EV Battery Cyclers

EV Battery Cyclers are specialized charge-discharge testing systems used to simulate the real operating conditions of electric vehicle batteries. They repeatedly charge and discharge lithium-ion battery cells, modules, or packs under controlled voltage, current, temperature, and safety parameters to evaluate performance, capacity retention, cycle life, thermal behavior, and reliability. These systems are widely used in battery R&D laboratories, EV OEM validation centers, and battery manufacturing formation and aging lines, and often include regenerative power technology that feeds discharged energy back to the grid to improve efficiency.

EV Battery Cyclers Market Summary

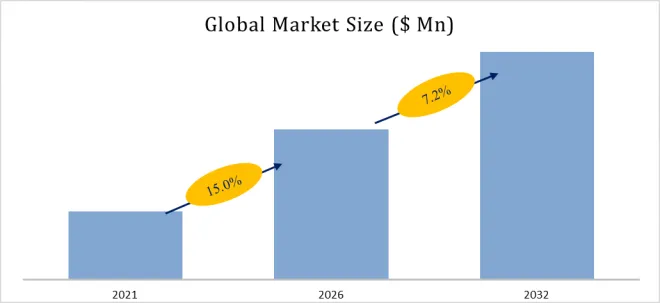

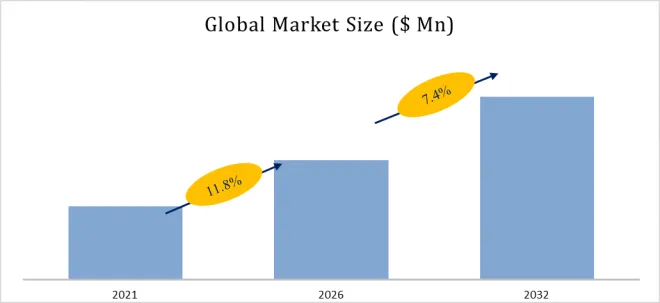

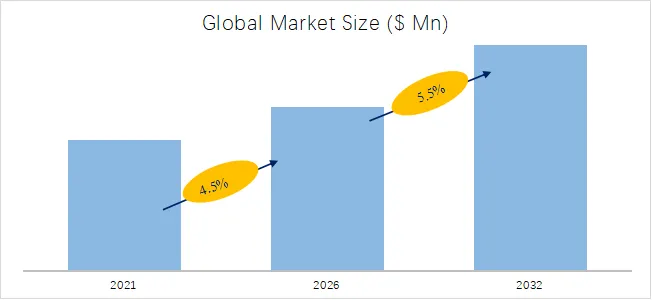

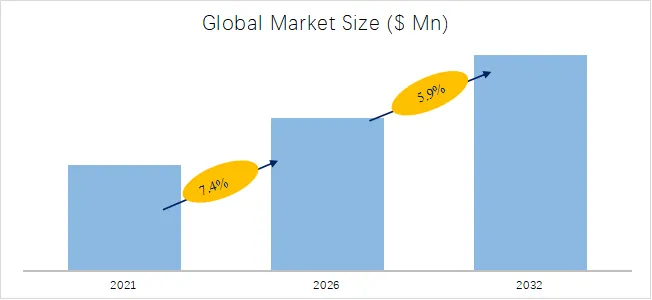

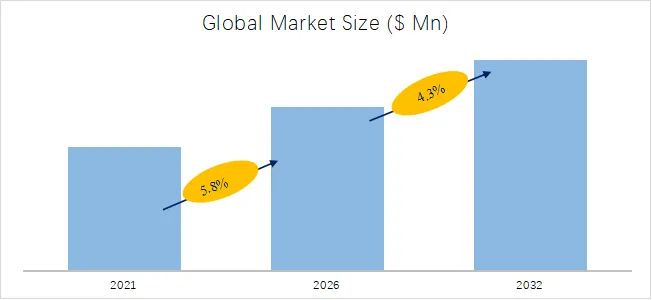

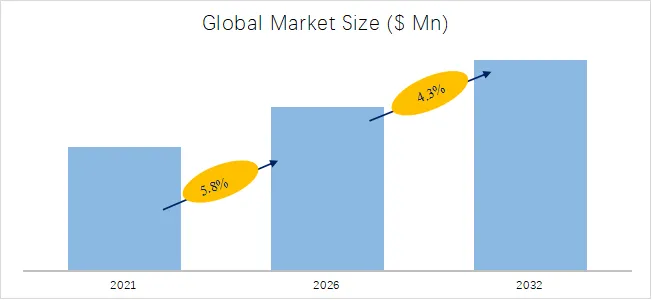

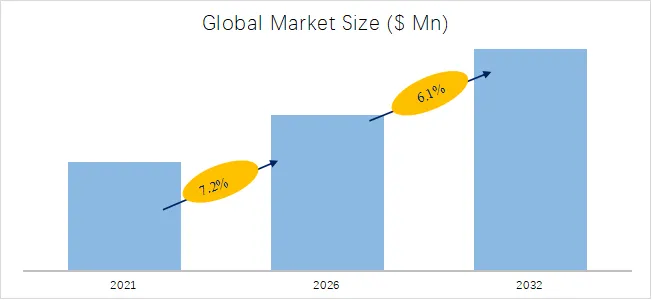

According to the new market research report “Global EV Battery Cyclers Market Report 2026-2032”, published by QYResearch, the global EV Battery Cyclers market size is projected to reach USD 0.66 billion by 2031, at a CAGR of 6.1% during the forecast period.

Global EV Battery Cyclers Market Size (US$ Million), 2021-2032

Above data is based on report from QYResearch: Global EV Battery Cyclers Market Report 2026-2032 (published in 2025). If you need the latest data, plaese contact QYResearch.

Global EV Battery Cyclers Market

Market Drivers:

The global EV battery cyclers market is primarily driven by the rapid growth of electric vehicle production and the expansion of lithium-ion battery manufacturing capacity worldwide. Every battery cell must undergo formation, aging, and performance validation testing, which requires large numbers of charge–discharge cycler channels in gigafactories. In addition, the shift toward higher-energy chemistries such as high-nickel cathodes, LFP fast-charging cells, and solid-state batteries increases testing complexity and cycle duration, further expanding equipment demand. Stricter safety certification, automotive qualification standards, and battery warranty requirements from automakers are also encouraging OEMs and cell manufacturers to invest in higher-precision and regenerative testing systems.

Restraint:

A major restraint in the EV battery cycler market is the high capital expenditure and long installation cycle associated with large-scale testing infrastructure. Formation and aging equipment requires extensive power supply systems, cooling, and facility integration, making deployment costly for new entrants. In addition, the rapid evolution of battery chemistries and voltage platforms can shorten equipment replacement cycles, creating investment uncertainty. Price competition among equipment vendors, especially in large gigafactory projects, also pressures profit margins and slows adoption of premium high-accuracy systems in cost-sensitive regions.

Opportunity:

Significant opportunities arise from next-generation batteries and new testing requirements across the EV ecosystem. Solid-state batteries, fast-charging platforms (800V architectures), battery swapping systems, and second-life energy storage applications require more advanced testing profiles and higher-power regenerative cyclers. Moreover, the growth of battery recycling, certification laboratories, and independent testing services is expanding demand beyond cell manufacturers. Integration of digital monitoring, cloud data analysis, and AI-based degradation prediction is also creating a new generation of intelligent battery testing equipment, opening opportunities for high-value system suppliers.

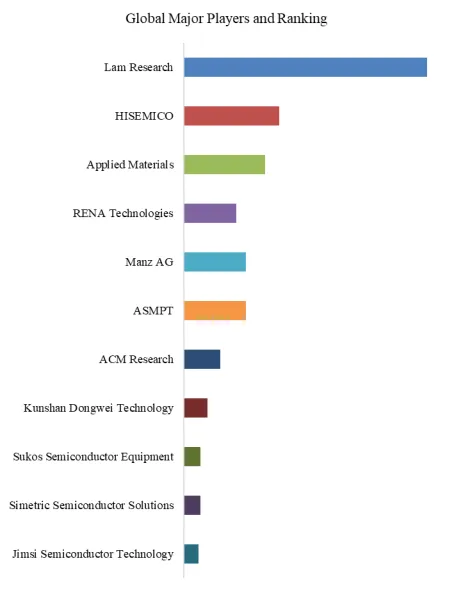

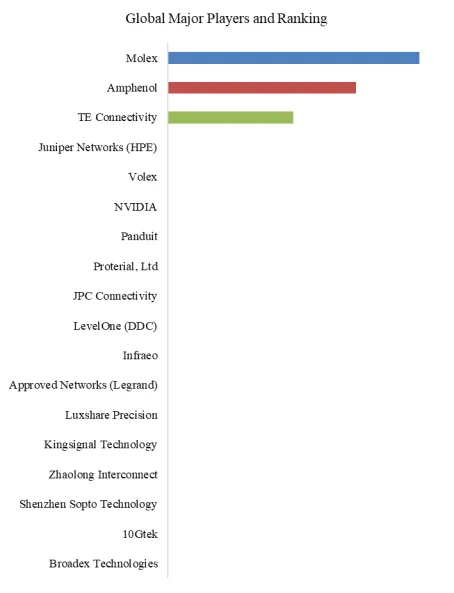

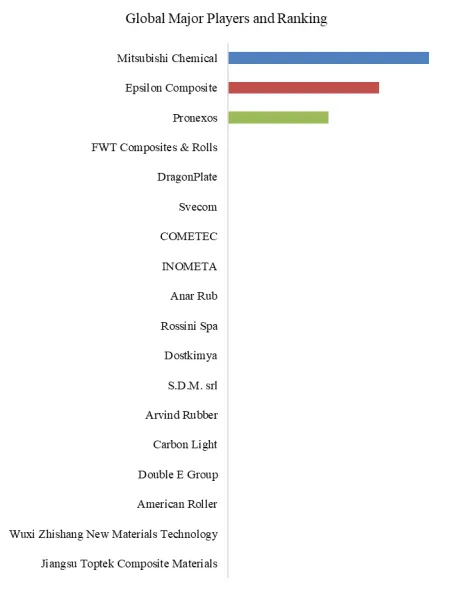

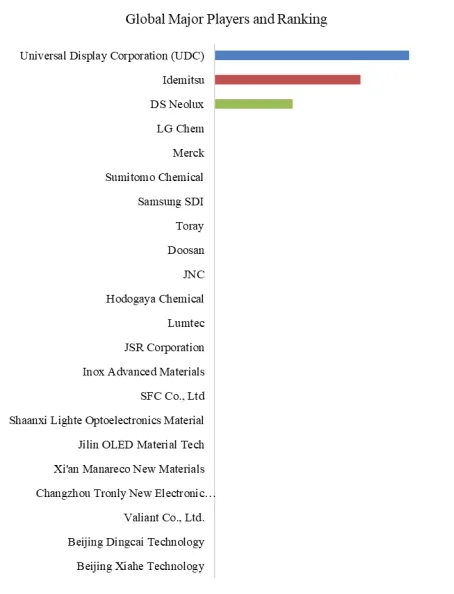

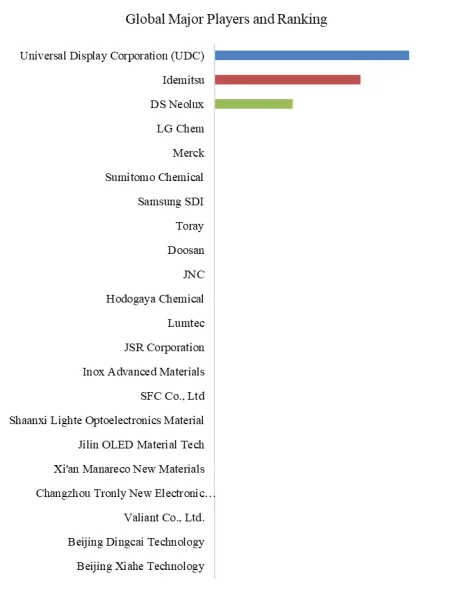

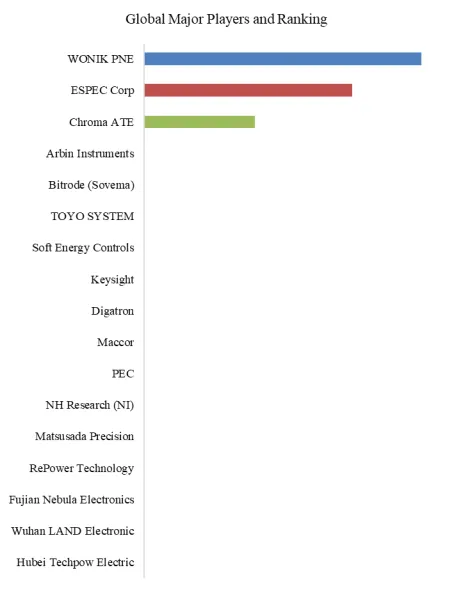

Global EV Battery Cyclers Top 17 Players Ranking and Market Share (Ranking is based on the revenue of 2025, continually updated)

Above data is based on report from QYResearch: Global EV Battery Cyclers Market Report 2026-2032 (published in 2025). If you need the latest data, plaese contact QYResearch.

This report profiles key players of EV Battery Cyclers such as WONIK PNE, ESPEC Corp, Chroma ATE.

In 2023, the global top five EV Battery Cyclers players account for 45.7% of market share in terms of revenue. Above figure shows the key players ranked by revenue in EV Battery Cyclers.

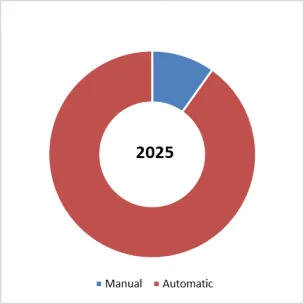

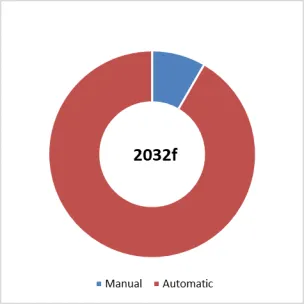

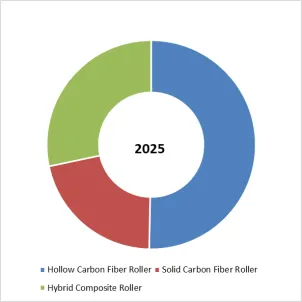

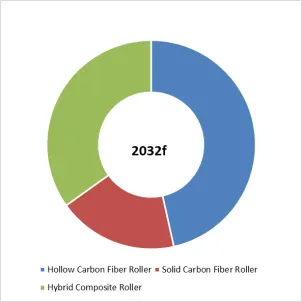

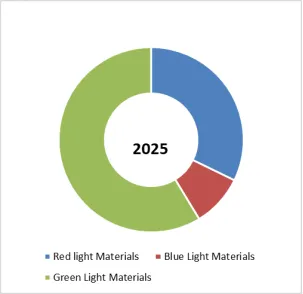

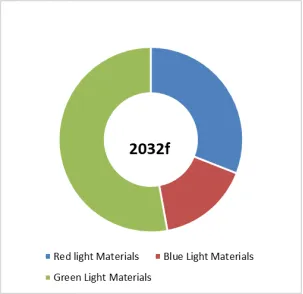

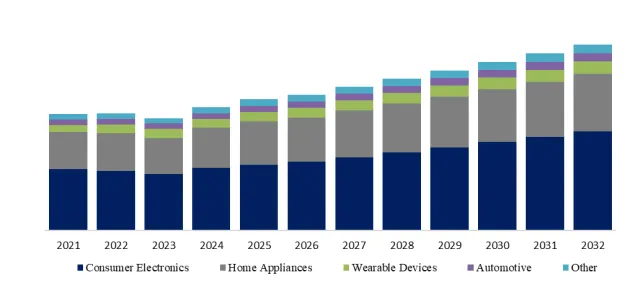

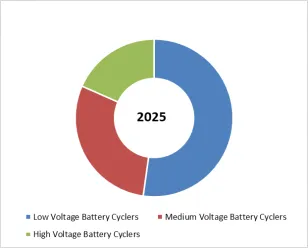

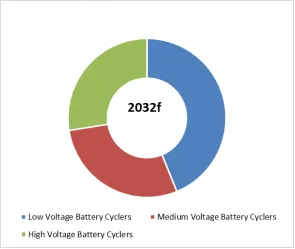

EV Battery Cyclers, Global Market Size, Split by Product Segment

Based on or includes research from QYResearch: Global EV Battery Cyclers Market Report 2026-2032.

In terms of product type, Low Voltage Battery Cyclers is the largest segment, hold a share of 52.2%,

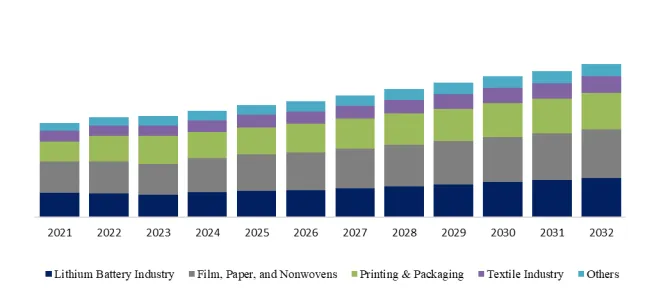

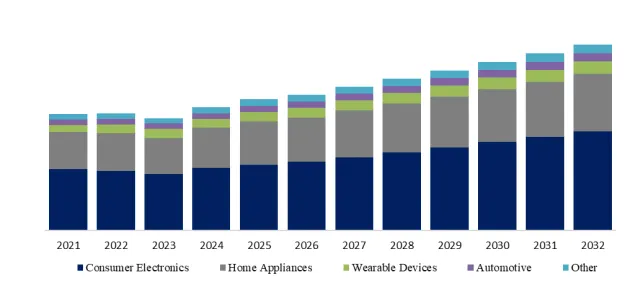

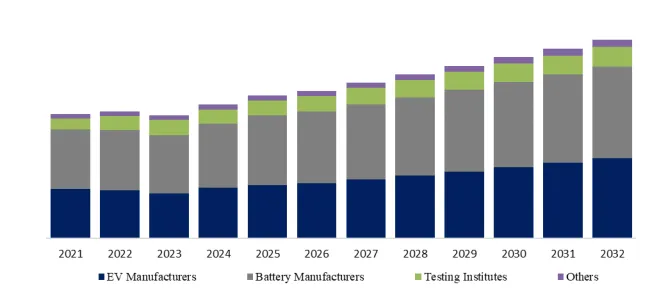

EV Battery Cyclers, Global Market Size, Split by Application Segment

Based on or includes research from QYResearch: Global EV Battery Cyclers Market Report 2026-2032.

In terms of product application, Battery Manufacturers is the largest application, hold a share of 48.5%,

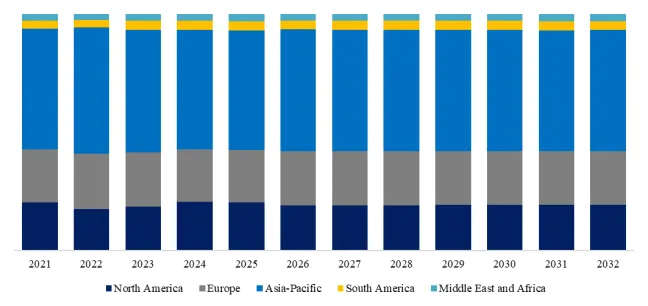

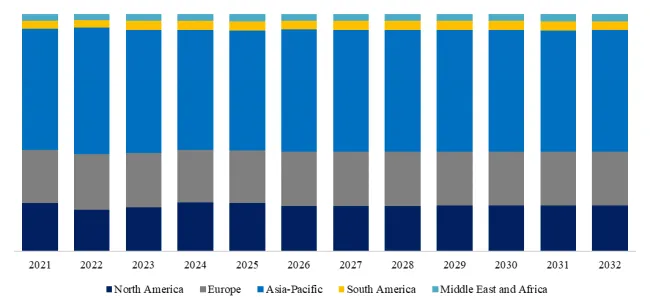

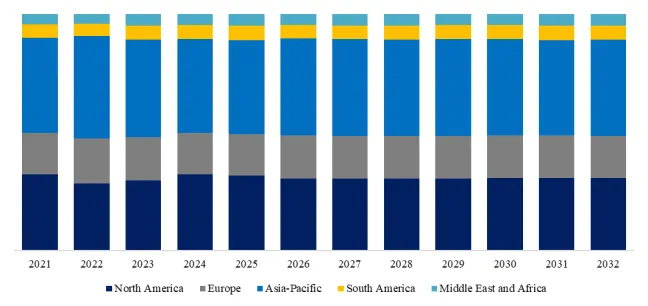

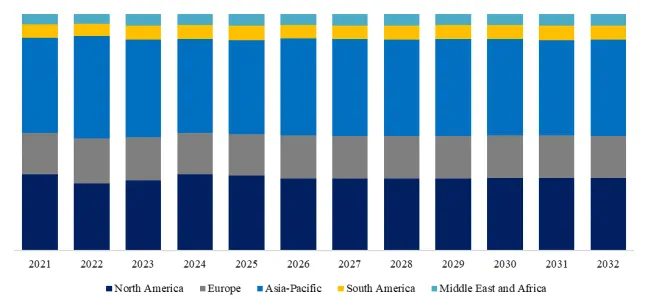

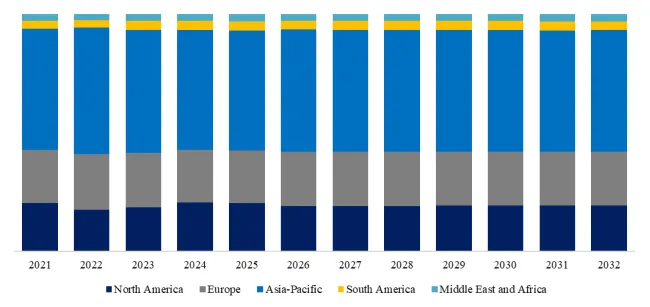

EV Battery Cyclers, Global Market Size, Split by Region

Based on or includes research from QYResearch: Global EV Battery Cyclers Market Report 2026-2032.

About QYResearch

QYResearch founded in California, USA in 2007.It is a leading global market research and consulting company. With over 17 years’ experience and professional research team in various cities over the world QY Research focuses on management consulting, database and seminar services, IPO consulting, industry chain research and customized research to help our clients in providing non-linear revenue model and make them successful. We are globally recognized for our expansive portfolio of services, good corporate citizenship, and our strong commitment to sustainability. Up to now, we have cooperated with more than 60,000 clients across five continents. Let’s work closely with you and build a bold and better future.

QYResearch is a world-renowned large-scale consulting company. The industry covers various high-tech industry chain market segments, spanning the semiconductor industry chain (semiconductor equipment and parts, semiconductor materials, ICs, Foundry, packaging and testing, discrete devices, sensors, optoelectronic devices), photovoltaic industry chain (equipment, cells, modules, auxiliary material brackets, inverters, power station terminals), new energy automobile industry chain (batteries and materials, auto parts, batteries, motors, electronic control, automotive semiconductors, etc.), communication industry chain (communication system equipment, terminal equipment, electronic components, RF front-end, optical modules, 4G/5G/6G, broadband, IoT, digital economy, AI), advanced materials industry Chain (metal materials, polymer materials, ceramic materials, nano materials, etc.), machinery manufacturing industry chain (CNC machine tools, construction machinery, electrical machinery, 3C automation, industrial robots, lasers, industrial control, drones), food, beverages and pharmaceuticals, medical equipment, agriculture, etc.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp