation.

- Consumer Electronics – Fourth (approx. 15% of market). Flip phone, encoder, rotation.

- Others – Medical, automotive. Approx. 5% of market.

Industry Layering: Slotted Sensor Gap Selection

| Gap Width | Typical Application | Resolution | Object Size | Price | Market Share |

|---|---|---|---|---|---|

| 1-2 mm | Encoder disk (fine), paper edge | High | Small | Medium | 30% |

| 3-5 mm | Printer carriage, object detection | Medium | Small-medium | Low | 45% |

| 5-10 mm | Industrial jams, large object | Low | Large | Low | 25% |

Technological Challenges & Market Drivers (2025-2026)

- Dust accumulation – Dust particles block light. Enclosed slot, self‑cleaning. Sensitivity adjustment.

- Vibration – Loose mounting misaligns emitter/detector. Robust housing.

- Ambient light – Sunlight, fluorescent. Shielded, modulated IR, optical filter.

- Cost pressure – Low cost ($0.30-1.00). Chinese manufacturers compete.

Real-World User Case Study (2025-2026 Data):

An industrial printer manufacturer (1 million units/year) replaced mechanical limit switch with slotted optical sensor (Omron, 5 mm gap, $0.80) for carriage home position. Baseline (mechanical): wear (500k cycles), bounce (debounce circuit). After optical (2025):

- Lifespan: 10+ years. Warranty reduction.

- Cost: 0.80vs0.80vs0.40 (+0.40).1Mx0.40).1Mx0.40 = $400k additional.

- Reliability: MTBF 5x higher.

- Result: Printer manufacturer adopted throughout product line.

Exclusive Industry Outlook (2027–2032):

Three strategic trajectories by 2028:

- Precision (≤5 mm) tier (Omron, Sharp, Rohm, Vishay, Panasonic, TT, Honeywell, Toshiba, On Semi) — 6-7% CAGR. $0.50-2.00.

- Industrial (>5 mm) tier (OSRAM, Kodenshi, Nippon Aleph, OncQue, Kingbright, Stanley, Shinkoh, Okaya, Edison, Lite‑On, Everlight) — 5-6% CAGR. $0.30-1.50.

- Miniature SMD tier — 7-8% CAGR (fastest‑growing). Portable electronics.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

Global Info Research

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp

% during the forecast period.

% during the forecast period.