Introduction (Covering Core User Needs: Pain Points & Solutions):

Global Leading Market Research Publisher QYResearch announces the release of its latest report “IoT eSIM IC – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032″. Based on current situation and impact historical analysis (2021-2025) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global IoT eSIM IC market, including market size, share, demand, industry development status, and forecasts for the next few years.

For IoT device manufacturers and large-scale deployers, traditional removable SIM cards present significant operational challenges: physical card slots consume valuable PCB space, SIM cards are vulnerable to tampering or environmental damage, and swapping operators requires manual field intervention. An IoT eSIM IC (Embedded Subscriber Identity Module Integrated Circuit) is a compact, programmable chip embedded into IoT devices that enables remote provisioning and secure mobile network authentication without needing a physical SIM card. Unlike traditional SIMs, eSIM ICs can switch between mobile network operators over-the-air (OTA), enhancing flexibility and reducing the need for manual replacement in large-scale or hard-to-reach deployments. This technology is especially valuable in IoT applications such as smart meters, industrial sensors, connected vehicles, and wearables, where reliability, longevity, and remote management are critical. As cellular IoT connections accelerate (projected 3-4 billion by 2030) and GSMA eSIM specifications mature, IoT eSIM ICs are transitioning from early adopter technology to standard connectivity component for mass-market IoT deployments.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)

https://www.qyresearch.com/reports/6095101/iot-esim-ic

1. Market Sizing & Growth Trajectory (With 2026–2032 Forecasts)

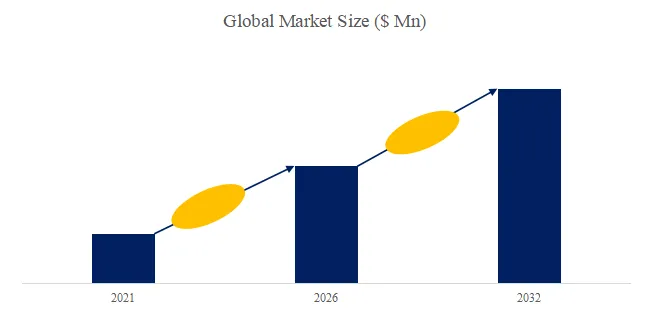

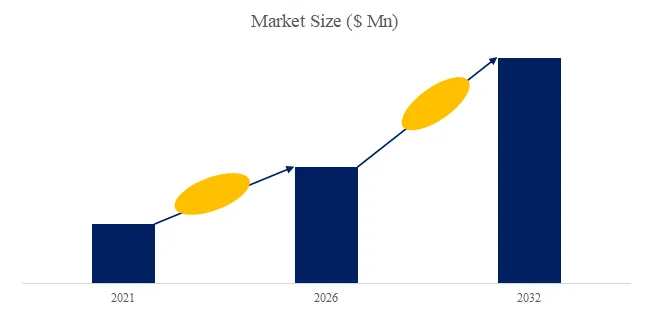

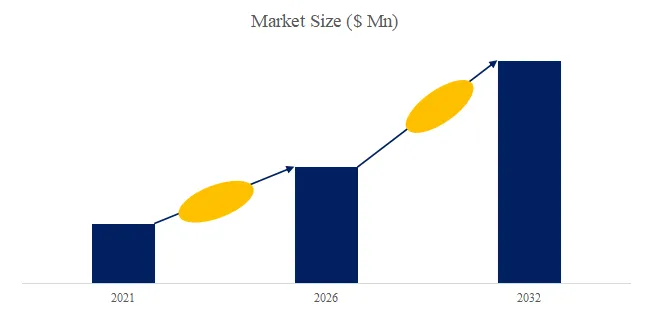

The global market for IoT eSIM IC was estimated to be worth US$1,049 million in 2025 and is projected to reach US$1,866 million by 2032, growing at a CAGR of 8.7% from 2026 to 2032. This strong growth is driven by three converging factors: (1) accelerating cellular IoT adoption across smart metering, asset tracking, and industrial monitoring, (2) GSMA eSIM specifications for IoT (SGP.02, SGP.32) enabling standardized remote provisioning, and (3) device miniaturization favoring soldered embedded chips over removable SIM card slots.

By form factor, MFF2 (Miniature Form Factor 2, 5×6×0.9mm) dominates with approximately 70% of unit volume (standard for industrial IoT). WLCSP (Wafer-Level Chip Scale Package, 2-4mm square) accounts for 20% (ultra-compact wearables and sensors). Others account for 10%.

2. Technology Deep-Dive: eUICC Architecture, Secure Element, and OTA Profile Management

Technical nuances often overlooked:

- Embedded secure element chip architecture: IoT eSIM IC consists of eUICC (embedded Universal Integrated Circuit Card) silicon with secure element (Java Card platform, CC EAL4+ to EAL6+ certified), non-volatile memory (1-5MB for profile storage), and communication interfaces (ISO 7816, SPI, I²C). Operating system implements GSMA eSIM specifications.

- Over-the-air network profile switching: Subscription management platform (SM-DP+, Subscription Manager Data Preparation) securely delivers encrypted operator profiles over cellular or Wi-Fi. Profile switching triggers re-authentication to target network (5-30 seconds). Supports multiple profiles (2-10) with active profile selection.

Recent 6-month advances (October 2025 – March 2026):

- STMicroelectronics launched “ST4SIM-200M” – industrial-grade IoT eSIM IC (MFF2) with extended temperature range (-40°C to +105°C) and 10-year data retention. Supports GSMA SGP.32 (IoT eSIM specification) and 5G SA networks. Integrated secure element CC EAL6+ certified. Price US$2.50-4.00.

- Infineon introduced “OPTIGA Connect IoT eSIM” – WLCSP eSIM IC (2.5×2.5×0.4mm) for ultra-compact wearables and sensors. Integrated energy harvesting interface (1µA sleep current). GSMA SGP.02 and SGP.32 certified. Price US$2.00-3.50.

- NXP commercialized “SN110 Secure IoT eSIM” – integrated eSIM IC + discrete secure element with NFC interface for contactless provisioning. Target: smart meters with in-field commissioning via NFC-enabled smartphones. Price US$3.00-5.00.

3. Industry Segmentation & Key Players

The IoT eSIM IC market is segmented as below:

By Form Factor (Physical Package):

- MFF2 Form-factor – 5×6×0.9mm, 8-32 contacts. Industrial IoT standard. Price: US$1.50-4.00. Dominant.

- WLCSP Form-factor – 2-4mm square, 0.3-0.5mm thickness. Ultra-compact, higher cost. Price: US$2.00-5.00.

- Others (DFN, QFN) – Niche form factors. Price: US$1.80-3.50.

By Application (End-Use Sector):

- Consumer Electronics (wearables, smart watches, fitness trackers, tablets) – 35% of 2025 revenue.

- Internet of Things (smart meters, connected vehicles, asset trackers, industrial sensors, medical devices, POS terminals) – 55% of revenue, fastest-growing at 10.5% CAGR.

- Others (smart home, drones, robotics) – 10%.

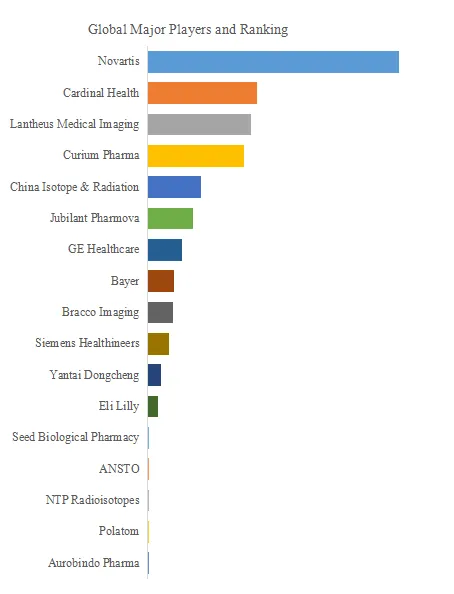

Key Players (2026 Market Positioning):

Semiconductor/IC Suppliers: STMicroelectronics (Switzerland/Italy), NXP (Netherlands), Infineon (Germany), GCT Semiconductor (Korea/USA), Unigroup Guoxin Microelectronics (China), HuaDa Semiconductor (China), Henghui Technology (China).

eSIM Solution Providers (also supplying ICs or bundled solutions): Thales Group (France), IDEMIA (France), Giesecke+Devrient (Germany), VALID (Brazil), Workz (Trasna, Ireland).

独家观察 (Exclusive Insight): The IoT eSIM IC market displays a two-tier structure with STMicroelectronics, NXP, and Infineon dominating (≈60-65% combined share), leveraging secure element expertise, manufacturing scale (12-inch wafer fabs), and GSMA certification. Thales, IDEMIA, and G+D lead in eSIM operating system and remote provisioning platforms, often supplying ICs through partnerships or in-house manufacturing. Chinese suppliers (Unigroup Guoxin, HuaDa Semiconductor, Henghui Technology) are rapidly gaining domestic market share (China IoT eSIM IC shipments estimated 150-200 million units by 2026), with 20-30% lower pricing and government support for domestic semiconductor content. GCT Semiconductor specializes in integrated eSIM + cellular IoT connectivity (eSIM IC + modem in single package). The market is seeing vertical integration: semiconductor suppliers adding COS and provisioning capabilities (ST’s Truphone partnership), and solution providers developing in-house ICs.

4. User Case Study & Policy Drivers

User Case (Q1 2026): Landis+Gyr (Switzerland/USA) – global smart meter manufacturer. Landis+Gyr adopted STMicroelectronics ST4SIM-200M eSIM ICs across 20 million cellular electricity meters deployed in Europe and North America (2024-2025 rollout). Key performance metrics:

- Field failure rate: <0.01% (vs. 0.5-0.8% for removable SIMs – corrosion, contact oxidation, physical damage)

- Remote network switching: migrated 8 million meters from Vodafone to Deutsche Telekom in 72 hours – avoided US$15-20 million in field truck rolls

- PCB space saving: eliminated SIM card holder (saved 70mm², reduced meter thickness by 2mm)

- Inventory simplification: single global eSIM IC SKU vs. 40+ country-specific removable SIM SKUs – inventory cost reduced 65%

- Cost comparison: eSIM IC US$2.80 vs. removable SIM US$0.90 + holder US$0.30 = US$1.20 – 2.3× higher component cost, offset by operational savings

Policy Updates (Last 6 months):

- GSMA SGP.32 (IoT eSIM Specification) – Final release (December 2025): Defines remote provisioning for large-scale IoT devices (optimized for low-power, high-volume, M2M). All major eSIM IC suppliers (ST, NXP, Infineon, Thales, IDEMIA, G+D) announced SGP.32 compliance.

- EU Cyber Resilience Act (CRA) – eSIM security requirements (January 2026): Requires eSIM ICs in connected devices to meet minimum CC EAL4+ for industrial IoT, EAL5+ for metering/automotive. Non-compliant ICs cannot be used in EU market.

- China MIIT – eSIM IC domestic content requirement (November 2025): Government-subsidized smart meter projects require domestic eSIM ICs (Unigroup Guoxin, HuaDa, Henghui). Foreign ICs (ST, NXP, Infineon) permitted for non-subsidized commercial deployments.

5. Technical Challenges and Future Direction

Despite strong growth, several technical challenges persist:

- Interoperability across MNOs: Not all mobile network operators support GSMA eSIM specifications; IoT devices may require pre-loaded profiles for target markets as fallback.

- Remote provisioning latency: Profile download (10-60 seconds) and switching (5-30 seconds) may delay device commissioning; use cases requiring instant connectivity may retain removable SIMs.

- eSIM IC lifecycle management: Managing millions of devices with multiple profiles requires robust cloud-based subscription management platforms, adding operational overhead for smaller deployers.

独家行业分层视角 (Exclusive Industry Segmentation View):

- Discrete IoT deployments (smart meters, connected vehicles, medical devices, industrial sensors) prioritize long lifecycle (10-15 years), remote provisioning (no field access), and security certification (CC EAL5+). Typically use MFF2 eSIM ICs from ST, NXP, Infineon with GSMA SGP.32. Key drivers are field reliability and regulatory compliance.

- Flow process IoT deployments (consumer wearables, asset trackers, smart home devices) prioritize cost (US$1.50-3.00), small form factor (WLCSP), and ease of integration. Typically use WLCSP eSIM ICs from Chinese suppliers or bundled solutions. Key metrics are cost per device and activation speed.

By 2030, IoT eSIM ICs will evolve toward iSIM (integrated SIM) – eSIM functionality embedded directly into cellular modem chip (no separate eUICC). Prototype products (GCT, ST, Qualcomm, MediaTek) integrate eSIM, cellular modem (NB-IoT, LTE-M, 5G RedCap), and application processor on single die, reducing BOM cost by 30-50% and PCB area by 60%. As embedded secure element chip technology matures and over-the-air profile switching becomes standard, IoT eSIM ICs will become the default connectivity component for cellular IoT deployments globally.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666 (US)

JP: https://www.qyresearch.co.jp