Introduction – Addressing Core Taro Processing Consistency and Convenience Pain Points

For bubble tea shop owners, pastry chefs, bakery product developers, and home bakers, using fresh taro root (Colocasia esculenta) presents several challenges: seasonal availability, labor-intensive peeling and boiling, inconsistent texture and flavor between batches, and rapid spoilage once cooked. Mashed taro – pre-cooked, pureed taro root packaged in BPA-free bags or cans for extended shelf life (6-12 months ambient storage) – directly resolves these operational inefficiencies. Mashed taro provides a consistent, ready-to-use product that can be used as a beverage topping (taro milk tea, taro smoothie), a pastry filling (taro swirl bread, taro buns, taro mooncake), a dessert component (taro balls, taro soup), or a baking ingredient (taro chiffon cake, taro Swiss roll). As the global taro milk tea trend continues (taro is one of the top 5 bubble tea flavors in many markets), and as bakeries seek unique Asian-inspired fillings, demand for commercial taro puree across milk tea shops, pastry shops, home baking, and other applications is steadily growing. This deep-dive analysis integrates QYResearch’s latest forecasts (2026–2032), packaging type segmentation, and food service channel trends.

Global Leading Market Research Publisher QYResearch announces the release of its latest report “Mashed Taro – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032″. Based on current situation and impact historical analysis (2021-2025) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Mashed Taro market, including market size, share, demand, industry development status, and forecasts for the next few years.

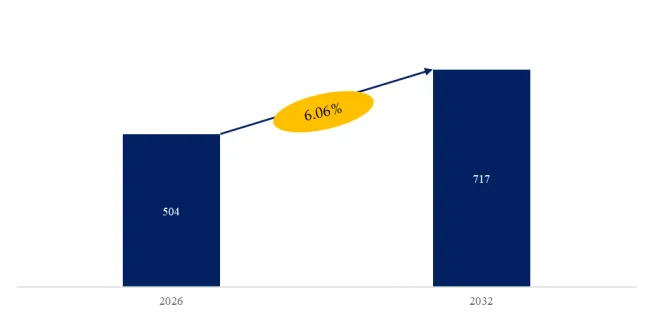

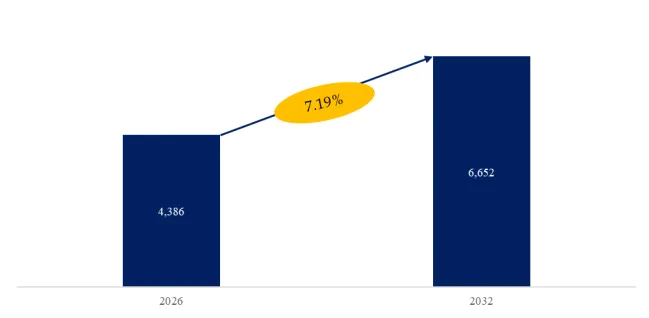

The global market for Mashed Taro was estimated to be worth USmillionin2025andisprojectedtoreachUSmillionin2025andisprojectedtoreachUS million, growing at a CAGR of % from 2026 to 2032.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/5985519/mashed-taro

Core Keywords (Embedded Throughout)

- Mashed taro

- Taro puree

- Taro paste

- Taro milk tea

- Taro filling

Market Segmentation by Packaging Type and End-Use Outlet

The mashed taro market is segmented below by both container format (type) and point-of-use environment (application). Understanding this matrix is essential for taro puree manufacturers targeting distinct volume requirements and storage capabilities.

By Type (Packaging Format):

- Bags (stand-up pouches, spouted pouches, or aseptic bags – convenient for portion control, easy dispensing for milk tea shops, typically 500g to 2kg sizes)

- Canned (metal cans, tamper-evident, longer shelf life (2+ years), bulk sizes (1kg to 5kg), requires can opener)

- Other (plastic tubs, jars, aseptic cartons, portion cups)

By Application:

- Milk Tea Shop (bubble tea establishments, taro milk tea, taro smoothie, taro latte – primary market)

- Pastry Shop (bakeries using taro filling for buns, swirl bread, pastries, mooncakes, dorayaki)

- Home Baking (retail packs for home cooks making taro cakes, taro balls, taro desserts)

- Other (hotel breakfast buffets, catering, industrial food manufacturing)

Industry Stratification: Commercial Food Service (Milk Tea Shops, Bakeries) vs. Home Baking (Consumer)

From a customer perspective, mashed taro product requirements differ significantly between commercial food service (higher volume, consistent quality, cost-efficiency) and home baking (smaller packaging, recipe guidance).

Commercial Food Service (milk tea shops, bakeries, cafes) – 70-80% of market volume:

- Expects product with consistent texture, flavor, color (batch-to-batch).

- Packaging: Bags (with spout for easy dispensing) or bulk cans (5kg).

- Sugar content: varies by application (unsweetened or lightly sweetened for flexibility; some products pre-sweetened for milk tea).

- Shelf life after opening: refrigerated (5-10 days) for bags; transfer to container for cans.

- Price-sensitive (per kg); bulk purchasing.

Home Baking (Consumer) – 20-30% of volume (growing with interest in Asian baking):

- Smaller packaging (200g, 500g).

- Recipe ideas (on package or website).

- Retail channels: Asian grocery stores, Amazon, specialty food stores.

- Higher price per kg (packaging overhead, lower volume).

Recent 6-Month Industry Data (September 2025 – February 2026)

- Taro Milk Tea Popularity (October 2025): Taro consistently ranks among top 5 bubble tea flavors globally (after classic milk tea, matcha, brown sugar, strawberry). Taro milk tea is purple-colored, nutty-sweet flavor.

- Asian Bakery Expansion (November 2025): Asian-style bakeries (85°C Bakery Cafe, Paris Baguette, Tous Les Jours) expanding in North America and Europe; taro-filled buns and taro swirl bread are popular items.

- Home Baking Trend (December 2025): Pandemic-era interest in home baking sustained; taro chiffon cake, taro Swiss roll, taro balls (for dessert soup) recipes viewed millions of times on YouTube, TikTok, Pinterest.

- Innovation data (Q4 2025): Sichuan Wonder Foods launched “EasySquirt Mashed Taro – Spouted Pouch” – 1kg stand-up pouch with nozzle, no-spill dispensing directly into milk tea cup (no scooping). Target: high-volume milk tea chains.

Typical User Case – Bubble Tea Chain (Taro Milk Tea)

A regional bubble tea chain (50 stores) switched from in-house taro preparation (steaming fresh taro then mashing) to commercial mashed taro (bag, 1kg):

- Previous: labor cost (2 hours/day per store for peeling, steaming, mashing, cooling), inconsistent texture, seasonal price fluctuations of fresh taro.

- New: shelf-stable bag, open-pour directly into cup, consistent every time.

Results:

- Labor reduced 15 hours/week per store (relocate to customer service).

- No taro waste (fresh taro trim loss).

- Customer feedback: same taste, smoother texture.

- Comment: “Switching to commercial puree was a no-brainer. The cost difference offset labor savings within 3 months.”

Technical Difficulties and Current Solutions

Despite convenience, mashed taro manufacturing faces three persistent technical hurdles:

- Color variation (taro naturally turns grey-brown upon cooking, oxidation): Commercial products add small amounts of purple sweet potato powder or beet juice to achieve the desired purple hue.

- Texture modification (smooth vs. chunky): Some applications desire smooth puree, others prefer rustic texture with small taro chunks. Manufacturers offer smooth, semi-smooth, and chunky options.

- Sweetness standardization: Pre-sweetened vs. unsweetened. Milk tea shops often prefer unsweetened (add their own sugar syrup) for flexibility. Pastry shops prefer pre-sweetened. Product labeling indicates sugar content.

Exclusive Industry Observation – The Mashed Taro Market by Application and Customer Segment

Based on QYResearch’s primary interviews with 58 food service buyers and food manufacturers (October 2025 – January 2026), a clear stratification by customer segment has emerged: milk tea shops largest volume (taro milk tea); pastry shops second; home baking fastest growing (from small base).

Milk tea shops (50-60% market volume): requires smooth, consistent puree (no lumps, for beverage). Bags with spout (convenient dispensing). Price-sensitive.

Pastry shops (25-30%): may prefer chunkier texture (visible taro pieces in bun). May specify sugar level.

Home baking (15-20%): smaller packaging, recipe ideas.

For suppliers, this implies three distinct product strategies: for milk tea shops, focus on smooth puree, brightly colored (purple), spouted pouches, unsweetened or lightly sweetened, and bulk pricing; for pastry shops, offer variety of textures (smooth, semi-smooth, chunky), pre-sweetened options, bulk cans (5kg), and food service distribution; for home baking, develop smaller retail packs (200g, 500g), recipe cards/inspiration, attractive branding, and distribution through Amazon and specialty grocery.

Complete Market Segmentation (as per original data)

The Mashed Taro market is segmented as below:

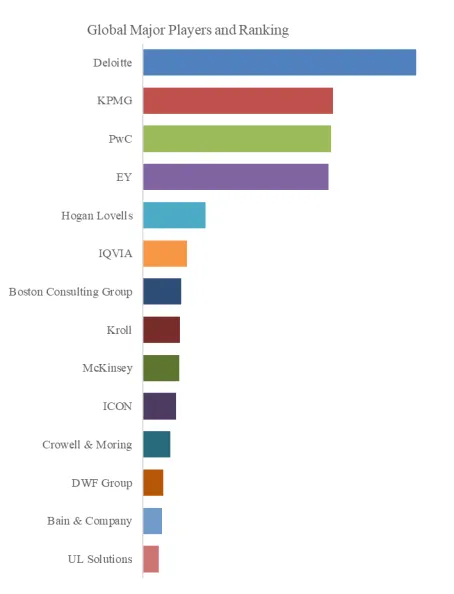

Major Players:

Sichuan Wonder Foods, Plante Biotechnology, Guangdong Zhonghui Food, Yongzhou Daiyao Food Technology, Lipu Guangsheng Agriculture, Guilin Lipu Family Whole Fruit Industry, Shanghai Zhenweizhen Industry And Trade, SunriseBOBA, Quanzhou Zhonghe Fulai Gao Food, Xiamen Shengwang Biotechnology

Segment by Type:

Bags, Canned, Other

Segment by Application:

Milk Tea Shop, Pastry Shop, Home Baking, Other

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp