PAA Anode Binders Market Summary

PAA Anode Binders is a new, environmentally friendly, water-based binder material for lithium batteries. Its unique bonding properties improve electrode structural stability and enhance battery cycle life. Its excellent compatibility with silicon-based anode materials makes it an ideal choice for silicon-based anode binders. PAA is gradually replacing traditional anode binders (CMC+SBR), particularly in high-capacity lithium-ion battery applications (which require high cycle life), and holds enormous market potential. The report is primarily based on statistics of PAA negative electrode adhesive in powder form.

Source, Indigo

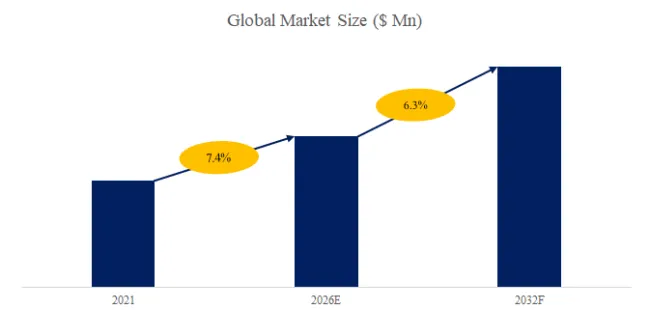

According to the new market research report “Global PAA Anode Binders Market Report 2026-2032”, published by QYResearch, the global PAA Anode Binders market size is projected to reach USD 0.9 billion by 2032, at a CAGR of 22.4% during the forecast period.

Figure00001. Global PAA Anode Binders Market Size (US$ Million), 2021-2032

Above data is based on report from QYResearch: Global PAA Anode Binders Market Report 2026-2032 (published in 2026). If you need the latest data, plaese contact QYResearch.

A Panoramic View of the Industry Chain: Ecosystem Collaboration from Raw Material Refining to End-User Applications

The PAA (Polyacrylic Acid) anode adhesive industry chain has formed a complete closed loop encompassing upstream raw materials, midstream preparation, and downstream applications. Upstream, acrylic acid monomers are the core raw material, supplemented by initiators, crosslinking agents, and other additives. The quality of the acrylic acid directly affects the bonding performance and stability of the anode adhesive. Domestic companies are gradually achieving large-scale production of high-purity monomers through catalytic oxidation process optimization. Midstream consists of specialized anode adhesive manufacturers who develop customized products suitable for different anode materials using emulsion polymerization, solution polymerization, and other technologies. For example, high-elasticity PAA adhesive for silicon-based anodes effectively buffers volume expansion during charge and discharge; low-cost general-purpose adhesives for graphite anodes balance bonding strength and cost through molecular weight control. Downstream covers diverse fields such as power batteries, consumer electronics, and energy storage, with new energy vehicles and energy storage markets becoming the main growth drivers. For instance, a leading battery company applies PAA anode adhesive to 4680 large cylindrical batteries, significantly improving cycle life and safety, driving the industry chain towards higher value-added segments.

Policy Support: Dual Carbon Goals Guide Standardized Industry Development Policy dividends provide a dual impetus for the PAA anode adhesive industry. At the national level, the new energy industry has been listed as a strategic emerging industry, with clear requirements to improve the performance and safety of battery materials, pointing the way for the technological upgrade of PAA anode adhesives. For example, the “New Energy Vehicle Industry Development Plan (2021-2035)” proposes “breakthroughs in high-safety, long-life battery material technologies,” directly driving the iteration of anode adhesives towards high bonding strength and low expansion rate. The “Lithium-ion Battery Industry Standard Conditions” issued by the Ministry of Industry and Information Technology imposes strict requirements on indicators such as impurity content and thermal stability of battery materials, prompting companies to optimize production processes and improve product consistency. At the local level, new energy industry clusters such as Jiangsu and Guangdong have introduced supporting policies, providing financial subsidies and tax incentives for anode adhesive R&D projects, attracting upstream and downstream enterprises to collaborate and form a regional ecological cluster of “raw materials-preparation-application.”

Trends and Opportunities: Technological Breakthroughs and Scenarios Expanding to Shape a New Industry Landscape

The industry is exhibiting three major development trends: First, material innovation, with performance improved through copolymerization modification and nanocomposite technologies. For example, introducing acrylonitrile monomers can enhance the alkali resistance of PAA, making it suitable for high-nickel ternary cathode systems; adding silica nanoparticles can improve the mechanical strength of the colloid and suppress negative electrode pulverization. Second, diversified applications, penetrating from power batteries to energy storage, low-speed vehicles, and other fields. For instance, in solid-state battery development, PAA negative electrode adhesive has become a potential binder choice due to its good interfacial compatibility; in the industrialization of sodium-ion batteries, its low-cost advantage and the universality of PAA create a synergistic effect. Third, green sustainability, with water-based PAA adhesives replacing traditional oil-based adhesives as the mainstream, reducing VOC emissions and aligning with the global carbon neutrality trend. For example, a company has developed a bio-based PAA adhesive, with raw materials derived from renewable resources, reducing carbon emissions by 40% compared to traditional products. On the opportunity side, the continued increase in the penetration rate of new energy vehicles and the explosive growth of the energy storage market are creating massive demand for PAA anode adhesives. Simultaneously, the commercialization of new technologies such as silicon-based anodes and solid-state batteries is driving the expansion of the high-end anode adhesive market, opening up new avenues for companies with technological reserves.

Challenges and Breakthroughs: A Leap from Performance Optimization to Ecosystem Co-construction The industry faces multiple challenges: Technologically, high-end products still rely on imports; for example, the preparation technology of high-elasticity, high-temperature resistant PAA adhesives is monopolized by a few international companies. In terms of cost, fluctuations in raw material prices and investment in environmental protection processes are driving up production costs, making it difficult for some small and medium-sized enterprises (SMEs) to maintain competitiveness. In terms of standards, the industry lacks a unified quality evaluation system, and the performance differences between products from different companies are significant, hindering large-scale application. The solution lies in differentiated competition and ecosystem collaboration: leading companies should focus on the high-end market and overcome technological bottlenecks through industry-academia-research cooperation; SMEs should cultivate niche areas, such as developing specialized adhesives for specific anode materials; and upstream and downstream collaboration should be strengthened, for example, battery companies and anode adhesive manufacturers should jointly build laboratories to optimize material formulations and battery design, forming a closed-loop innovation cycle of “demand-R&D-application”.

Barriers to Entry: A Triple Test of Technology, Capital, and Ecosystem The PAA anode adhesive market faces high barriers to entry: Technological barriers require mastering core patents such as emulsion polymerization kinetic control and precise molecular weight regulation; for example, real-time monitoring of colloidal particle size using dynamic light scattering technology requires long-term experience. Capital barriers necessitate massive investments in R&D equipment, environmental facilities, and large-scale production lines; for instance, a thousand-ton-level production line requires an investment exceeding 100 million yuan. Ecosystem barriers require establishing long-term trust relationships with battery companies and verifying product performance through multiple rounds of testing, making it difficult for new entrants to quickly integrate into the supply chain. Against this backdrop, new participants must break through these barriers through differentiated positioning, such as focusing on the low-cost water-based adhesive market or developing specialty adhesives suitable for emerging battery technologies, to secure a place in the fiercely competitive market.

About The Authors

| Chengping Zhang | A experienced Technology & Market Analyst. Deep experience in chemical industry, focus on electronic materials, engineering materials and mineral resources, etc. Fully engaged in the development of technology and market reports as well as custom projects. | |

|

Senior Analyst |

||

| Email: zhangchengping@qyresearch.com |

Website: www.qyresearch.com Hot Line:4006068865

QYResearch focus on Market Survey and Research

US: +1-888-365-4458(US) +1-202-499-1434(Int’L)

EU: +44-808-111-0143(UK) +44-203-734-8135(EU)

Asia: +86-10-8294-5717(CN) +852-30628839(HK)

About QYResearch

QYResearch founded in California, USA in 2007.It is a leading global market research and consulting company. With over 17 years’ experience and professional research team in various cities over the world QY Research focuses on management consulting, database and seminar services, IPO consulting (data is widely cited in prospectuses, annual reports and presentations), industry chain research and customized research to help our clients in providing non-linear revenue model and make them successful. We are globally recognized for our expansive portfolio of services, good corporate citizenship, and our strong commitment to sustainability. Up to now, we have cooperated with more than 60,000 clients across five continents. Let’s work closely with you and build a bold and better future.

QYResearch is a world-renowned large-scale consulting company. The industry covers various high-tech industry chain market segments, spanning the semiconductor industry chain (semiconductor equipment and parts, semiconductor materials, ICs, Foundry, packaging and testing, discrete devices, sensors, optoelectronic devices), photovoltaic industry chain (equipment, cells, modules, auxiliary material brackets, inverters, power station terminals), new energy automobile industry chain (batteries and materials, auto parts, batteries, motors, electronic control, automotive semiconductors, etc.), communication industry chain (communication system equipment, terminal equipment, electronic components, RF front-end, optical modules, 4G/5G/6G, broadband, IoT, digital economy, AI), advanced materials industry Chain (metal materials, polymer materials, ceramic materials, nano materials, etc.), machinery manufacturing industry chain (CNC machine tools, construction machinery, electrical machinery, 3C automation, industrial robots, lasers, industrial control, drones), food, beverages and pharmaceuticals, medical equipment, agriculture, etc.

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 18 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp

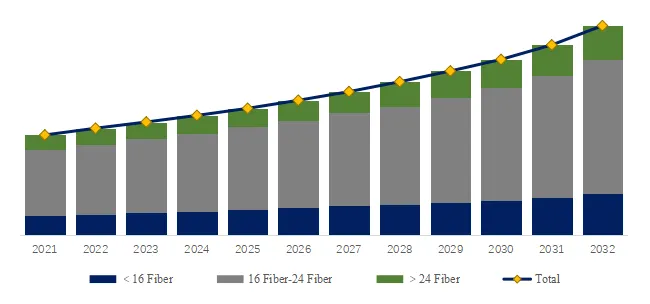

MT Ferrule, Global Market Size, Split by Product Segment

MT Ferrule, Global Market Size, Split by Product Segment