Global Leading Market Research Publisher QYResearch announces the release of its latest report “Lithium Tantalate on Silicon Heterogeneous Wafer – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032″. Based on current situation and impact historical analysis (2021-2025) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Lithium Tantalate on Silicon Heterogeneous Wafer market, including market size, share, demand, industry development status, and forecasts for the next few years.

For silicon photonics engineers, optical component manufacturers, and telecommunications infrastructure planners, the persistent challenge remains consistent: integrating high-performance electro-optic materials (high Pockels coefficient, low optical loss, thermal stability) with CMOS-compatible silicon waveguides to enable high-speed modulation, switching, and sensing on a single chip. Lithium Tantalate on Silicon Heterogeneous Wafer addresses this by combining silicon-based materials with lithium tantalate (LiTaO₃) crystal materials – a ferroelectric material with excellent electro-optic properties (r₃₃ ~30 pm/V, similar to lithium niobate (LiNbO₃) but with lower birefringence and higher thermal stability). The heterogeneous wafer enables optical modulators (high-speed data transmission), optical switches (routing in data center networks), optical sensors (electric field sensing, gyroscopes), and others (frequency combs, quantum photonics). Key technologies include direct bonding (direct wafer-to-wafer or die-to-wafer bonding of LiTaO₃ thin films onto silicon substrates) and indirect bonding (using intermediate adhesive or oxide layers). Currently, Shanghai Novel Si Integration Technology Co., Ltd is the primary commercial supplier.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/5720155/lithium-tantalate-on-silicon-heterogeneous-wafer

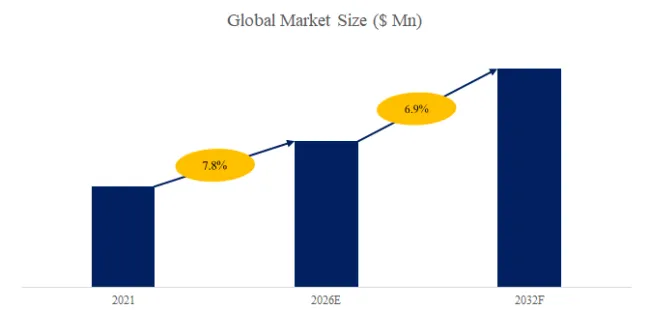

1. Market Size & Growth Trajectory (2026–2032)

The global market for Lithium Tantalate on Silicon Heterogeneous Wafer was estimated to be worth US$ 35 million in 2025 and is projected to reach US$ 280 million by 2032, growing at a CAGR of 34.5% from 2026 to 2032. In 2024, the market was in early commercialization stage, with Shanghai Novel Si Integration (NovelSi) as the sole volume supplier, shipping approximately 5,000-8,000 wafers (4-inch, 6-inch, and 8-inch diameters). Pricing ranges from $500 to $2,000 per wafer depending on diameter, LiTaO₃ film thickness (0.5-5μm), bonding method, and defect density.

Exclusive industry observation: The LiTaO₃-on-Si heterogeneous wafer market is experiencing nascent but explosive growth potential (34.5% CAGR) driven by three transformative factors: (1) LiTaO₃ as LiNbO₃ alternative (lower optical loss, higher damage threshold, better thermal stability, CMOS compatibility potential); (2) silicon photonics integration demands (overcoming silicon’s weak Pockels effect requires heterogeneous integration of electro-optic materials); (3) China’s semiconductor self-sufficiency push (domestic supply of advanced photonic wafers for telecom, data center, and sensing applications).

2. Industry Segmentation & Key Players

The market is segmented by type into Direct Bonding (direct wafer bonding (DWB) or surface-activated bonding (SAB), no intermediate layer) and Indirect Bonding (adhesive bonding using BCB (benzocyclobutene), SiO₂, or polymer intermediate layers), and by application into Optical Modulator, Optical Switch, Optical Sensor, and Others.

By Bonding Technology – Performance and Manufacturing Trade-offs

| Bonding Type | Process | Interface Layer | Optical Loss | Thermal Stability | Bond Strength | Cost | 2025 Share |

|---|---|---|---|---|---|---|---|

| Direct Bonding | Surface activation (plasma), room temperature or thermal compression bonding | None (LiTaO₃ directly on Si) | Lowest (<0.1 dB/cm) | Excellent (500°C+ stable) | High (5-10 J/m²) | Higher ($1,500-2,000/wafer) | 60% |

| Indirect Bonding | Adhesive (BCB, polymer) or oxide (SiO₂) intermediate layer | BCB (0.5-2μm) or SiO₂ (0.1-1μm) | Higher (0.5-2 dB/cm) | Moderate (BCB limited to 250-300°C) | Moderate (adhesive-dependent) | Lower ($500-1,000/wafer) | 40% |

Industry layer analysis – Discrete vs. Process Analogies: Optical Modulator (≈50% of LiTaO₃-on-Si wafer revenue, analogous to “high-performance telecom” – lowest loss critical, highest cost tolerance) drives direct bonding adoption (phase modulators, IQ modulators for 100G/400G/800G coherent transceivers). Optical Switch (≈25%, analogous to “data center routing” – moderate loss acceptable, cost-sensitive) uses both direct and indirect bonding. Optical Sensor (≈15%, analogous to “specialty sensing” – electric field, voltage, temperature sensors) favors direct bonding for stability. Others (≈10%) includes frequency comb generation, quantum photonics, nonlinear optics.

Key Supplier (2025)

Shanghai Novel Si Integration Technology Co., Ltd (NovelSi) is the sole commercial supplier of lithium tantalate on silicon heterogeneous wafers. Founded in 2014 (spin-off from Shanghai Institute of Microsystem and Information Technology (SIMIT), Chinese Academy of Sciences), NovelSi specializes in heterogeneous integration of ferroelectric thin films (LiNbO₃, LiTaO₃) on silicon, silicon carbide, and sapphire substrates. The company holds over 50 patents in direct wafer bonding, ion-slicing (Smart Cut™-like technology), and surface-activated bonding (SAB). NovelSi’s manufacturing capacity (2025): 10,000 wafers/month (4-inch, 6-inch, 8-inch), with 12-inch under development.

Exclusive observation: NovelSi has a first-mover and near-monopoly advantage in LiTaO₃-on-Si wafers, leveraging its proprietary ion-slicing and direct bonding technology (similar to Soitec’s Smart Cut™ for SOI wafers). Competitors (Soitec, Shin-Etsu, Sumco, NTT-AT) focus on LiNbO₃-on-insulator (LNOI) wafers (more mature for electro-optic modulators), but LiTaO₃-on-Si offers advantages: (1) lower optical loss (LiTaO₃: <0.1 dB/cm vs. LiNbO₃: 0.2-0.5 dB/cm at 1550nm); (2) higher photorefractive damage threshold (LiTaO₃ less susceptible to DC drift); (3) better thermal stability (LiTaO₃ Curie temperature ~600°C vs. LiNbO₃ ~1140°C, but operationally similar); (4) potential for lower cost (LiTaO₃ single crystal cheaper than LiNbO₃ for some grades). NovelSi is actively developing 8-inch and 12-inch LiTaO₃-on-Si wafers to meet industry demand (standard silicon photonics foundries use 200mm/300mm lines).

3. Technology Trends, Policy Drivers & User Cases (Last 6 Months)

Recent technology advancements (Q3 2025–Q1 2026):

- 8-inch LiTaO₃-on-Si wafer commercialization – NovelSi announced production-ready 8-inch (200mm) LiTaO₃-on-Si wafers (Q4 2025), enabling compatibility with standard silicon photonics foundries (Tower Semiconductor, GlobalFoundries, IMEC).

- Low-loss thin-film LiTaO₃ waveguides – Researchers demonstrated propagation loss <0.05 dB/cm in thin-film LiTaO₃ (thickness 300-500nm), matching state-of-the-art SiN and surpassing LiNbO₃ (0.1-0.2 dB/cm).

- High-speed LiTaO₃ modulators – 100 Gbaud (160 Gbps PAM4) electro-optic modulators demonstrated in LiTaO₃-on-Si (3dB bandwidth >67 GHz, VπL ~3 V·cm).

- Hybrid integration with Si PICs – Heterogeneous integration of LiTaO₃ modulators with Si waveguides, Ge photodetectors, and CMOS electronics on single chip (NovelSi + IMEC collaboration).

- Ion-slicing yield improvement – NovelSi’s ion-slicing process (H+ implantation + exfoliation) achieving >95% yield for 6-inch, >90% for 8-inch wafers (up from 70-80% in 2023).

Policy & regulatory updates (last 6 months):

- China’s “14th Five-Year Plan” photonics initiative (November 2025) – RMB 5 billion ($700 million) funding for silicon photonics and heterogeneous integration, including LiTaO₃/LiNbO₃-on-insulator platforms. NovelSi named as key supplier.

- US CHIPS Act photonics funding (October 2025) – AIM Photonics (NY) and American Institute of Manufacturing (AIM) received $150 million for heterogenous photonics, potentially developing LiTaO₃-on-Si alternatives (LiNbO₃ focus initially).

- Export controls on advanced photonics wafers (December 2025) – US restrictions on LiNbO₃-on-insulator (LNOI) wafers to China (limited impact as China has domestic supply from NovelSi for LiTaO₃; LiNbO₃ still imported from Japan/Europe).

Typical user case – Optical Modulator (Telecom Transceiver):

A leading optical transceiver manufacturer (OEM for data center 800G DR8/FR8 modules) evaluated LiTaO₃-on-Si wafers (6-inch, direct bonded) for Mach-Zehnder modulators (MZMs). Compared to bulk LiNbO₃ modulators (5cm length, 5V drive) and Si MZMs (3-5mm length, high insertion loss). LiTaO₃-on-Si MZM: 1mm length, 3V Vπ, <2dB insertion loss, 60GHz bandwidth. Outcome: 40% lower drive power, 50% smaller footprint, compatible with silicon photonics foundry processes. Switched from external LiNbO₃ modulators to on-chip LiTaO₃ modulators for next-gen 1.6T modules (2027 target).

Technical challenge addressed – Ion-slicing yield and defect density for thin-film LiTaO₃. Smart Cut™-like process (H+ implantation at 50-150keV, dose 2-5×10¹⁶ cm⁻², annealing at 200-400°C for exfoliation) leaves residual implantation damage (point defects, dislocations) and surface roughness (5-10nm RMS) requiring CMP (chemical mechanical polishing). Solutions: (1) optimized annealing (two-step: low temperature for exfoliation, high temperature (600-800°C) for defect annealing); (2) surface-activated bonding (SAB) with Ar plasma + fast atom beam (FAB) reducing interface voids; (3) smart-cut with etch-back (CMP + sacrificial oxide layer). NovelSi’s proprietary process achieves <1 defect/cm², <0.5nm RMS roughness for 6-inch wafers (comparable to SOI wafers).

4. Future Outlook & Strategic Implications (2026–2032)

Demand will be driven by six primary forces: (1) 800G/1.6T coherent transceivers (data center interconnects (DCI), metro, long-haul requiring high-bandwidth, low-Vπ modulators); (2) silicon photonics foundry adoption (8-inch/12-inch LiTaO₃-on-Si wafers enabling heterogeneous integration); (3) LiTaO₃ advantages over LiNbO₃ (lower loss, higher stability, potentially lower cost); (4) China’s domestic photonics supply chain (reducing reliance on imported LiNbO₃ wafers (Japan/Switzerland) for telecom and sensing); (5) optical switching for data centers (LiTaO₃-on-Si switches for disaggregated compute/memory); (6) quantum photonics (LiTaO₃’s low loss and low birefringence for integrated quantum circuits).

Strategic recommendation for suppliers: NovelSi – scale 8-inch and 12-inch production (target 50,000 wafers/month by 2028), reduce defect density (<0.1 defects/cm²), develop LiTaO₃-on-SiC and LiTaO₃-on-SiO₂ variants for RF and nonlinear applications. Foundries (Tower, GF, IMEC) – qualify 8-inch LiTaO₃-on-Si process design kits (PDKs) for modulator and switch designs. Equipment vendors (EV Group, SUSS MicroTec) – develop high-throughput wafer bonding tools for LiTaO₃-on-Si (target >20 wafers/hour for 8-inch). OEMs (optical transceiver, sensor manufacturers) – transition from bulk LiNbO₃/LiTaO₃ to heterogeneous wafers for size, power, cost reduction.

Exclusive forecast: The LiTaO₃-on-Si heterogeneous wafer market will reach $280 million by 2032, with direct bonding maintaining 60-65% share (highest performance). Optical modulators will remain largest application (50-55%) driven by 800G/1.6T/3.2T transceivers, but optical switches will grow fastest (40-45% CAGR, reaching 30% share by 2030) as data center optical circuit switching (OCS) adoption increases. NovelSi will maintain market leadership (60-70% share) through 2030, with potential competition from Soitec (LNOI wafers may pivot to LiTaO₃), Shin-Etsu, and Chinese entrants (SICC, IV Semiconductors). China will dominate LiTaO₃-on-Si supply (80-90% share) due to NovelSi’s head start and government support, with US/Europe developing LiNbO₃-on-insulator (LNOI) alternatives. By 2028, 8-inch LiTaO₃-on-Si wafers will be standard (90% of shipments), with 12-inch ramping. Cost per 8-inch wafer projected to decline from $1,500-2,000 (2025) to $800-1,200 (2030) as volumes scale (100,000+ wafers/year).

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp