Prostate Tumor Drugs Market Summary

Prostate tumor drugs refer to a class of systemic therapeutic agents used for the prevention, control, and treatment of prostate cancer, including hormonal therapy, chemotherapy, targeted therapy, and immunotherapy. Among these, androgen deprivation therapy (ADT) and androgen receptor pathway inhibitors are the foundational approaches, reducing androgen levels or blocking their signaling pathways to inhibit tumor growth and progression. With advances in precision medicine and molecular biology, therapies such as PARP inhibitors, radioligand therapy, and immunotherapy are increasingly applied in advanced and metastatic cases, significantly expanding treatment options. These drugs are characterized by long-term administration, combination regimens, and personalized treatment strategies, forming a key component of chronic cancer management. Driven by target innovation and evolving therapeutic strategies, this segment continues to grow steadily and represents a high-barrier area within the oncology therapeutics market.

The growth of the prostate tumor drugs market in Spain is primarily driven by an aging population and the continuous improvement of the public healthcare system. Increased emphasis on cancer screening and early diagnosis has led to higher detection rates, expanding demand for pharmacological treatments. At the same time, strong adherence to European clinical guidelines has accelerated the adoption of next-generation androgen receptor inhibitors and targeted therapies, driving treatment upgrades. In addition, the gradual inclusion of innovative drugs in the national health system and the development of oncology networks provide a solid foundation for market growth.

The main challenges in Spain stem from fiscal pressure and regional disparities within the healthcare system. Strict cost-control measures in the public healthcare system require new drugs to undergo complex pricing and reimbursement processes, delaying market entry. Differences in healthcare infrastructure and drug accessibility across autonomous regions further hinder the uniform adoption of innovative therapies. Moreover, intensifying competition, particularly in hormonal and targeted therapies, results in limited product differentiation and ongoing pricing pressure.

In Spain, demand for prostate cancer treatment is shifting toward chronic disease management and personalized medicine. As patient survival improves, the need for long-term maintenance therapy continues to grow, with oral drugs becoming increasingly preferred due to better compliance. The rising proportion of advanced and metastatic cases is driving the widespread use of combination therapies. Additionally, the integration of genetic testing into clinical decision-making is boosting demand for personalized treatments. The expansion of outpatient and day-care treatment models is also increasing demand for convenient and minimally invasive therapies.

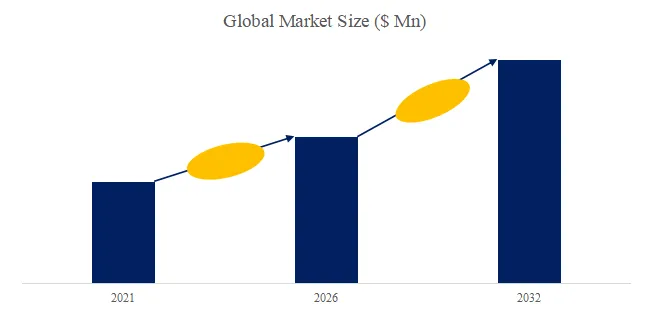

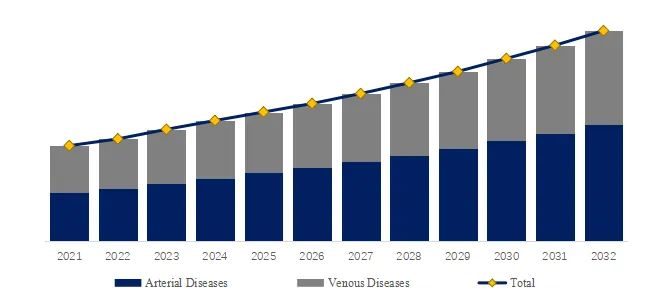

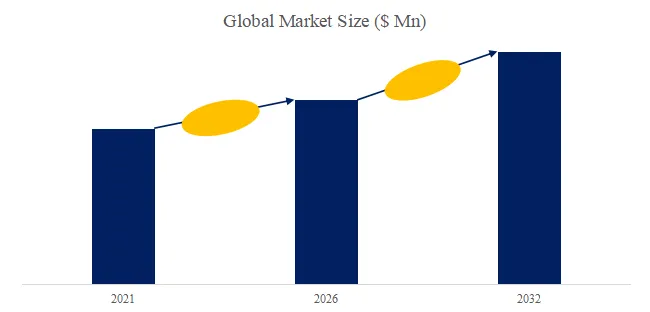

According to the new market research report “Spain Prostate Tumor Drugs Market Report 2026-2032”, published by QYResearch, the Spain Prostate Tumor Drugs market size is projected to reach USD 0.85 billion by 2032, at a CAGR of 11.9% during the forecast period.

Figure00001. Spain Prostate Tumor Drugs Market Size (US$ Million), 2021-2032

Above data is based on report from QYResearch: Global Prostate Tumor Drugs Market Report 2026-2032 (published in 2025). If you need the latest data, plaese contact QYResearch.

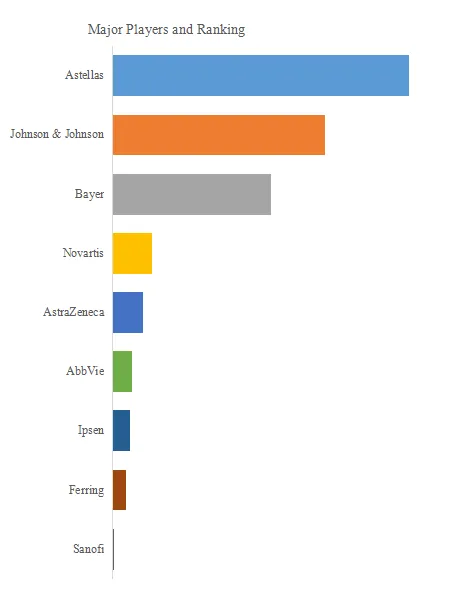

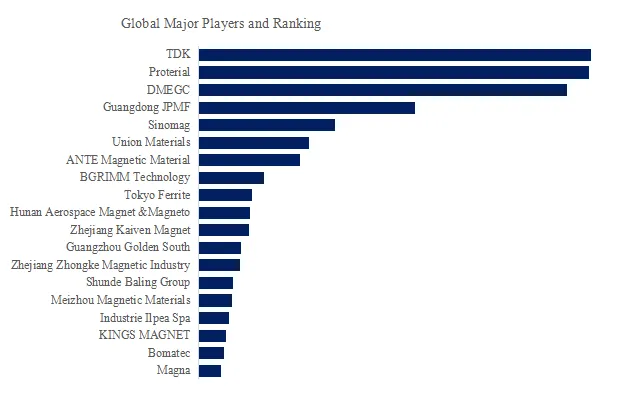

Figure00002. Spain Prostate Tumor Drugs Top 9 Players Ranking and Market Share (Ranking is based on the revenue of 2025, continually updated)

Above data is based on report from QYResearch: Global Prostate Tumor Drugs Market Report 2026-2032 (published in 2025). If you need the latest data, plaese contact QYResearch.

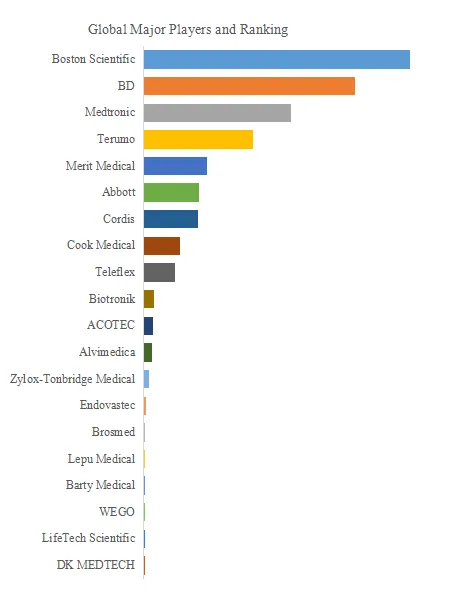

According to QYResearch Top Players Research Center, the Spain key manufacturers of Prostate Tumor Drugs include Astellas, Johnson & Johnson, Bayer, Novartis, etc. In 2025, the Spain top four players had a share approximately 76.0% in terms of revenue.

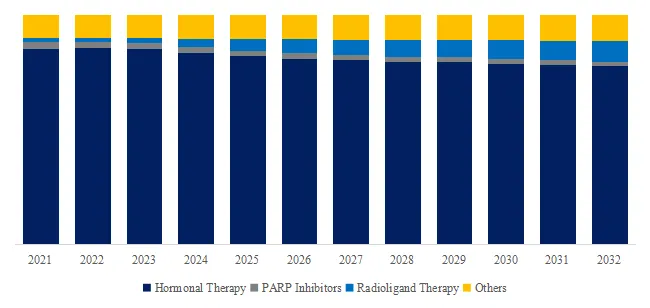

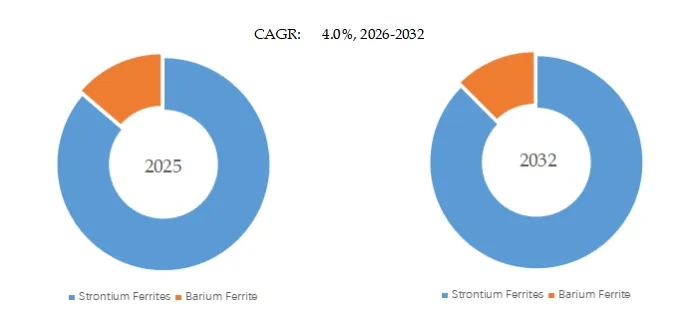

Figure00003. Prostate Tumor Drugs, Spain Market Size, Split by Product Segment

Based on or includes research from QYResearch: Global Prostate Tumor Drugs Market Report 2026-2032.

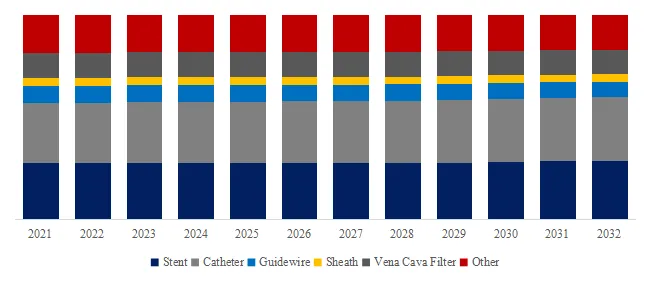

In terms of product type, currently Hormonal Therapy is the largest segment, hold a share of 82.2%.

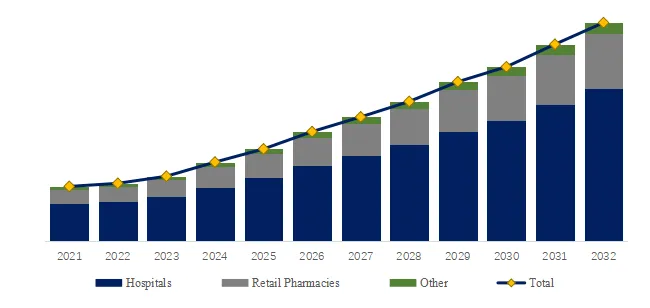

Figure00004. Prostate Tumor Drugs, Spain Market Size, Split by Application Segment

Based on or includes research from QYResearch: Global Prostate Tumor Drugs Market Report 2026-2032.

In terms of product application, currently Hospitals is the largest segment, hold a share of 68.6%.

About The Authors

Zhang Xiao – Lead Author

Email: zhangxiao@qyresearch.com

Zhang Xiao is a market senior analyst specializing in medical device, pharma, Lab consumable. Zhang Xiao has 8 years’ experience in medical device and pharma market analysis, and focuses on medical device and consumables (imaging equipment, medical consumables, wearable medical equipment, medical robots, home care equipment, dental equipment, implant equipment, operating room equipment, in vitro diagnostics, etc.) and drugs (API, finished drugs, patented drugs, blood products , vaccines, etc.) . She is engaged in the development of technology and market reports and is also involved in custom projects.

About QYResearch

QYResearch founded in California, USA in 2007.It is a leading global market research and consulting company. With over 17 years’ experience and professional research team in various cities over the world QY Research focuses on management consulting, database and seminar services, IPO consulting (data is widely cited in prospectuses, annual reports and presentations), industry chain research and customized research to help our clients in providing non-linear revenue model and make them successful. We are globally recognized for our expansive portfolio of services, good corporate citizenship, and our strong commitment to sustainability. Up to now, we have cooperated with more than 60,000 clients across five continents. Let’s work closely with you and build a bold and better future.

QYResearch is a world-renowned large-scale consulting company. The industry covers various high-tech industry chain market segments, spanning the semiconductor industry chain (semiconductor equipment and parts, semiconductor materials, ICs, Foundry, packaging and testing, discrete devices, sensors, optoelectronic devices), photovoltaic industry chain (equipment, cells, modules, auxiliary material brackets, inverters, power station terminals), new energy automobile industry chain (batteries and materials, auto parts, batteries, motors, electronic control, automotive semiconductors, etc.), communication industry chain (communication system equipment, terminal equipment, electronic components, RF front-end, optical modules, 4G/5G/6G, broadband, IoT, digital economy, AI), advanced materials industry Chain (metal materials, polymer materials, ceramic materials, nano materials, etc.), machinery manufacturing industry chain (CNC machine tools, construction machinery, electrical machinery, 3C automation, industrial robots, lasers, industrial control, drones), food, beverages and pharmaceuticals, medical equipment, agriculture, etc.

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 18 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp

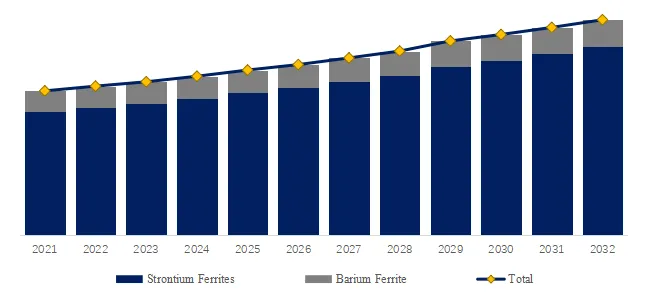

. Global Permanent Magnet Ferrite Magnet Top 19 Players Ranking and Market Share (Ranking is based on the revenue of 2025, continually updated)

. Global Permanent Magnet Ferrite Magnet Top 19 Players Ranking and Market Share (Ranking is based on the revenue of 2025, continually updated) Permanent Magnet Ferrite Magnet, Global Market Size, Split by Product Segment

Permanent Magnet Ferrite Magnet, Global Market Size, Split by Product Segment