Key Blank Market Summary

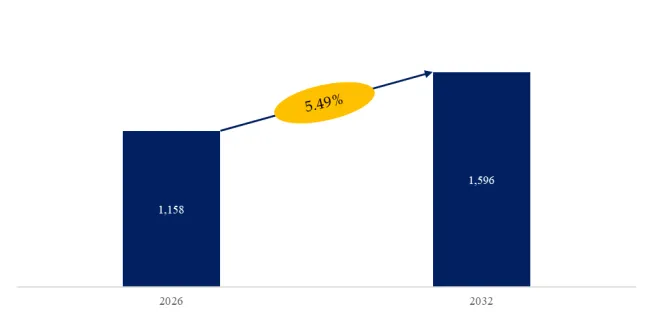

The global Key Blank market — the foundational components of mechanical keys used in residential, commercial, and automotive locking systems — is entering a period of sustained expansion, driven by continued demand for traditional security solutions, growth in construction and automotive sectors, and the ongoing need for replacement and duplication services. According to new market forecasts, the global Key Blank market size is projected to grow from US$ 1.02 billion in 2025 to US$ 1.60 billion by 2032, representing a compound annual growth rate (CAGR) of 5.49% during the forecast period from 2026 to 2032.

Although smart and electronic access technologies have gained traction in recent years, mechanical locks remain widely used around the world, particularly in applications where cost, simplicity, reliability, and compatibility are key considerations. Key blanks — the uncut keys that locksmiths and key duplication services shape into functioning keys — continue to form the backbone of mechanical access systems across residential housing, commercial buildings, automotive applications, and other sectors.

Figure00001. Global Key Blank Market Size (US$ million), 2026-2033

Above data is based on report from QYResearch: Global Key Blank Market Report 2026-2032 (published in 2026). If you need the latest data, plaese contact QYResearch.

Material Types: Brass Dominates Market Share

Key blanks are manufactured from several different materials, with their selection dependent on cost, durability, machinability, and application requirements. In 2025, the global composition of the Key Blank market by material type was:

Brass Key Blank — 60.72%

Iron/Steel Key Blank — 7.09%

Others (e.g., nickel silver, zinc, aluminum) — 32.19%

Brass continues to dominate due to its excellent balance of corrosion resistance, ease of machining, and wear characteristics, which are particularly important for residential and commercial keys subjected to frequent use. Iron and steel blanks, though representing a smaller share, are preferred in certain heavy-duty or industrial applications. Other materials — including advanced alloys and composite materials — are gaining traction in specialized uses or where specific mechanical properties are required.

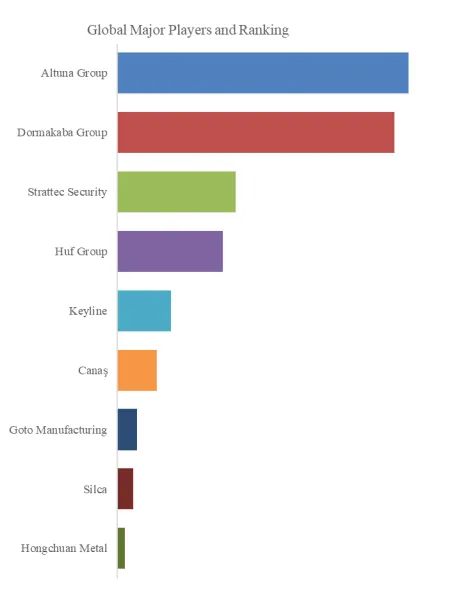

Market Structure: Fragmented, with Leading Players Holding Modest Share

The Key Blank market in 2025 remains relatively fragmented, with a broad mix of international and regional manufacturers supplying products to a global customer base including locksmiths, hardware retailers, building developers, and automotive aftermarkets.

Market data for 2025 shows that the top two revenue generators — Altuna Group and Dormakaba Group — accounted for a combined share of just 15.88% of total global revenue, illustrating the decentralized nature of the market. Additional notable global competitors include Strattec Security, Huf Group, Keyline, Canaş, Goto Manufacturing, Silca, and Hongchuan Metal, with the remainder divided among numerous smaller regional and local producers.

This distribution underscores the decentralized competitive landscape, in which a wide range of manufacturers — both multinational and local — co-exist. Regional producers play an important role, especially in markets with high volumes of key duplication services or local locksmith demand.

Figure00002. Global Key Blank Top 9 Players Ranking and Market Share (Ranking is based on the revenue of 2025, continually updated)

Above data is based on report from QYResearch: Global Key Blank Market Report 2026-2032 (published in 2026). If you need the latest data, plaese contact QYResearch.

End-User Segments: Residential Leads, Commercial and Automotive Gain Ground

By application, the Key Blank market in 2025 was segmented as follows:

Residential — 59.24%

Commercial — 20.07%

Automotive — 10.74%

Others — 9.95%

Residential applications remain the largest segment, driven by ongoing demand for housing construction, rental property turnover, and home security upgrades. Commercial buildings — including offices, retail spaces, institutions, and multi-tenant facilities — represent a significant second category, where complex keying systems and master key suites generate recurring requirements for blanks and replacement keys.

The automotive segment, while smaller, continues to grow as vehicles often require multiple mechanical key solutions (including valet keys, spare keys, and service keys), even as electronic key fobs and smart access systems become more prevalent. The “Others” category includes industrial, institutional, and custom applications that fall outside traditional residential, commercial, and automotive classifications.

Drivers of Growth: Construction, Aftermarket, and Locksmith Services

Several core drivers underpin the forecasted growth of the Key Blank market:

1. Continued Construction Activity

Global residential and commercial construction continues to support demand for key blanks. As cities expand and housing inventories increase in both emerging and developed markets, the need for mechanical access solutions remains, particularly in mid-market and cost-sensitive segments where mechanical locks are preferred.

2. Robust Aftermarket Demand

Locksmith services and hardware retailers around the world rely on a steady supply of key blanks for duplication, replacement, and emergency service work. The expansion of automotive ownership and aging building infrastructure also contributes to ongoing aftermarket requirements.

3. Replacement and Security Maintenance

Periodic wear, lost keys, tenant turnover, and security upgrades drive repeat purchases of key blanks. Even in buildings with electronic access control, mechanical keys often remain in auxiliary roles such as service access, storage areas, and low-security entry points, sustaining baseline demand.

Challenges Facing the Market

Despite growth prospects, the Key Blank market faces challenges:

1. Price Sensitivity and Commoditization

Key blanks are highly price-competitive commodity products. Manufacturers and distributors operate on relatively thin margins, and purchasers — especially hardware retailers and wholesale buyers — frequently prioritize price and availability over brand.

2. Electronics and Smart Lock Adoption

The rising adoption of electronic locks, smart access systems, and mobile key solutions presents structural pressure on mechanical key demand. Although mechanical keys remain critical in many applications, particularly in cost-sensitive regions and backup roles, the long-term migration toward digital access could constrain future mechanical key blank growth.

3. Supply Chain Complexity

Fragmented manufacturing and distribution networks present operational challenges, including inconsistent quality standards, raw material price fluctuations (especially brass and steel), and logistical irregularities in global supply chains.

Regional Insights and Innovation Trends

Regional demand patterns reveal nuanced dynamics. North America and Western Europe, with mature construction markets and well-established locksmith industries, account for substantial portions of global key blank consumption. In contrast, the Asia-Pacific region, particularly China, India, and Southeast Asia, exhibits the fastest growth rates owing to urbanization, expanding housing markets, and increasing DIY home improvement trends.

Innovation in the Key Blank market centers on materials engineering, manufacturing automation, and integration with digital key coding. Manufacturers are exploring new alloys that balance machinability with durability, and adopting precision stamping and CNC machining to improve efficiency and reduce production costs. There is also increasing interest in key blanks designed for hybrid systems, where mechanical and electronic access features coexist.

Outlook to 2032

Looking ahead, the Key Blank market is expected to grow steadily through 2032, achieving an estimated value of US$ 1.60 billion. While electronic access technologies will continue to evolve, mechanical key blanks are likely to remain indispensable in many segments due to their cost-effectiveness, simplicity, and established ubiquity. The market’s growth will be shaped by robust residential and commercial demand, ongoing aftermarket services, and evolving manufacturing innovations that optimize quality and cost.

For industry stakeholders — from global manufacturers to regional distributors — strategic emphasis on expanded material offerings, enhanced manufacturing precision, and adaptive distribution networks will be key to capturing sustained value in the evolving Key Blank landscape.

About QYResearch

QYResearch founded in California, USA in 2007.It is a leading global market research and consulting company. With over 17 years’ experience and professional research team in various cities over the world QY Research focuses on management consulting, database and seminar services, IPO consulting (data is widely cited in prospectuses, annual reports and presentations), industry chain research and customized research to help our clients in providing non-linear revenue model and make them successful. We are globally recognized for our expansive portfolio of services, good corporate citizenship, and our strong commitment to sustainability. Up to now, we have cooperated with more than 60,000 clients across five continents. Let’s work closely with you and build a bold and better future.

QYResearch is a world-renowned large-scale consulting company. The industry covers various high-tech industry chain market segments, spanning the semiconductor industry chain (semiconductor equipment and parts, semiconductor materials, ICs, Foundry, packaging and testing, discrete devices, sensors, optoelectronic devices), photovoltaic industry chain (equipment, cells, modules, auxiliary material brackets, inverters, power station terminals), new energy automobile industry chain (batteries and materials, auto parts, batteries, motors, electronic control, automotive semiconductors, etc.), communication industry chain (communication system equipment, terminal equipment, electronic components, RF front-end, optical modules, 4G/5G/6G, broadband, IoT, digital economy, AI), advanced materials industry Chain (metal materials, polymer materials, ceramic materials, nano materials, etc.), machinery manufacturing industry chain (CNC machine tools, construction machinery, electrical machinery, 3C automation, industrial robots, lasers, industrial control, drones), food, beverages and pharmaceuticals, medical equipment, agriculture, etc.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp